Advertisement

- United States

- /

- Life Sciences

- /

- NasdaqGS:MEDP

Is Medpace (MEDP) Fairly Priced After Its Recent Pullback? A Fresh Look at Valuation

Simply Wall St

Reviewed by Simply Wall St

Medpace Holdings (MEDP) has pulled back about 6% over the past week and 8% this month, even after a strong year to date. That dip is prompting a closer look at the valuation setup.

See our latest analysis for Medpace Holdings.

Even after this sharp pullback, which includes a 1 day share price return of minus 5.5 percent and a 7 day share price return of minus 10.2 percent, Medpace’s 62.7 percent year to date share price return and hefty multi year total shareholder returns suggest momentum is cooling rather than breaking.

If Medpace’s run has you rethinking where the next leg of growth might come from, it could be worth scanning similar healthcare stocks that are also executing well.

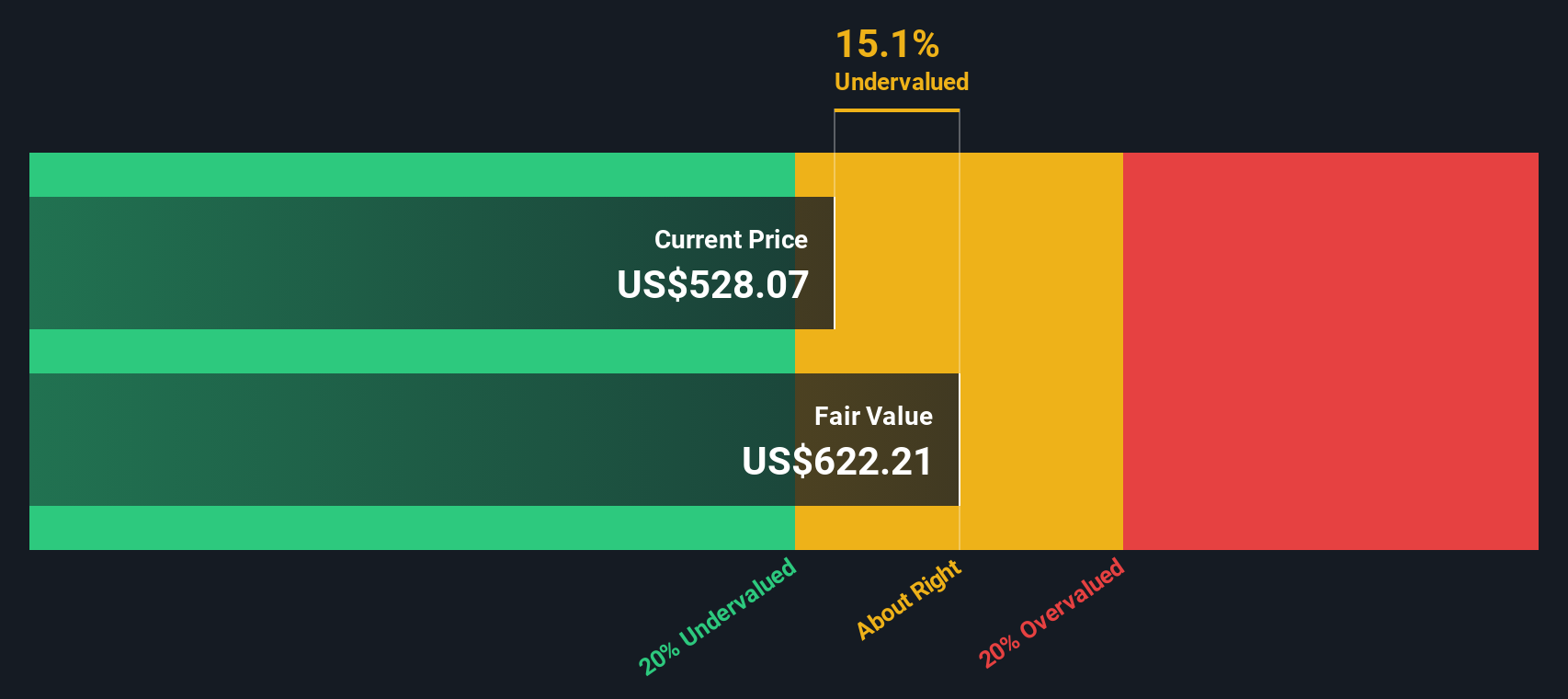

With shares still up strongly this year yet now trading below some intrinsic value estimates, investors face a key question: Is Medpace finally offering a compelling entry point, or is the market already pricing in its next chapter of growth?

Most Popular Narrative: 1.2% Overvalued

Medpace’s narrative fair value of $538.25 sits slightly below the last close of $544.77, setting up a finely balanced valuation debate.

Despite strong topline growth, win rates for new business were down and backlog is declining (-1.8% year over year). This suggests competitive pressures and a lack of large contract wins may negatively impact future bookings and limit revenue and earnings visibility beyond 2025. The company is guiding for accelerated hiring in the back half of 2025 to support the faster pace of trials. Combined with higher investigator and salary costs, this could increase operating expenses faster than underlying EBITDA if productivity gains plateau or reverse, exerting pressure on net margins.

Curious how modest margin compression, steady double digit growth, and a lower future earnings multiple still combine to justify this price tag? The full narrative unpacks the math driving this call.

Result: Fair Value of $538.25 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent trial demand and operational efficiency gains could sustain growth and margins longer than expected, which could undermine the cautious overvaluation narrative.

Find out about the key risks to this Medpace Holdings narrative.

Another View: SWS DCF Points to Upside

While the narrative fair value says Medpace is slightly overvalued, our DCF model suggests the opposite, with a fair value of $674.85 versus the current $544.77, implying roughly 19 percent upside. If future cash flows hold up, is the market underestimating the long term story?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Medpace Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 907 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Medpace Holdings Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a full narrative in just a few minutes: Do it your way

A great starting point for your Medpace Holdings research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Do not stop at one company. Use the Simply Wall St Screener today to find fresh opportunities before other investors notice them and identify the most attractive setups.

- Capture potential mispricing by reviewing these 907 undervalued stocks based on cash flows that may offer different upside than what the broader market currently expects.

- Explore the next wave of innovation by targeting these 26 AI penny stocks positioned at the forefront of artificial intelligence and automation.

- Adjust your income potential by focusing on these 15 dividend stocks with yields > 3% that can change your portfolio’s cash flow over time.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:MEDP

Medpace Holdings

Provides clinical research-based drug and medical device development services in North America, Europe, and Asia.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4729.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6410.8% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.8% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.71.9% undervalued

1341 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative