Advertisement

- United States

- /

- Pharma

- /

- NasdaqCM:VYNE

VYNE Therapeutics (NASDAQ:VYNE) Will Have To Spend Its Cash Wisely

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you'd have done very well indeed. Having said that, unprofitable companies are risky because they could potentially burn through all their cash and become distressed.

Given this risk, we thought we'd take a look at whether VYNE Therapeutics (NASDAQ:VYNE) shareholders should be worried about its cash burn. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. We'll start by comparing its cash burn with its cash reserves in order to calculate its cash runway.

See our latest analysis for VYNE Therapeutics

When Might VYNE Therapeutics Run Out Of Money?

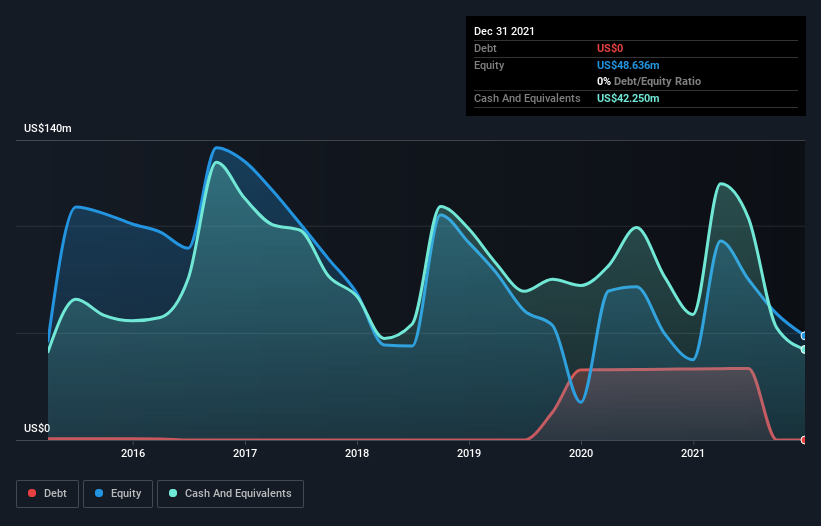

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. When VYNE Therapeutics last reported its balance sheet in December 2021, it had zero debt and cash worth US$42m. In the last year, its cash burn was US$72m. That means it had a cash runway of around 7 months as of December 2021. That's quite a short cash runway, indicating the company must either reduce its annual cash burn or replenish its cash. Depicted below, you can see how its cash holdings have changed over time.

How Well Is VYNE Therapeutics Growing?

We reckon the fact that VYNE Therapeutics managed to shrink its cash burn by 48% over the last year is rather encouraging. Unfortunately, however, operating revenue declined by 30% during the period. On balance, we'd say the company is improving over time. While the past is always worth studying, it is the future that matters most of all. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

How Hard Would It Be For VYNE Therapeutics To Raise More Cash For Growth?

Given VYNE Therapeutics' revenue is receding, there's a considerable chance it will eventually need to raise more money to spend on driving growth. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. Many companies end up issuing new shares to fund future growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

VYNE Therapeutics' cash burn of US$72m is about 184% of its US$39m market capitalisation. That suggests the company may have some funding difficulties, and we'd be very wary of the stock.

How Risky Is VYNE Therapeutics' Cash Burn Situation?

On this analysis of VYNE Therapeutics' cash burn, we think its cash burn reduction was reassuring, while its cash burn relative to its market cap has us a bit worried. After considering the data discussed in this article, we don't have a lot of confidence that its cash burn rate is prudent, as it seems like it might need more cash soon. On another note, VYNE Therapeutics has 5 warning signs (and 1 which is significant) we think you should know about.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:VYNE

VYNE Therapeutics

A clinical-stage biopharmaceutical company, focuses on developing therapies to treat chronic inflammatory and immune-mediated conditions.

Flawless balance sheet moderate.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor