Advertisement

- United States

- /

- Life Sciences

- /

- NasdaqGM:SLGC

Why Investors Shouldn't Be Surprised By SomaLogic, Inc.'s (NASDAQ:SLGC) P/S

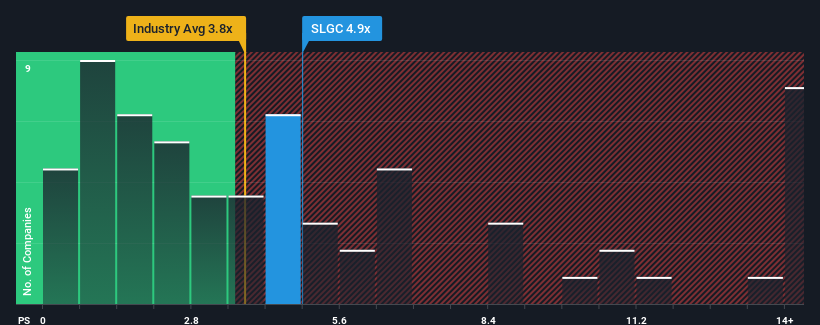

SomaLogic, Inc.'s (NASDAQ:SLGC) price-to-sales (or "P/S") ratio of 4.9x may not look like an appealing investment opportunity when you consider close to half the companies in the Life Sciences industry in the United States have P/S ratios below 3.8x. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for SomaLogic

How SomaLogic Has Been Performing

With revenue that's retreating more than the industry's average of late, SomaLogic has been very sluggish. One possibility is that the P/S ratio is high because investors think the company will turn things around completely and accelerate past most others in the industry. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on SomaLogic.Do Revenue Forecasts Match The High P/S Ratio?

In order to justify its P/S ratio, SomaLogic would need to produce impressive growth in excess of the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 20%. However, a few very strong years before that means that it was still able to grow revenue by an impressive 46% in total over the last three years. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been more than adequate for the company.

Looking ahead now, revenue is anticipated to climb by 18% each year during the coming three years according to the four analysts following the company. That's shaping up to be materially higher than the 4.6% per year growth forecast for the broader industry.

In light of this, it's understandable that SomaLogic's P/S sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Key Takeaway

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our look into SomaLogic shows that its P/S ratio remains high on the merit of its strong future revenues. Right now shareholders are comfortable with the P/S as they are quite confident future revenues aren't under threat. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

And what about other risks? Every company has them, and we've spotted 2 warning signs for SomaLogic you should know about.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:SLGC

Standard BioTools

SomaLogic, Inc. operates as a protein biomarker discovery and clinical diagnostics company in the United States.

Flawless balance sheet with concerning outlook.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor