Advertisement

- United States

- /

- Biotech

- /

- NasdaqGM:MNKD

US$6.17: That's What Analysts Think MannKind Corporation (NASDAQ:MNKD) Is Worth After Its Latest Results

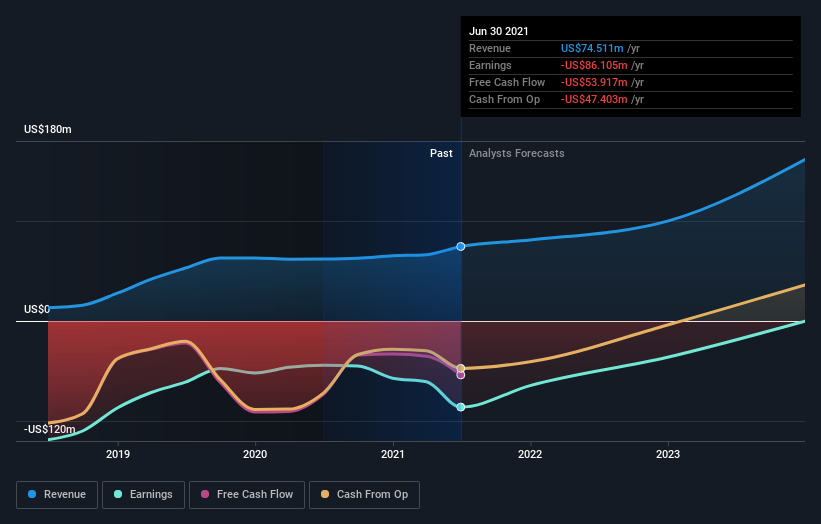

MannKind Corporation (NASDAQ:MNKD) came out with its second-quarter results last week, and we wanted to see how the business is performing and what industry forecasters think of the company following this report. Revenues of US$23m crushed expectations, although expenses also blew out, with the company reporting a statutory loss per share of US$0.14, 204% bigger than analysts expected. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

See our latest analysis for MannKind

Following the latest results, MannKind's six analysts are now forecasting revenues of US$81.0m in 2021. This would be a meaningful 8.7% improvement in sales compared to the last 12 months. The loss per share is expected to greatly reduce in the near future, narrowing 28% to US$0.26. Before this latest report, the consensus had been expecting revenues of US$77.9m and US$0.18 per share in losses. While this year's revenue estimates increased, there was also a very substantial increase in loss per share expectations, suggesting the consensus has a bit of a mixed view on the stock.

It will come as no surprise that expanding losses caused the consensus price target to fall 5.1% to US$6.17with the analysts implicitly ranking ongoing losses as a greater concern than growing revenues. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. Currently, the most bullish analyst values MannKind at US$8.00 per share, while the most bearish prices it at US$5.00. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. For example, we noticed that MannKind's rate of growth is expected to accelerate meaningfully, with revenues forecast to exhibit 18% growth to the end of 2021 on an annualised basis. That is well above its historical decline of 22% a year over the past five years. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 10% annually. Not only are MannKind's revenues expected to improve, it seems that the analysts are also expecting it to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts increased their loss per share estimates for next year. Happily, they also upgraded their revenue estimates, and are forecasting revenues to grow faster than the wider industry. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have estimates - from multiple MannKind analysts - going out to 2023, and you can see them free on our platform here.

However, before you get too enthused, we've discovered 3 warning signs for MannKind (1 is a bit unpleasant!) that you should be aware of.

When trading MannKind or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGM:MNKD

MannKind

A biopharmaceutical company, focuses on the development and commercialization of therapeutic products and services for endocrine and orphan lung diseases in the United States.

Solid track record with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor