Advertisement

- United States

- /

- Pharma

- /

- NYSE:JNJ

Is J&J a Good Value After Its 11.2% Monthly Surge and Legal Updates?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Johnson & Johnson’s stock is actually a good deal right now? We’re diving straight into its value, so whether you’re on the fence about buying or just curious, you’re in the right place.

- Johnson & Johnson has caught investors’ attention recently, rising 1.8% in the past week and jumping an impressive 11.2% over the last month. This suggests changes in growth expectations and perceptions of risk.

- Wall Street has buzzed about the company’s advances in its pharmaceutical and medtech divisions, as well as recent legal updates regarding opioid settlements and talc-related litigation. These headlines help set the backdrop for recent price movements and highlight the external factors shaping investor sentiment.

- When it comes to valuation, Johnson & Johnson scores a strong 5 out of 6 on our undervalued checks. Next up, let’s explore which valuation methods got us here, and why there may be an even smarter way to cut through the noise at the end of this article.

Approach 1: Johnson & Johnson Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model is a popular tool for valuation that projects a company’s future cash flows and discounts them back to today’s value. This helps investors gauge what the business is truly worth.

For Johnson & Johnson, the DCF approach uses the company’s current Free Cash Flow of $19.47 Billion as a starting point. Analysts provide cash flow estimates for the next five years, with Simply Wall St extrapolating beyond that. The projection anticipates Free Cash Flow rising to $48.01 Billion by 2035, reflecting consistent growth over the next decade. These projections are all calculated in US Dollars, the company’s reporting currency.

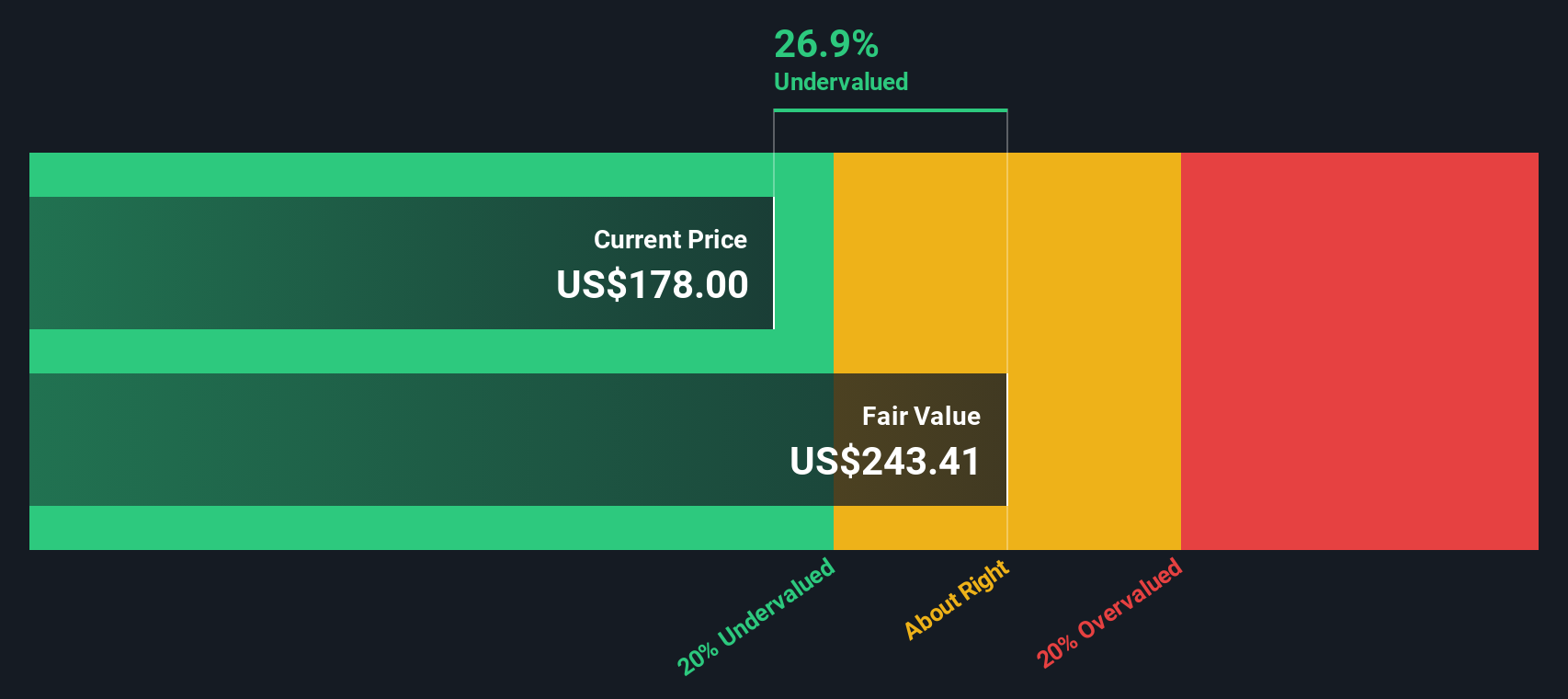

By discounting these expected future cash flows to present-day value, the estimated intrinsic value per share is $384.12. At the current share price, this suggests Johnson & Johnson stock is 46.0% undervalued compared to what the company's future cash generation could deliver.

Based on this analysis, the DCF indicates that Johnson & Johnson currently offers a substantial value opportunity for investors.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Johnson & Johnson is undervalued by 46.0%. Track this in your watchlist or portfolio, or discover 927 more undervalued stocks based on cash flows.

Approach 2: Johnson & Johnson Price vs Earnings (PE)

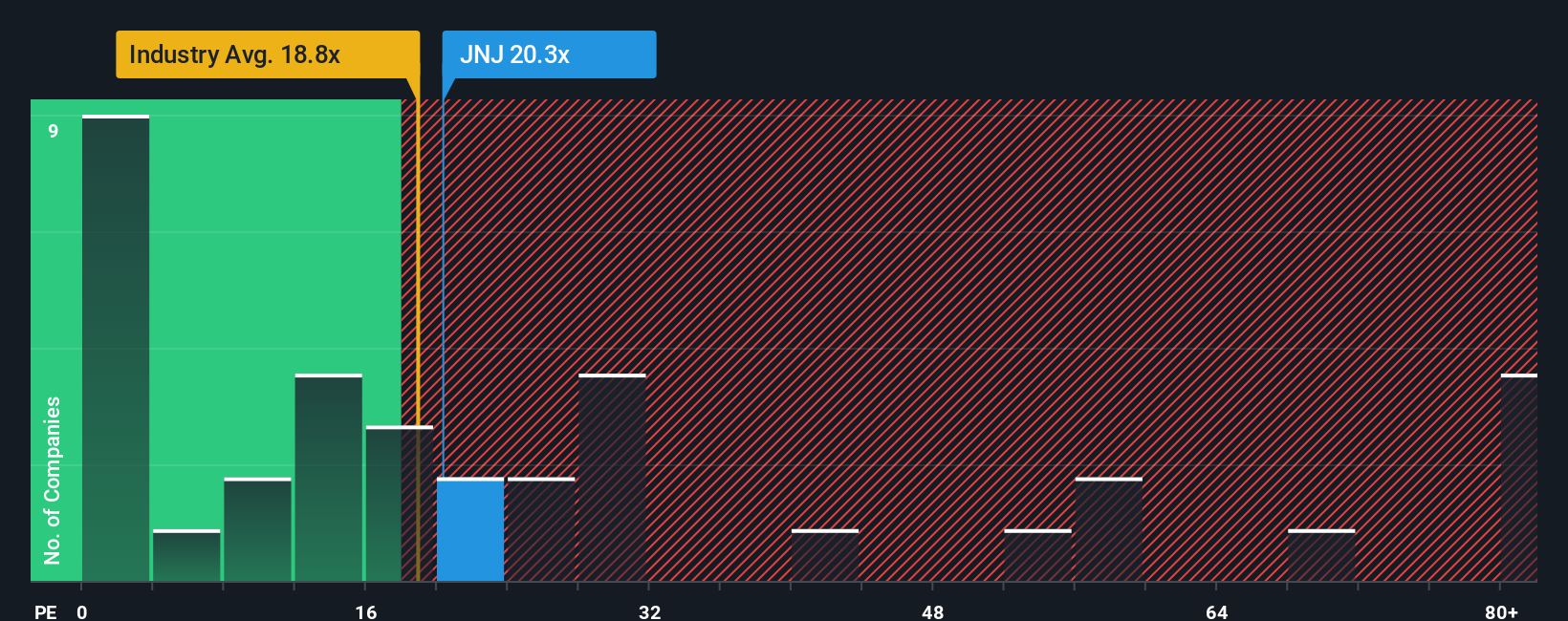

The Price-to-Earnings (PE) ratio is a trusted yardstick for valuing consistently profitable companies like Johnson & Johnson. Because it compares a company's share price with its earnings, the PE ratio gives investors a straightforward sense of how much they are paying for every dollar of profit in the business.

Growth prospects and risk play a big role in determining what is considered a “normal” or fair PE ratio. Faster-growing or lower-risk companies typically trade at higher PE multiples since investors are willing to pay up for quality and future potential, while companies facing slower growth or more uncertainty often sit at lower PE ratios.

Currently, Johnson & Johnson trades on a PE ratio of 19.9x. This is just below the Pharmaceuticals industry average of 20.6x, and well below the peer average of 24.7x. On its surface, this could suggest the stock is cheaper than its competitors. To provide a more tailored benchmark, Simply Wall St’s proprietary “Fair Ratio” model incorporates specific factors like earnings growth, profit margins, market cap, risks, and the unique dynamics of the Pharmaceuticals sector. For Johnson & Johnson, the Fair Ratio is 26.7x.

This approach is more reliable than simple peer and industry comparisons, as the Fair Ratio accounts for the nuances that make each company, even within the same industry, unique in its strengths and risks.

Because Johnson & Johnson’s current PE of 19.9x is meaningfully lower than its Fair Ratio of 26.7x, the stock looks undervalued on this metric as well.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1439 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Johnson & Johnson Narrative

Earlier we mentioned there is an even better way to understand valuation, so let's introduce you to Narratives, a smarter approach that brings your perspective to the investment decision. Rather than relying solely on numbers, Narratives let you connect your view of Johnson & Johnson’s business to a financial forecast and, ultimately, a fair value for the stock.

A Narrative is simply your story or outlook about a company’s future, for example, what you think about their growth in innovative medicines or the impact of legal risks, combined with assumptions about future revenue, margins, and earnings. On Simply Wall St’s Community page, millions of investors use Narratives to set out their own case for a stock, linking the company’s story to the math behind expected returns.

Narratives help you quickly compare your own fair value with the latest share price, making it easier to decide whether to buy or sell. They update dynamically as new information, such as earnings reports or big news, becomes available, so your investing view keeps up with reality.

For instance, one Johnson & Johnson Narrative might forecast a fair value as high as $200, based on growth from next-gen therapies, while another sets it at $155, concerned about exclusivity losses and legal risks. This highlights that your investment decision should always be built around your own story and expectations.

Do you think there's more to the story for Johnson & Johnson? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:JNJ

Johnson & Johnson

Engages in the research and development, manufacture, and sale of various products in the healthcare field worldwide.

Undervalued with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k1.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative