Advertisement

- United States

- /

- Pharma

- /

- OTCPK:PLXP.Q

Health Check: How Prudently Does PLx Pharma (NASDAQ:PLXP) Use Debt?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that PLx Pharma Inc. (NASDAQ:PLXP) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for PLx Pharma

What Is PLx Pharma's Debt?

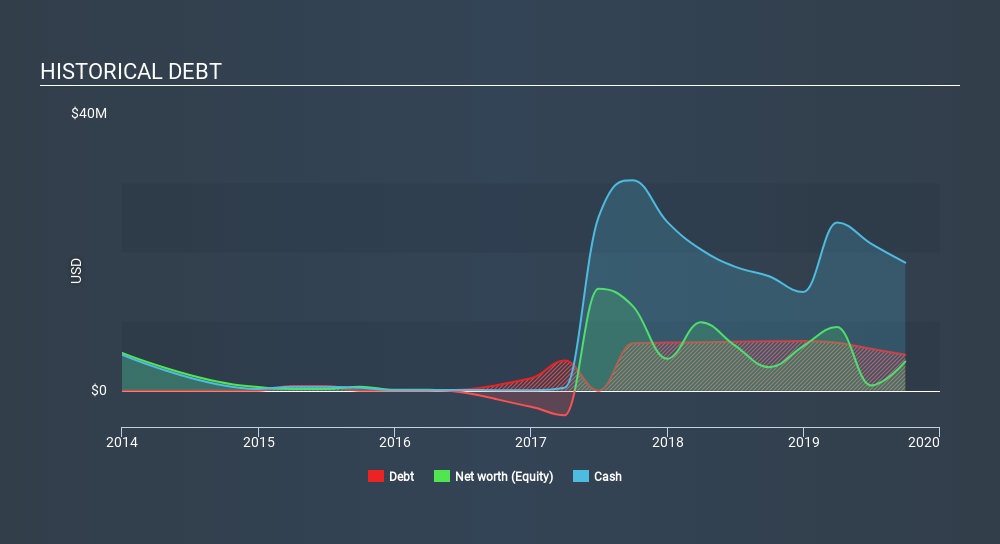

The image below, which you can click on for greater detail, shows that at September 2019 PLx Pharma had debt of US$5.18m, up from US$7.1 in one year. However, its balance sheet shows it holds US$18.5m in cash, so it actually has US$13.3m net cash.

A Look At PLx Pharma's Liabilities

We can see from the most recent balance sheet that PLx Pharma had liabilities of US$6.17m falling due within a year, and liabilities of US$12.6m due beyond that. Offsetting these obligations, it had cash of US$18.5m as well as receivables valued at US$193.7k due within 12 months. So these liquid assets roughly match the total liabilities.

This state of affairs indicates that PLx Pharma's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the US$42.6m company is struggling for cash, we still think it's worth monitoring its balance sheet. While it does have liabilities worth noting, PLx Pharma also has more cash than debt, so we're pretty confident it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine PLx Pharma's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Given it has no significant operating revenue at the moment, shareholders will be hoping PLx Pharma can make progress and gain better traction for the business, before it runs low on cash.

So How Risky Is PLx Pharma?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And the fact is that over the last twelve months PLx Pharma lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through US$11m of cash and made a loss of US$29m. However, it has net cash of US$13.3m, so it has a bit of time before it will need more capital. Overall, we'd say the stock is a bit risky, and we're usually very cautious until we see positive free cash flow. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 4 warning signs for PLx Pharma you should be aware of, and 1 of them shouldn't be ignored.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About OTCPK:PLXP.Q

PLx Pharma Winddown

PLx Pharma Winddown Corp. operates as a commercial-stage drug delivery platform technology company in the United States.

Adequate balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|43.0% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|30.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|18.3% undervalued

BL

Community Contributor