Advertisement

- United States

- /

- Life Sciences

- /

- NasdaqGS:TECH

Bio-Techne (TECH): Assessing Valuation After ACA Subsidy Extension Buzz Boosts Investor Sentiment

Investor sentiment around Bio-Techne (TECH) got a lift after news broke that the Trump administration may extend ACA subsidies for an additional two years. The announcement sparked a quick share price response and drew investor attention.

See our latest analysis for Bio-Techne.

Bio-Techne's share price has shown signs of renewed momentum lately, rebounding 18.1% over the past 90 days and 4.8% in the last week, helped by sector policy headlines and a series of upcoming investor presentations. Despite this, the one-year total shareholder return remains firmly negative, reflecting challenges the company continues to face over the longer term even as short-term sentiment looks brighter.

If the policy-driven volatility in healthcare is on your radar, you might also want to explore other sector leaders. See the full list in our Healthcare Stock Screener: See the full list for free.

With shares rebounding and policy shifts supporting sector optimism, investors are left wondering if Bio-Techne is still trading at a discount or if the market has already priced in every bit of future growth potential.

Most Popular Narrative: 6.7% Undervalued

Bio-Techne's last close of $64.51 sits below the narrative fair value of $69.17, drawing attention to the drivers that analysts believe could unlock further upside.

The company's shift in portfolio focus, highlighted by the divestiture of Exosome Diagnostics, allows redeployment of capital and resources toward higher-margin core business segments and growth pillars. This supports both immediate operating margin improvement (expected 100 to 200 basis point expansion) and higher future earnings. Accelerated innovation and product launches in automated proteomic instrumentation (such as Leo Simple Western and Maurice) and digital platforms are driving high-margin, high-throughput product adoption, increasingly embedding the company's solutions in regulated pharma manufacturing workflows. This is expected to improve product mix and the long-term net margin profile.

Inside the most-followed narrative, a bold transition is underway, powered by targeted divestments, margin-boosting upgrades, and new platform launches. Can you guess the key financial leap behind the upgraded fair value? One big projection ties these moving parts together. Find out what makes the upside case so compelling.

Result: Fair Value of $69.17 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing biotech funding challenges and new pharmaceutical tariffs could still disrupt Bio-Techne's growth trajectory and investor optimism in the near term.

Find out about the key risks to this Bio-Techne narrative.

Another View: Is TECH Priced for Perfection?

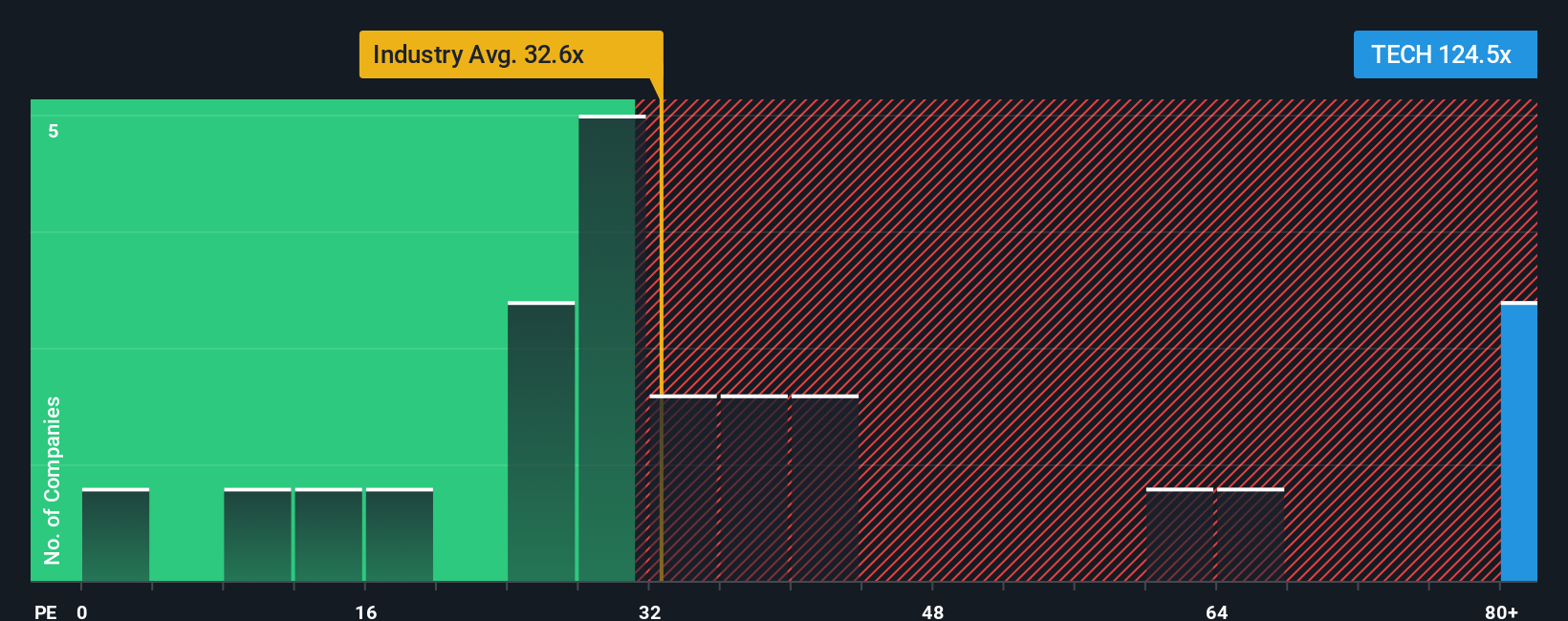

Taking a step back from fair value models and looking at TECH’s earnings ratio offers a different perspective. With a price-to-earnings ratio of 129x, the stock looks far more expensive than its North American Life Sciences peers at 37.9x, and even higher compared to the estimated fair ratio of 25.7x. This kind of gap signals that investors are betting heavily on future growth, leaving little room for error if results disappoint.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Bio-Techne Narrative

Keep in mind that if you have a different view, or want to explore the numbers on your own terms, building a personalized narrative takes just a few minutes. Do it your way.

A great starting point for your Bio-Techne research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Don’t let unique opportunities pass you by. Expand your research and strengthen your portfolio by checking out these different investment angles Simply Wall St has curated for you:

- Capitalize on untapped potential by scanning these 920 undervalued stocks based on cash flows stocks that might be trading at a fraction of their intrinsic value right now.

- Tap into the future of healthcare by evaluating these 30 healthcare AI stocks and see which companies are leading AI-driven breakthroughs in medicine.

- Unlock reliable income streams by reviewing these 15 dividend stocks with yields > 3% to find stocks offering yields above 3% for those who value steady returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bio-Techne might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TECH

Bio-Techne

Develops, manufactures, and sells life science reagents, instruments, and services for the research, diagnostics, and bioprocessing markets worldwide.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2542.1% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$482.3% overvalued

28 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5450.7% undervalued

50 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$825.3% undervalued

26 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

IN

inimosini on Lucky Cement ·

Discounted Cash Flow Valuation of Lucky Cement Limited (LUCK)

Fair Value:PK₨511.86.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PR

Premium_Bobcat_cwey on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6530.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Space Exploration Technologies ·

WHY YOU SHOULD NOT BUY THE SPACEX IPO

Fair Value:US$50224.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.1% undervalued

80 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9631.3% undervalued

63 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0544.6% undervalued

54 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative