- United States

- /

- Life Sciences

- /

- OTCPK:NSTG.Q

Take Care Before Jumping Onto NanoString Technologies, Inc. (NASDAQ:NSTG) Even Though It's 42% Cheaper

The NanoString Technologies, Inc. (NASDAQ:NSTG) share price has fared very poorly over the last month, falling by a substantial 42%. For any long-term shareholders, the last month ends a year to forget by locking in a 62% share price decline.

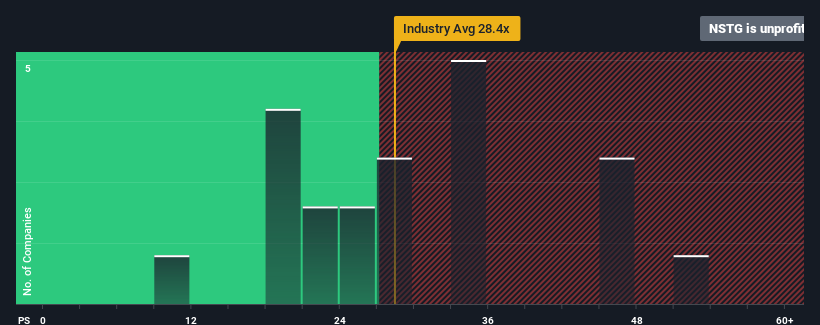

Since its price has dipped substantially, NanoString Technologies may be sending very bullish signals at the moment with its price-to-earnings (or "P/E") ratio of -1.8x, since almost half of all companies in the United States have P/E ratios greater than 15x and even P/E's higher than 30x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

While the market has experienced earnings growth lately, NanoString Technologies' earnings have gone into reverse gear, which is not great. The P/E is probably low because investors think this poor earnings performance isn't going to get any better. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

See our latest analysis for NanoString Technologies

Is There Any Growth For NanoString Technologies?

The only time you'd be truly comfortable seeing a P/E as depressed as NanoString Technologies' is when the company's growth is on track to lag the market decidedly.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 24%. Unfortunately, that's brought it right back to where it started three years ago with EPS growth being virtually non-existent overall during that time. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Looking ahead now, EPS is anticipated to climb by 15% per annum during the coming three years according to the seven analysts following the company. With the market only predicted to deliver 11% per annum, the company is positioned for a stronger earnings result.

In light of this, it's peculiar that NanoString Technologies' P/E sits below the majority of other companies. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

The Bottom Line On NanoString Technologies' P/E

Shares in NanoString Technologies have plummeted and its P/E is now low enough to touch the ground. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that NanoString Technologies currently trades on a much lower than expected P/E since its forecast growth is higher than the wider market. There could be some major unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. It appears many are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

You should always think about risks. Case in point, we've spotted 3 warning signs for NanoString Technologies you should be aware of.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

If you're looking to trade NS Wind Down, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if NS Wind Down might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OTCPK:NSTG.Q

NS Wind Down

Develops, manufactures, and sells technology for scientific and clinical information in the fields of genomics and proteomics in the Americas, Europe, the Middle East, and the Asia Pacific.

Slightly overvalued with weak fundamentals.

Similar Companies

Market Insights

Community Narratives