- United States

- /

- Life Sciences

- /

- NasdaqGM:HBIO

Analysts Are Optimistic We'll See A Profit From Harvard Bioscience, Inc. (NASDAQ:HBIO)

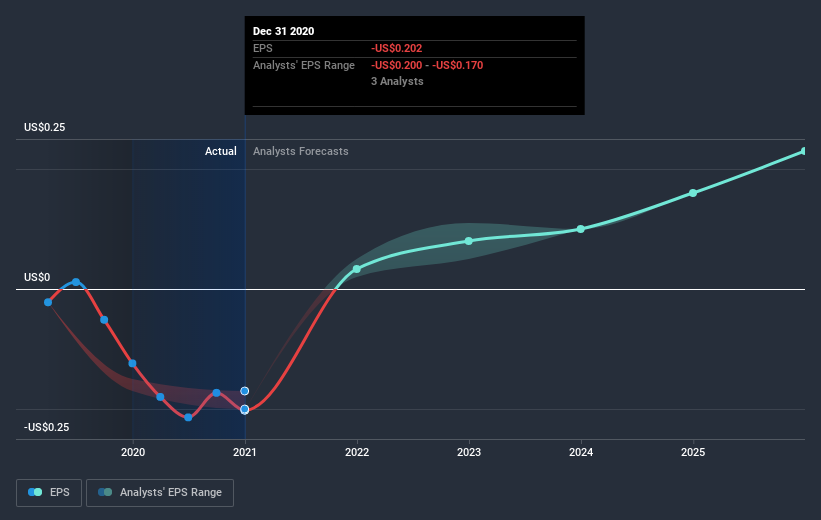

We feel now is a pretty good time to analyse Harvard Bioscience, Inc.'s (NASDAQ:HBIO) business as it appears the company may be on the cusp of a considerable accomplishment. Harvard Bioscience, Inc. develops, manufactures, and sells technologies, products, and services that enables fundamental research, discovery, and pre-clinical testing for drug development. On 31 December 2020, the US$217m market-cap company posted a loss of US$7.8m for its most recent financial year. Many investors are wondering about the rate at which Harvard Bioscience will turn a profit, with the big question being “when will the company breakeven?” In this article, we will touch on the expectations for the company's growth and when analysts expect it to become profitable.

View our latest analysis for Harvard Bioscience

According to the 3 industry analysts covering Harvard Bioscience, the consensus is that breakeven is near. They anticipate the company to incur a final loss in 2020, before generating positive profits of US$1.4m in 2021. Therefore, the company is expected to breakeven roughly a year from now or less! At what rate will the company have to grow in order to realise the consensus estimates forecasting breakeven in under 12 months? Using a line of best fit, we calculated an average annual growth rate of 59%, which is extremely buoyant. Should the business grow at a slower rate, it will become profitable at a later date than expected.

We're not going to go through company-specific developments for Harvard Bioscience given that this is a high-level summary, though, bear in mind that generally life science companies, depending on the stage of product development, have irregular periods of cash flow. This means, large upcoming growth rates are not abnormal as the company is beginning to reap the benefits of earlier investments.

Before we wrap up, there’s one issue worth mentioning. Harvard Bioscience currently has a relatively high level of debt. Generally, the rule of thumb is debt shouldn’t exceed 40% of your equity, which in Harvard Bioscience's case is 63%. Note that a higher debt obligation increases the risk around investing in the loss-making company.

Next Steps:

This article is not intended to be a comprehensive analysis on Harvard Bioscience, so if you are interested in understanding the company at a deeper level, take a look at Harvard Bioscience's company page on Simply Wall St. We've also compiled a list of relevant aspects you should further research:

- Valuation: What is Harvard Bioscience worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether Harvard Bioscience is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Harvard Bioscience’s board and the CEO’s background.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

If you decide to trade Harvard Bioscience, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Harvard Bioscience might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGM:HBIO

Harvard Bioscience

Develops, manufactures, and sells technologies, products, and services for life science applications in the United States and internationally.

Undervalued with excellent balance sheet.