Advertisement

- United States

- /

- Real Estate

- /

- NasdaqGM:EXPI

eXp World Holdings (NASDAQ:EXPI) Is Paying Out A Larger Dividend Than Last Year

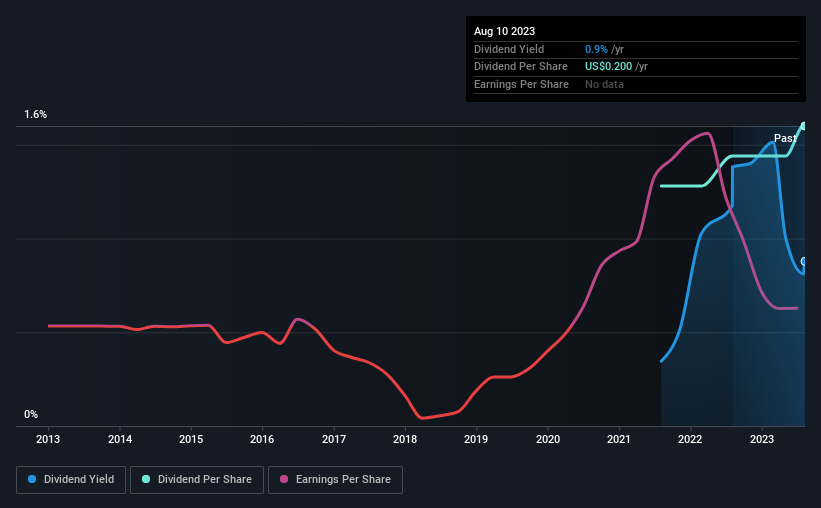

eXp World Holdings, Inc. ( NASDAQ:EXPI ) has announced that it will be increasing its dividend from last year's comparable payment on the 4th of September to $0.05. Even though the dividend went up, the yield is still quite low at only 0.9%.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that eXp World Holdings' stock price has increased by 74% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

Check out our latest analysis for eXp World Holdings

eXp World Holdings' Dividend Is Well Covered By Earnings

Even a low dividend yield can be attractive if it is sustained for years on end. Before making this announcement, eXp World Holdings' dividend was higher than its profits, but the free cash flows quite comfortably covered it. Generally, we think cash is more important than accounting measures of profit, so with the cash flows easily covering the dividend, we don't think there is much reason to worry.

Looking forward, earnings per share is forecast to rise exponentially over the next year. If recent patterns in the dividend continue, we could see the payout ratio reaching 42% which is fairly sustainable.

eXp World Holdings Doesn't Have A Long Payment History

The dividend has been pretty stable looking back, but the company hasn't been paying one for very long. This makes it tough to judge how it would fare through a full economic cycle. The dividend has gone from an annual total of $0.16 in 2021 to the most recent total annual payment of $0.185. This works out to be a compound annual growth rate (CAGR) of approximately 12% a year over that time. eXp World Holdings has been growing its dividend quite rapidly, which is exciting. However, the short payment history makes us question whether this performance will persist across a full market cycle.

Dividend Growth Could Be Constrained

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. eXp World Holdings has seen EPS rising for the last five years, at 51% per annum. EPS has been growing well, but eXp World Holdings has been paying out a massive proportion of its earnings, which can make the dividend tough to maintain.

Our Thoughts On eXp World Holdings' Dividend

Overall, we always like to see the dividend being raised, but we don't think eXp World Holdings will make a great income stock. The payments haven't been particularly stable and we don't see huge growth potential, but with the dividend well covered by cash flows it could prove to be reliable over the short term. We would probably look elsewhere for an income investment.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For instance, we've picked out 3 warning signs for eXp World Holdings that investors should take into consideration. Is eXp World Holdings not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:EXPI

eXp World Holdings

Provides cloud-based real estate brokerage services for residential homeowners and homebuyers.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|27.6% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.1% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|60.0% undervalued

ME

Community Contributor