Advertisement

- United States

- /

- Biotech

- /

- NasdaqGM:ZNTL

Zentalis Pharmaceuticals, Inc. (NASDAQ:ZNTL) Surges 26% Yet Its Low P/S Is No Reason For Excitement

Zentalis Pharmaceuticals, Inc. (NASDAQ:ZNTL) shares have continued their recent momentum with a 26% gain in the last month alone. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 39% in the last twelve months.

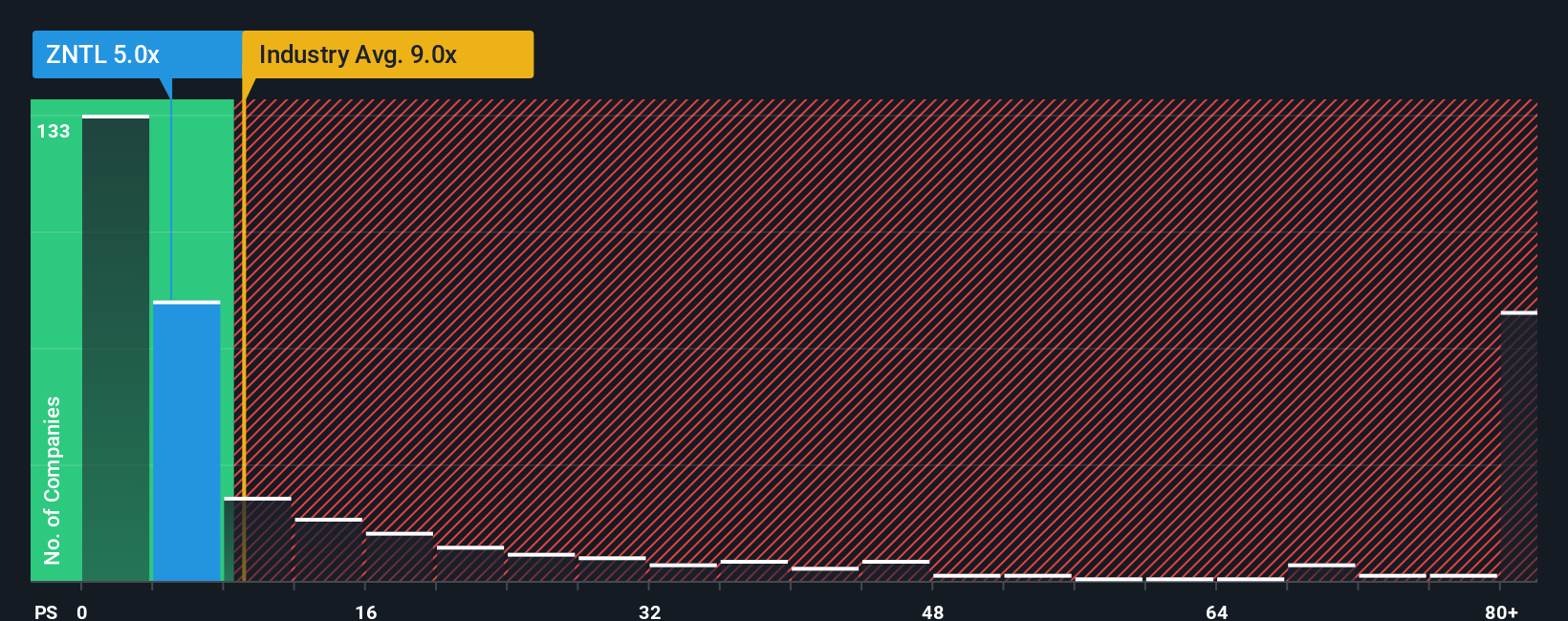

In spite of the firm bounce in price, Zentalis Pharmaceuticals may still be sending bullish signals at the moment with its price-to-sales (or "P/S") ratio of 5x, since almost half of all companies in the Biotechs industry in the United States have P/S ratios greater than 9x and even P/S higher than 67x are not unusual. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Zentalis Pharmaceuticals

How Zentalis Pharmaceuticals Has Been Performing

Zentalis Pharmaceuticals could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. Perhaps the P/S remains low as investors think the prospects of strong revenue growth aren't on the horizon. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Zentalis Pharmaceuticals.Is There Any Revenue Growth Forecasted For Zentalis Pharmaceuticals?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Zentalis Pharmaceuticals' to be considered reasonable.

Retrospectively, the last year delivered a frustrating 34% decrease to the company's top line. At least revenue has managed not to go completely backwards from three years ago in aggregate, thanks to the earlier period of growth. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Turning to the outlook, the next three years should generate growth of 4.6% each year as estimated by the seven analysts watching the company. Meanwhile, the rest of the industry is forecast to expand by 114% per annum, which is noticeably more attractive.

With this in consideration, its clear as to why Zentalis Pharmaceuticals' P/S is falling short industry peers. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Final Word

Despite Zentalis Pharmaceuticals' share price climbing recently, its P/S still lags most other companies. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Zentalis Pharmaceuticals' analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Zentalis Pharmaceuticals that you need to be mindful of.

If these risks are making you reconsider your opinion on Zentalis Pharmaceuticals, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Zentalis Pharmaceuticals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:ZNTL

Zentalis Pharmaceuticals

A clinical-stage biopharmaceutical company, focuses on discovering and developing small molecule therapeutics for the treatment of various cancers in the United States.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|51.2% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|6.7% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|24.6% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|53.6% overvalued

RO

Community Contributor