Advertisement

- United States

- /

- Biotech

- /

- NasdaqGS:VRTX

Reassessing Vertex Pharmaceuticals After Pipeline Progress and Recent 7% Share Price Jump

Simply Wall St

Reviewed by Bailey Pemberton

- If you are wondering whether Vertex Pharmaceuticals at around $455 a share is still a smart buy or if the best days are already priced in, you are not alone.

- The stock has climbed 7.0% over the last week and 11.2% over the past month. It is still only up 12.3% year to date and is actually down 3.9% over the last year, despite a strong 45.0% three year and 99.7% five year run.

- Recent headlines have focused on Vertex's expanding pipeline in cystic fibrosis and non opioid pain, along with growing investor interest in its gene editing collaborations. At the same time, analysts are revisiting their long term growth assumptions as these programs move closer to key regulatory milestones. This helps explain the stock's latest swings.

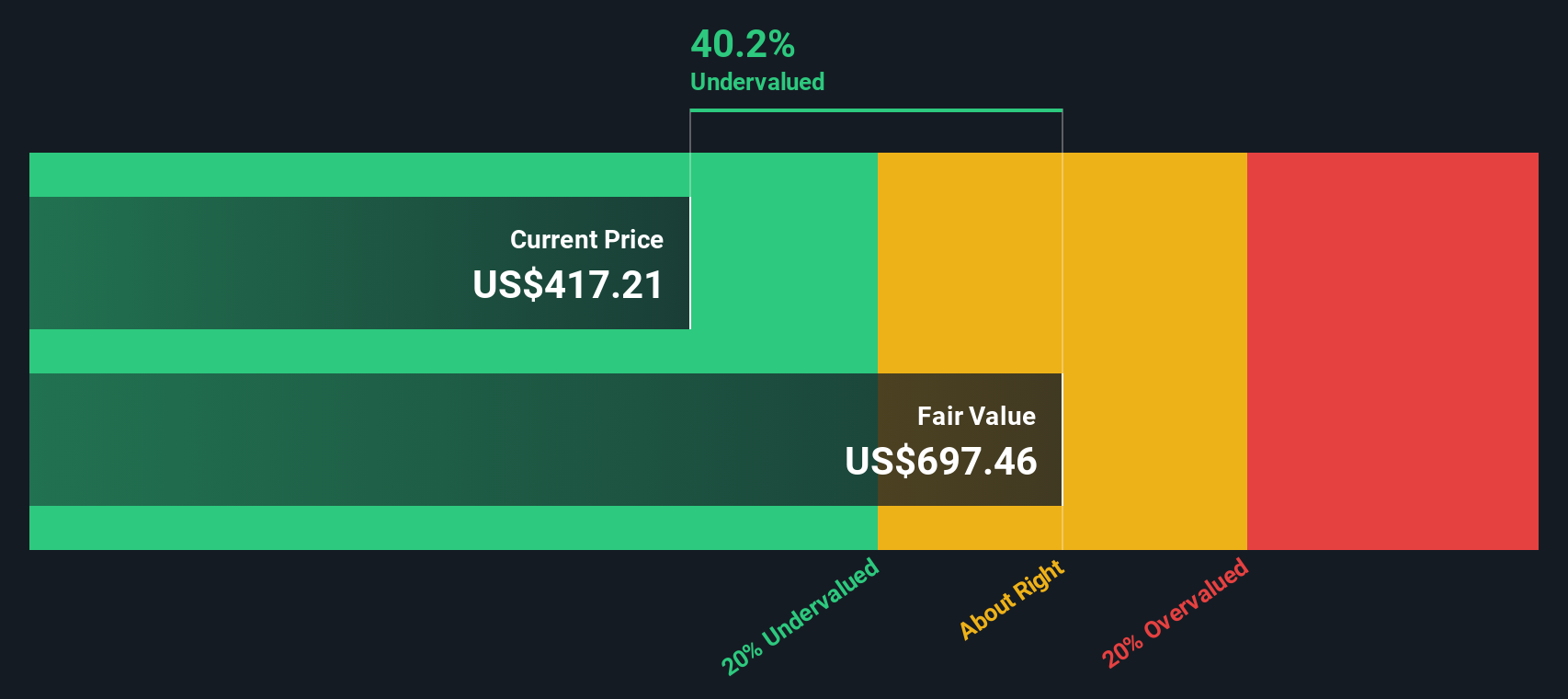

- On our valuation framework, Vertex scores a 3/6 for being undervalued. This suggests the market might be overlooking some of its strengths while still factoring in a fair bit of optimism. Next, we will break down what different valuation methods say about the stock today, and then finish with a broader way to think about its long term value.

Find out why Vertex Pharmaceuticals's -3.9% return over the last year is lagging behind its peers.

Approach 1: Vertex Pharmaceuticals Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it can generate in the future and discounting those cash flows back to today in dollar terms.

Vertex currently produces around $3.3 billion in free cash flow, and analysts expect this to climb steadily as its cystic fibrosis franchise expands and new therapies launch. Under the 2 Stage Free Cash Flow to Equity model, analyst forecasts are used for the next few years. After that point, Simply Wall St extrapolates further growth. By 2029, free cash flow is projected to reach roughly $6.7 billion, with longer term estimates rising toward about $9.5 billion by 2035.

When all these projected cash flows are discounted back to today, the model arrives at an intrinsic value of about $711 per share. Compared to the current share price around $455, the DCF suggests the stock is roughly 36.0% undervalued. This implies the market is not fully pricing in Vertex's future cash generation based on these assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Vertex Pharmaceuticals is undervalued by 36.0%. Track this in your watchlist or portfolio, or discover 905 more undervalued stocks based on cash flows.

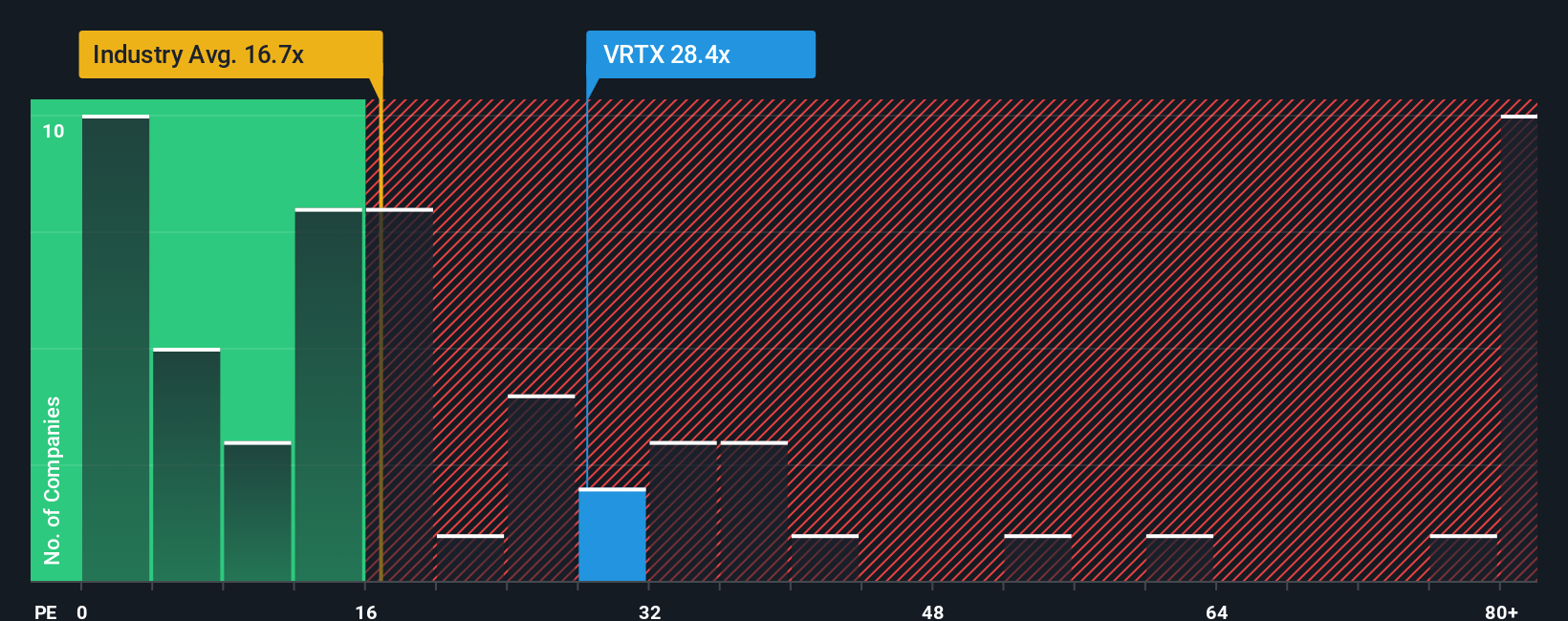

Approach 2: Vertex Pharmaceuticals Price vs Earnings

For a profitable business like Vertex, the price to earnings ratio is a useful way to gauge how much investors are willing to pay today for each dollar of current earnings. It naturally reflects what the market thinks about future growth and the level of risk in those earnings. Faster, more reliable growth usually justifies a higher PE, while slower or more uncertain growth tends to compress the multiple.

Vertex currently trades on a PE of about 31.4x, which is above the broader Biotechs industry average of roughly 19.1x but still well below the 57.5x average of its higher growth peers. Simply Wall St also calculates a Fair Ratio of 30.0x, which is the PE you would expect given Vertex's earnings growth profile, profitability, industry, size and specific risks. This tailored benchmark is more informative than a simple industry or peer comparison because it adjusts for the company’s own fundamentals rather than assuming one size fits all.

With the actual PE only slightly above the Fair Ratio, the multiple based view suggests that Vertex is priced close to its fundamental value.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1448 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Vertex Pharmaceuticals Narrative

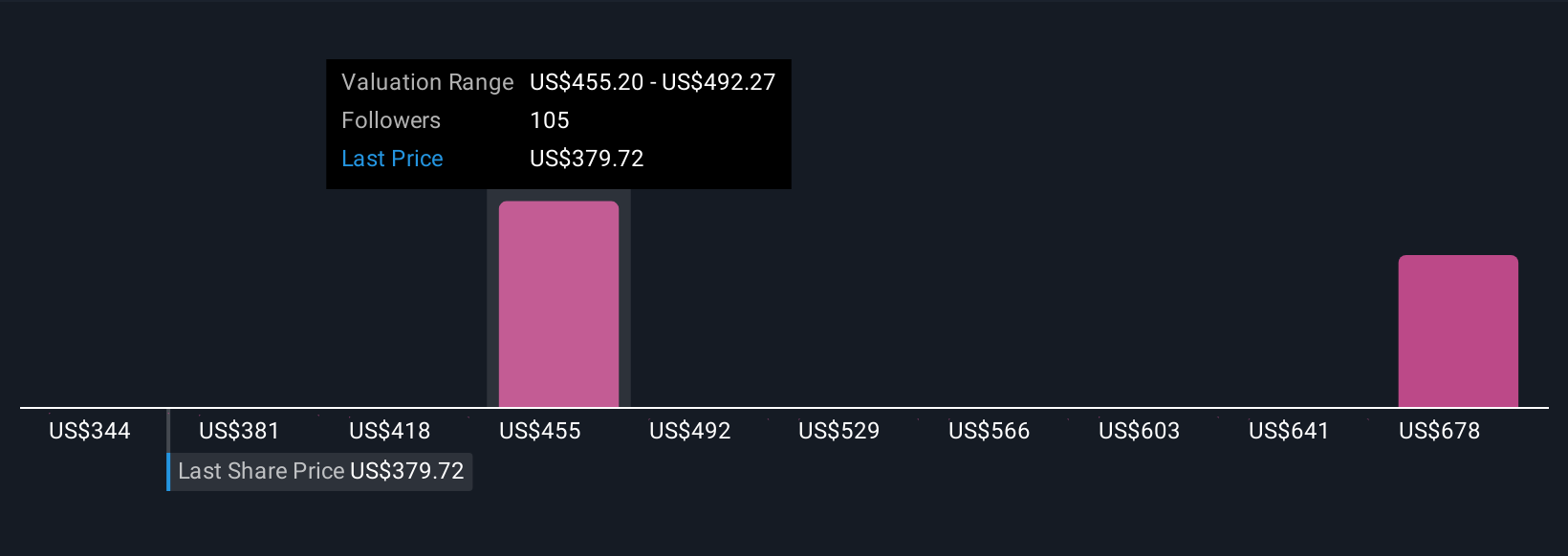

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple framework for connecting your view of a company with the numbers behind it.

A Narrative is your story about Vertex Pharmaceuticals, expressed through assumptions about its future revenue, earnings, and margins that then translate into a Fair Value estimate. Instead of only relying on a DCF or PE multiple, Narratives link the company’s business story, a clear financial forecast, and a valuation you can compare to today’s share price.

On Simply Wall St, Narratives are available in the Community page. Millions of investors can quickly build and share these story driven forecasts, then see at a glance whether their Fair Value suggests Vertex is a buy, hold, or sell versus the current market price.

Because Narratives update dynamically when fresh information arrives, such as new kidney trial data or changes to analyst targets, one investor might see Vertex worth around $330 per share while another believes the pipeline and gene editing opportunity justify a value closer to $616. Both perspectives can be explored and tested side by side.

Do you think there's more to the story for Vertex Pharmaceuticals? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:VRTX

Vertex Pharmaceuticals

A biotechnology company, engages in developing and commercializing therapies for treating cystic fibrosis (CF).

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

65 followersusers have followed this narrative

7 commentsusers have commented on this narrative

19 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Magma Silver ·

Silver's Breakout to over $50US will make Magma’s future shine with drill sampling returning 115g/t Silver and 2.3 g/t Gold at its Peru Mine

Fair Value:CA$0.3534.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on SEGRO ·

SEGRO's Revenue to Rise 14.7% Amidst Optimistic Growth Plans

Fair Value:UK£9.3924.7% undervalued

0 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PI

PicaCoder on Microsoft ·

After the AI Party: A Sobering Look at Microsoft's Future

Fair Value:US$42015.0% overvalued

62 followersusers have followed this narrative

12 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

958 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

65 followersusers have followed this narrative

7 commentsusers have commented on this narrative

19 likesusers have liked this narrative