- United States

- /

- Pharma

- /

- NYSE:NUVB

Nuvation Bio (NUVB): Reassessing Valuation After a Powerful Multi‑Year Share Price Rebound

Reviewed by Simply Wall St

Nuvation Bio (NUVB) has quietly turned heads after a sharp rebound over the past month, with the stock surging as traders reassess its oncology pipeline and long term upside relative to earlier expectations.

See our latest analysis for Nuvation Bio.

That rebound sits on top of a powerful run, with the share price returning 78 percent over the past month and 234 percent year to date, while three year total shareholder return exceeds 340 percent, signaling strong momentum as investors re rate its pipeline risk.

If Nuvation Bio’s surge has you rethinking your healthcare exposure, it might be a good time to explore other potential movers among healthcare stocks.

With shares now well off their lows and trading below consensus targets but after a huge run, the key debate is whether Nuvation Bio still trades at a discount or if markets are already pricing in years of future growth.

Price to Book of 9.1x: Is it justified?

Nuvation Bio trades on a rich 9.1 times price to book at 8.66 dollars, a level that implies investors are already baking in aggressive future progress versus peers.

The price to book multiple compares a company’s market value to its net assets, a common yardstick for capital intensive or asset heavy healthcare and biotech names where near term earnings can be distorted by R and D spend.

For Nuvation Bio, a 9.1 times price to book suggests the market is assigning substantial value to its future oncology pipeline and a potential transition toward profitability, even though the company is currently loss making and has seen losses deepen over the past five years.

That optimism stands out when set against the broader US pharmaceuticals industry, where the average price to book is just 2.5 times. This highlights how forcefully investors are re rating Nuvation Bio’s balance sheet and prospects despite a lack of current profits.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price to Book of 9.1x (OVERVALUED)

However, setbacks in clinical trials or slower than expected commercialization of taletrectinib and other candidates could quickly challenge the current optimism and lofty valuation.

Find out about the key risks to this Nuvation Bio narrative.

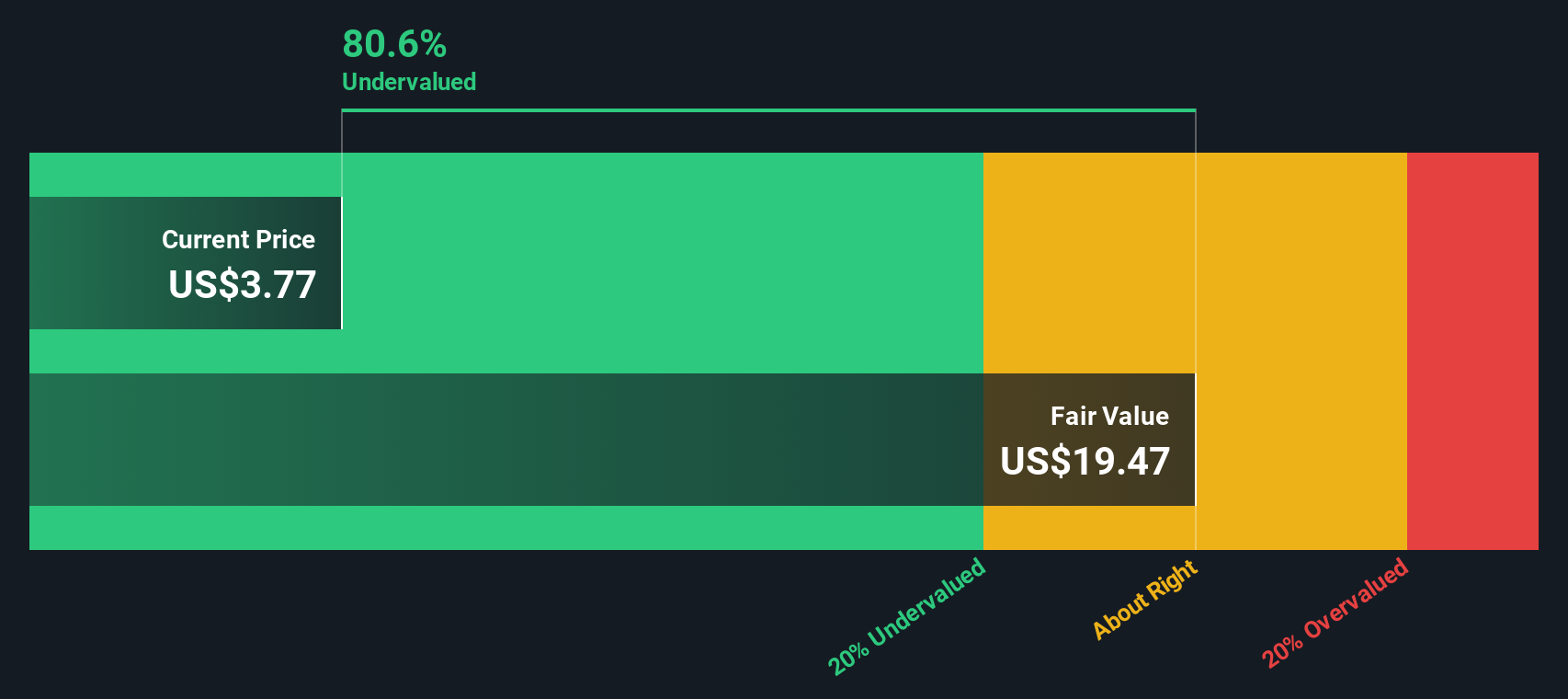

Another View: Our DCF Points to Deep Value

Price to book says Nuvation Bio looks expensive, but our DCF model tells a different story, with fair value at 31.99 dollars versus today’s 8.66 dollars, which implies the stock trades about 73 percent below this estimate of intrinsic value. Readers can consider whether this represents a potential opportunity or simply reflects optimistic assumptions in the forecasts.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Nuvation Bio for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 909 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Nuvation Bio Narrative

If you see the numbers differently or would rather dig into the details yourself, you can build a personalized view in just a few minutes: Do it your way.

A great starting point for your Nuvation Bio research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more high conviction ideas?

Turn today’s insight into your next smart move by using the Simply Wall Street Screener to pinpoint fresh opportunities before the crowd notices them.

- Capture powerful mispricings by targeting these 909 undervalued stocks based on cash flows that the market has not fully appreciated yet.

- Ride the next wave of innovation by zeroing in on these 26 AI penny stocks with potential to transform entire industries.

- Strengthen your income stream by focusing on these 13 dividend stocks with yields > 3% that can help support long term returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Nuvation Bio might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:NUVB

Nuvation Bio

A clinical-stage biopharmaceutical company, focuses on developing therapeutic candidates for oncology.

High growth potential with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)