Advertisement

- United States

- /

- Specialized REITs

- /

- NasdaqGS:SBAC

SBA Communications Corporation Just Missed Earnings And Its EPS Looked Sad - But Analysts Have Updated Their Models

Last week, you might have seen that SBA Communications Corporation (NASDAQ:SBAC) released its third-quarter result to the market. The early response was not positive, with shares down 2.6% to US$239 in the past week. Sales of US$508m surpassed estimates by 2.0%, although earnings per share missed badly, coming in 45% below expectations at US$0.19 per share. Earnings are an important time for investors, as they can track a company's performance, look at what top analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. So we collected the latest post-earnings consensus estimates to see what could be in store for next year.

View our latest analysis for SBA Communications

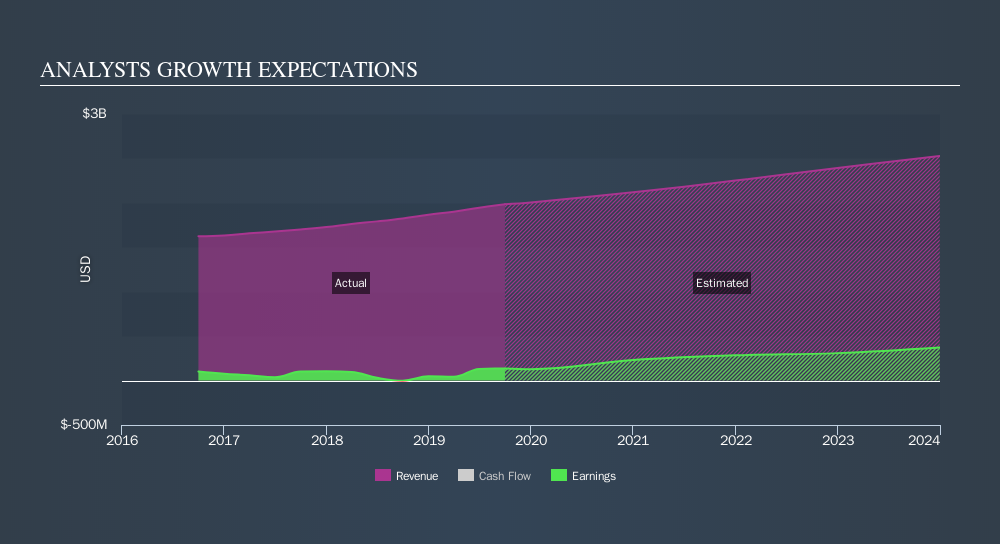

After the latest results, the 15 analysts covering SBA Communications are now predicting revenues of US$2.1b in 2020. If met, this would reflect an okay 6.8% improvement in sales compared to the last 12 months. Earnings per share are expected to soar 76% to US$2.13. Yet prior to the latest earnings, analysts had been forecasting revenues of US$2.1b and earnings per share (EPS) of US$2.10 in 2020. So it's pretty clear that, although analysts have updated their estimates, there's been no major change in expectations for the business following the latest results.

It will come as no surprise then, to learn that the consensus price target is largely unchanged at US$248. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on SBA Communications, with the most bullish analyst valuing it at US$292 and the most bearish at US$155 per share. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how analyst forecasts compare, both to the SBA Communications's past performance and to peers in the same market. Analysts are definitely expecting SBA Communications's growth to accelerate, with the forecast 6.8% growth ranking favourably alongside historical growth of 4.9% per annum over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 5.2% per year. Factoring in the forecast acceleration in revenue, it's pretty clear that SBA Communications is expected to grow much faster than its market.

The Bottom Line

The most obvious conclusion from these results is that there's been no major change in the business' prospects in recent times, with analysts holding earnings per share steady, in line with previous estimates. Fortunately, analysts also reconfirmed their revenue estimates, suggesting sales are tracking in line with expectations - and our data does suggest that SBA Communications's revenues are expected to grow faster than the wider market. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. At Simply Wall St, we have a full range of analyst estimates for SBA Communications going out to 2023, and you can see them free on our platform here..

It might also be worth considering whether SBA Communications's debt load is appropriate, using our debt analysis tools on the Simply Wall St platform, here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NasdaqGS:SBAC

SBA Communications

A leading independent owner and operator of wireless communications infrastructure including towers, buildings, rooftops, distributed antenna systems (DAS) and small cells.

Solid track record and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.3% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor