Advertisement

- United States

- /

- Biotech

- /

- NasdaqCM:PRQR

New Forecasts: Here's What Analysts Think The Future Holds For ProQR Therapeutics N.V. (NASDAQ:PRQR)

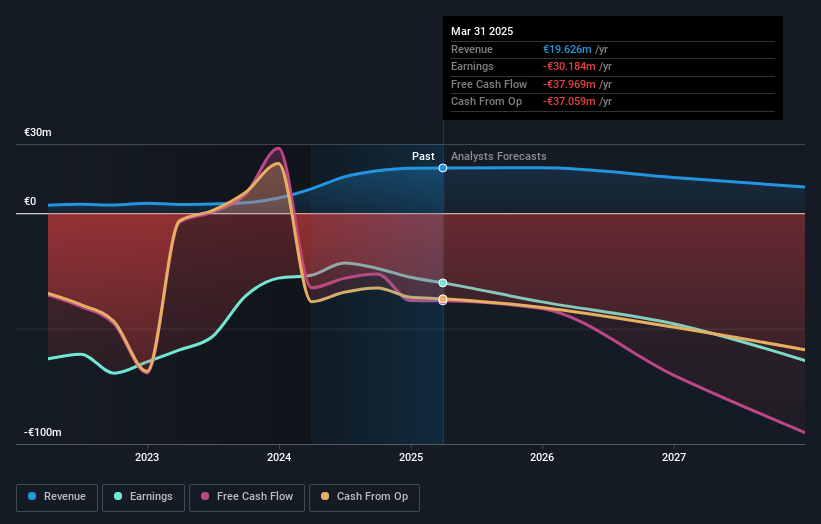

Celebrations may be in order for ProQR Therapeutics N.V. (NASDAQ:PRQR) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. The revenue forecast for this year has experienced a facelift, with analysts now much more optimistic on its sales pipeline.

Our free stock report includes 3 warning signs investors should be aware of before investing in ProQR Therapeutics. Read for free now.After the upgrade, the consensus from ProQR Therapeutics' seven analysts is for revenues of €19m in 2025, which would reflect a noticeable 5.4% decline in sales compared to the last year of performance. Per-share losses are expected to explode, reaching €0.38 per share. However, before this estimates update, the consensus had been expecting revenues of €17m and €0.40 per share in losses. It looks like there's been a modest increase in sentiment in the recent updates, with the analysts becoming a bit more optimistic in their predictions for both revenues and losses per share.

View our latest analysis for ProQR Therapeutics

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would highlight that sales are expected to reverse, with a forecast 7.1% annualised revenue decline to the end of 2025. That is a notable change from historical growth of 57% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 17% annually for the foreseeable future. It's pretty clear that ProQR Therapeutics' revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing here is that analysts reduced their loss per share estimates for this year, reflecting increased optimism around ProQR Therapeutics' prospects. Pleasantly, analysts also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow slower than the wider market. Given that analysts appear to be expecting substantial improvement in the sales pipeline, now could be the right time to take another look at ProQR Therapeutics.

Still, the long-term prospects of the business are much more relevant than next year's earnings. We have estimates - from multiple ProQR Therapeutics analysts - going out to 2027, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks with high insider ownership.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:PRQR

ProQR Therapeutics

A biotechnology company, focuses on the discovery and development of novel therapeutic medicines.

Flawless balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|40.2% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|62.7% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.1% undervalued

UN

Community Contributor