Advertisement

- United States

- /

- Pharma

- /

- NasdaqCM:LQDA

Analysts Are Updating Their Liquidia Corporation (NASDAQ:LQDA) Estimates After Its First-Quarter Results

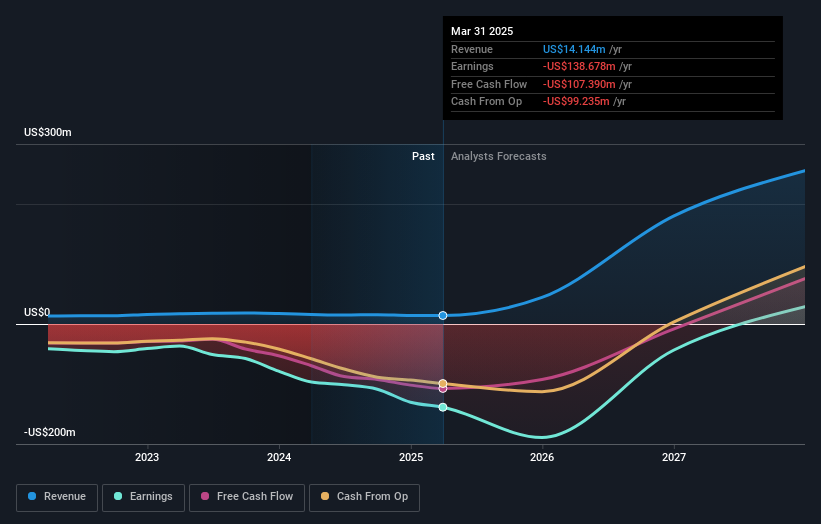

It's shaping up to be a tough period for Liquidia Corporation (NASDAQ:LQDA), which a week ago released some disappointing first-quarter results that could have a notable impact on how the market views the stock. Revenues missed expectations somewhat, coming in at US$3.1m and leading to a corresponding blowout in statutory losses. The loss per share was US$0.45, some 12% larger than the analysts forecast. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

Taking into account the latest results, the most recent consensus for Liquidia from nine analysts is for revenues of US$44.3m in 2025. If met, it would imply a major 213% increase on its revenue over the past 12 months. Losses are forecast to balloon 40% to US$2.27 per share. Yet prior to the latest earnings, the analysts had been forecasting revenues of US$43.6m and losses of US$1.57 per share in 2025. So it's pretty clear the analysts have mixed opinions on Liquidia even after this update; although they reconfirmed their revenue numbers, it came at the cost of a sizeable expansion in per-share losses.

Check out our latest analysis for Liquidia

As a result, there was no major change to the consensus price target of US$27.00, with the analysts implicitly confirming that the business looks to be performing in line with expectations, despite higher forecast losses. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. The most optimistic Liquidia analyst has a price target of US$36.00 per share, while the most pessimistic values it at US$20.00. As you can see, analysts are not all in agreement on the stock's future, but the range of estimates is still reasonably narrow, which could suggest that the outcome is not totally unpredictable.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. The analysts are definitely expecting Liquidia's growth to accelerate, with the forecast 4x annualised growth to the end of 2025 ranking favourably alongside historical growth of 26% per annum over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 8.3% annually. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Liquidia to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts increased their loss per share estimates for next year. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. The consensus price target held steady at US$27.00, with the latest estimates not enough to have an impact on their price targets.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have forecasts for Liquidia going out to 2027, and you can see them free on our platform here.

You can also see our analysis of Liquidia's Board and CEO remuneration and experience, and whether company insiders have been buying stock.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:LQDA

Liquidia

A biopharmaceutical company, develops, manufactures, and commercializes various products for unmet patient needs in the United States.

High growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.5% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.4% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|15.3% undervalued

MA

Community Contributor