Advertisement

- United States

- /

- Pharma

- /

- NasdaqGS:TLRY

Does Tilray’s Steep 2025 Share Price Slide Create a Long Term Opportunity?

Simply Wall St

Reviewed by Bailey Pemberton

- If you are wondering whether Tilray Brands is a bargain or a value trap at today’s price, you are not alone. This breakdown is designed to help you cut through the noise.

- The stock has slid sharply, down about 11.2% over the last week, 43.6% over the past month, and roughly 50.5% year to date. This has many investors questioning whether the market has overreacted or simply caught up with reality.

- Recently, Tilray has stayed in the headlines as investors weigh shifting cannabis regulations in the US and abroad alongside its ongoing push into beverages and consumer packaged goods. These developments, together with changing sentiment around the broader cannabis sector, help explain why the share price has been so volatile.

- Despite the slide, Tilray scores a solid 5/6 on our valuation checks, suggesting the stock screens as undervalued on most of the metrics we track. Next, we will walk through those approaches to see what they are really telling us about TLRY, before finishing with a more powerful way to think about valuation overall.

Find out why Tilray Brands's -43.6% return over the last year is lagging behind its peers.

Approach 1: Tilray Brands Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth today by projecting the cash it could generate in the future and discounting those cash flows back to their value in the present.

For Tilray Brands, the model starts from last twelve months Free Cash Flow of about $93.4 Million outflow, reflecting a business still investing heavily to reach consistent profitability. Analysts then forecast improving Free Cash Flow, with projections rising to about $43 Million by 2030. Further years are extrapolated by Simply Wall St using a 2 Stage Free Cash Flow to Equity approach to capture Tilray’s transition from negative to positive cash generation.

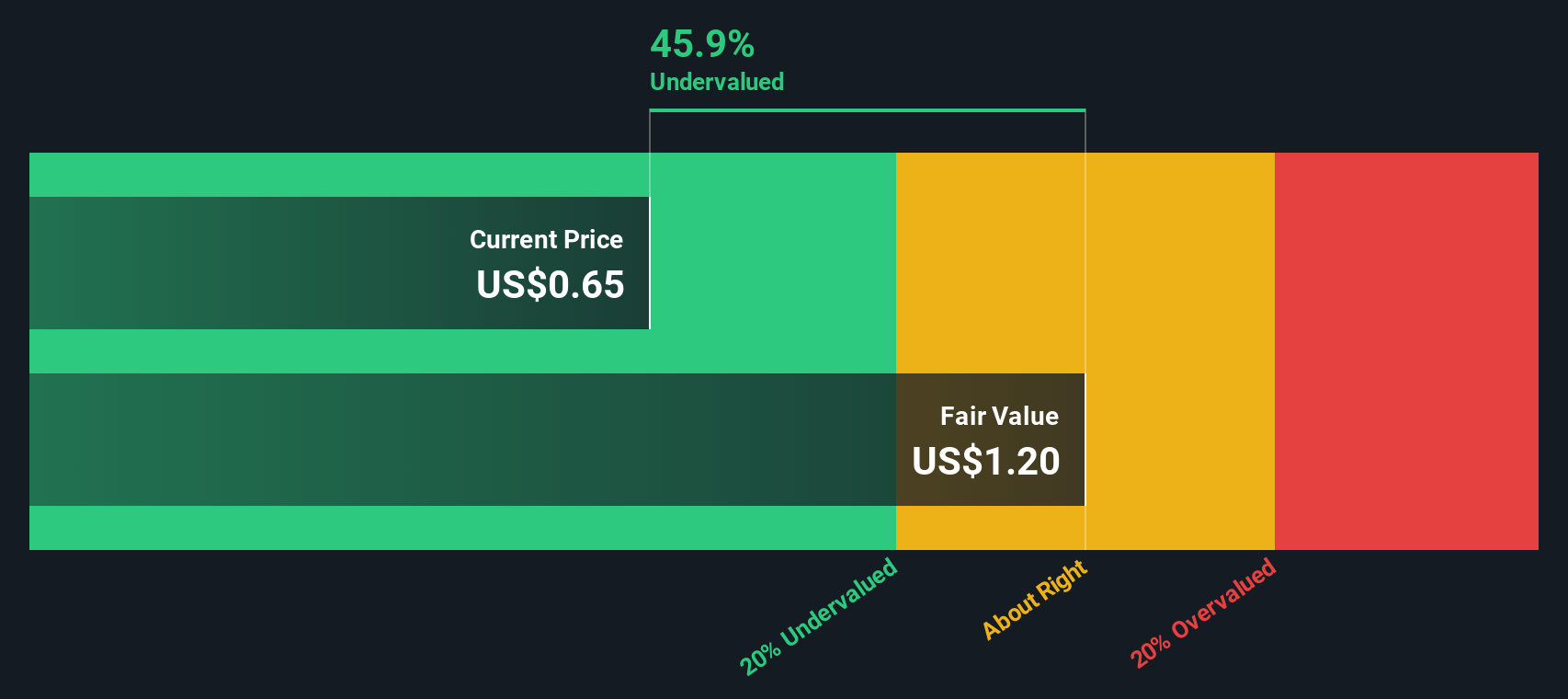

When all those future cash flows are discounted back to today, the model arrives at an intrinsic value of roughly $11.24 per share. Compared with the current market price, this implies the stock trades at about a 35.8% discount. This suggests investors are pricing in a much bleaker future than the cash flow projections assume.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Tilray Brands is undervalued by 35.8%. Track this in your watchlist or portfolio, or discover 912 more undervalued stocks based on cash flows.

Approach 2: Tilray Brands Price vs Sales

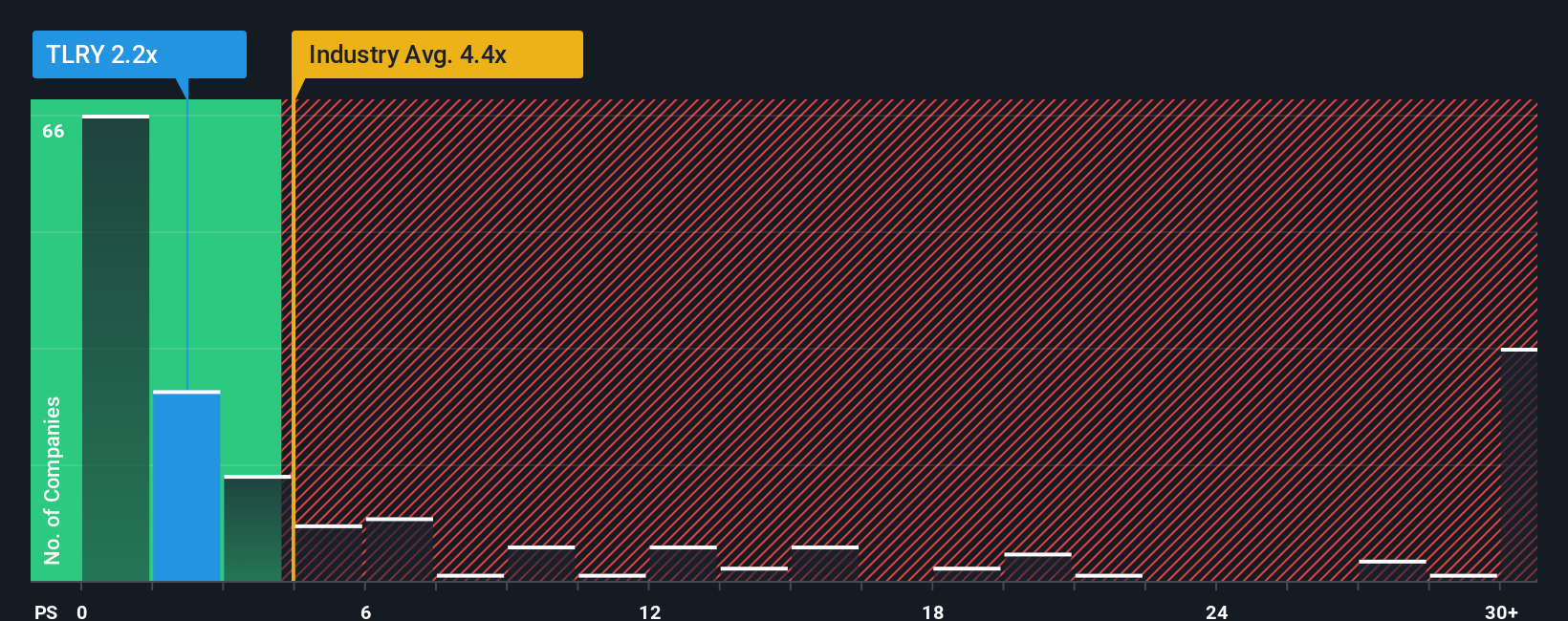

For companies like Tilray that are still working toward consistent profitability, the Price to Sales ratio is often a more useful yardstick than earnings based measures. It compares what investors are paying for each dollar of revenue, which can be more stable than profits during a turnaround.

In general, higher growth expectations and lower perceived risk justify a richer valuation multiple. Slower growth or higher uncertainty should translate into a lower, more conservative ratio. A “normal” or “fair” Price to Sales multiple will usually sit somewhere between those extremes, depending on how the market views a company’s prospects.

Tilray currently trades at about 1.0x sales, which is well below both the Pharmaceuticals industry average of around 4.0x and a peer group average near 4.4x. Simply Wall St’s proprietary Fair Ratio for Tilray is roughly 2.1x, reflecting what investors might reasonably pay once factors like expected growth, margins, industry, company size, and risk are taken into account. This Fair Ratio is more informative than a simple peer comparison because it adjusts for Tilray’s specific fundamentals rather than assuming it should match the typical sector stock. Compared with the current 1.0x, the 2.1x Fair Ratio suggests the shares may be attractively priced on a sales basis.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Tilray Brands Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of Tilray’s story with a concrete financial forecast and a clear fair value that you can compare to today’s share price.

On Simply Wall St’s Community page, Narratives let you spell out your assumptions about Tilray’s future revenue, earnings, and margins, then turn that story into a dynamic valuation that updates automatically as new earnings, regulatory news, or company developments are released.

This makes Narratives an easy, accessible decision tool, because you can quickly see whether your fair value estimate is above the current price, which may support considering a more positive stance, or below it, which may suggest holding off or reassessing your position.

For example, one Tilray Narrative might assume that federal policy shifts unlock strong U.S. opportunities and justify a fair value near $2.00 per share, while a more cautious Narrative, focused on regulatory and profitability risks, could anchor closer to $0.60, helping you decide which story best fits your own expectations and risk tolerance.

Do you think there's more to the story for Tilray Brands? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tilray Brands might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TLRY

Tilray Brands

A lifestyle consumer products company, engages in the research, cultivation, processing, and distribution of medical cannabis products in Canada, the United States, Europe, the Middle East, Africa, and internationally.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4729.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6410.8% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.8% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.71.9% undervalued

1341 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative