Advertisement

- United States

- /

- Health Care REITs

- /

- NasdaqGS:SBRA

Sabra Health Care REIT, Inc. Just Missed EPS By 5.9%: Here's What Analysts Think Will Happen Next

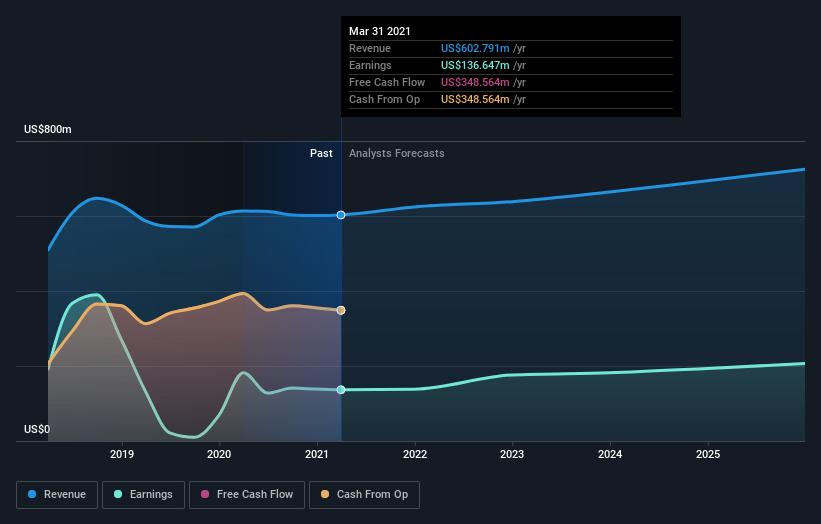

Sabra Health Care REIT, Inc. (NASDAQ:SBRA) shareholders are probably feeling a little disappointed, since its shares fell 2.4% to US$17.73 in the week after its latest first-quarter results. It looks like the results were a bit of a negative overall. While revenues of US$152m were in line with analyst predictions, statutory earnings were less than expected, missing estimates by 5.9% to hit US$0.16 per share. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

View our latest analysis for Sabra Health Care REIT

Taking into account the latest results, the most recent consensus for Sabra Health Care REIT from five analysts is for revenues of US$624.1m in 2021 which, if met, would be a satisfactory 3.5% increase on its sales over the past 12 months. Statutory earnings per share are expected to decrease 2.7% to US$0.64 in the same period. In the lead-up to this report, the analysts had been modelling revenues of US$611.8m and earnings per share (EPS) of US$0.72 in 2021. While next year's revenue estimates increased, there was also a real cut to EPS expectations, suggesting the consensus has a bit of a mixed view of these results.

The consensus price target was unchanged at US$19.07, suggesting the business is performing roughly in line with expectations, despite some adjustments to profit and revenue forecasts. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. There are some variant perceptions on Sabra Health Care REIT, with the most bullish analyst valuing it at US$24.00 and the most bearish at US$17.00 per share. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. It's pretty clear that there is an expectation that Sabra Health Care REIT's revenue growth will slow down substantially, with revenues to the end of 2021 expected to display 4.7% growth on an annualised basis. This is compared to a historical growth rate of 19% over the past five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 6.4% annually. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than Sabra Health Care REIT.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Sabra Health Care REIT. Fortunately, they also upgraded their revenue estimates, although our data indicates sales are expected to perform worse than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Sabra Health Care REIT analysts - going out to 2025, and you can see them free on our platform here.

We don't want to rain on the parade too much, but we did also find 4 warning signs for Sabra Health Care REIT (1 is a bit concerning!) that you need to be mindful of.

If you’re looking to trade Sabra Health Care REIT, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGS:SBRA

Sabra Health Care REIT

As of September 30, 2024, Sabra’s investment portfolio included 373 real estate properties held for investment (consisting of (i) 233 skilled nursing/transitional care facilities, (ii) 39 senior housing communities (“senior housing - leased”), (iii) 68 senior housing communities operated by third-party property managers pursuant to property management agreements (“senior housing - managed”), (iv) 18 behavioral health facilities and (v) 15 specialty hospitals and other facilities), 14 investments in loans receivable (consisting of three mortgage loans and 11 other loans), five preferred equity investments and two investments in unconsolidated joint ventures.

Good value with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.8% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|43.5% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|61.4% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor