Advertisement

- United States

- /

- Retail REITs

- /

- NasdaqGS:PECO

What Phillips Edison (PECO)'s Raised Earnings Guidance Signals for Investors in Necessity-Based Retail Centers

Simply Wall St

Reviewed by Sasha Jovanovic

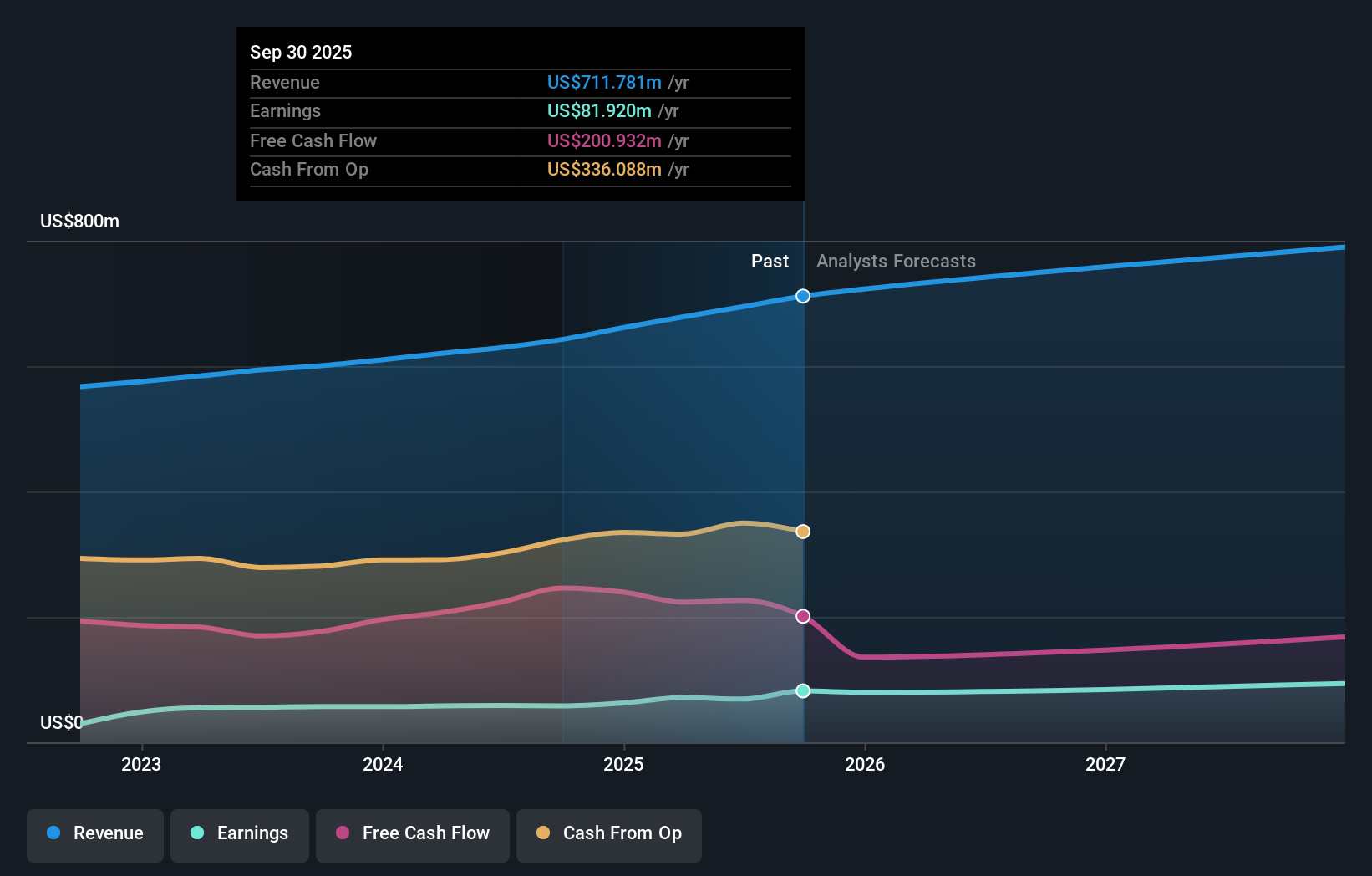

- Phillips Edison & Company, Inc. recently reported its third-quarter and nine-month 2025 earnings, showing strong year-over-year growth in both revenue and net income, and raised its full-year earnings guidance to US$0.62–$0.65 per share.

- These results highlight improved operational performance and confidence in sustained demand for grocery-anchored retail properties within the company's portfolio.

- We'll explore how Phillips Edison's raised earnings outlook further supports its investment narrative of stable income from necessity-based retail centers.

Find companies with promising cash flow potential yet trading below their fair value.

Phillips Edison Investment Narrative Recap

To be a shareholder in Phillips Edison, you need to believe in the resilience of necessity-based, grocery-anchored retail centers even as e-commerce and alternative shopping channels increase competition. The company’s raised earnings guidance reflects ongoing operational strength and stable demand, but does not meaningfully alter key near-term catalysts or the primary risks facing the business, such as continued shifts toward digital-first retail and exposure to the grocery sector.

Among the recent announcements, the company’s decision to increase its full-year earnings guidance to US$0.62–$0.65 per share stands out most. This move closely follows the reported growth in third-quarter revenue and net income, supporting the view that Phillips Edison’s core portfolio continues to deliver stable recurring revenues, which is central to investor expectations.

However, what investors should keep in mind is that persistent competition from digital-first retailers and ongoing changes in consumer preferences could still threaten occupancy rates and long-term growth...

Read the full narrative on Phillips Edison (it's free!)

Phillips Edison's narrative projects $811.1 million in revenue and $93.3 million in earnings by 2028. This requires 5.3% yearly revenue growth and a $24.5 million earnings increase from $68.8 million today.

Uncover how Phillips Edison's forecasts yield a $39.18 fair value, a 14% upside to its current price.

Exploring Other Perspectives

The Simply Wall St Community submitted a single fair value estimate of US$39.18 per share before this latest guidance update. While community sentiment may lag behind recent earnings momentum, broader analyst consensus points to stable revenue streams but also highlights ongoing exposure to disruptive retail trends. Explore how differing perspectives offer fresh insights for your own research.

Explore another fair value estimate on Phillips Edison - why the stock might be worth as much as 14% more than the current price!

Build Your Own Phillips Edison Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Phillips Edison research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Phillips Edison research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Phillips Edison's overall financial health at a glance.

Contemplating Other Strategies?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

- These 16 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Outshine the giants: these 27 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PECO

Phillips Edison

Phillips Edison & Company, Inc. (“PECO”) is one of the nation’s largest owners and operators of high-quality, grocery-anchored neighborhood shopping centers.

Proven track record second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.6% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.6% undervalued

GM

Community Contributor