Stock Analysis

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk'. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Exact Sciences Corporation (NASDAQ:EXAS) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Exact Sciences

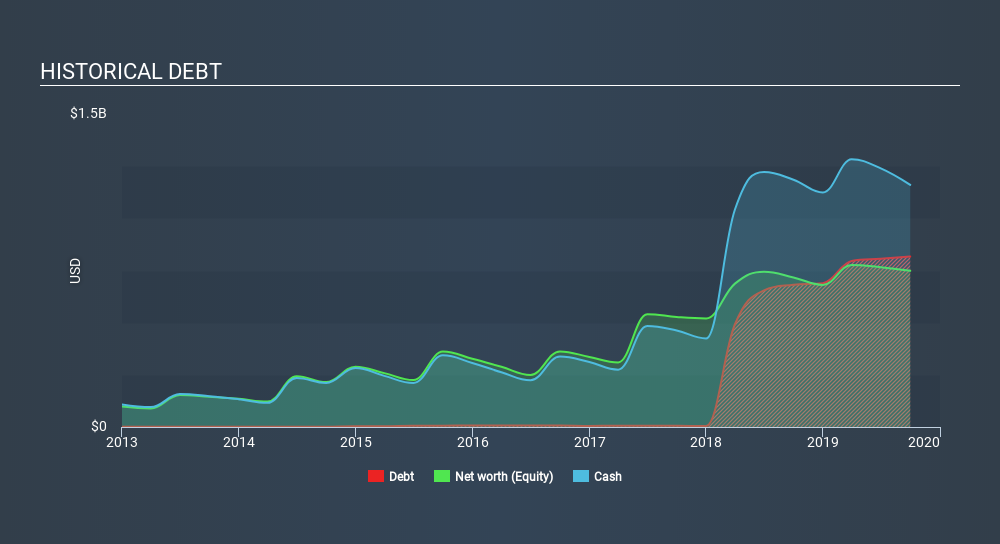

How Much Debt Does Exact Sciences Carry?

As you can see below, at the end of September 2019, Exact Sciences had US$817.0m of debt, up from US$681 a year ago. Click the image for more detail. But on the other hand it also has US$1.16b in cash, leading to a US$343.5m net cash position.

How Healthy Is Exact Sciences's Balance Sheet?

We can see from the most recent balance sheet that Exact Sciences had liabilities of US$480.7m falling due within a year, and liabilities of US$530.3m due beyond that. On the other hand, it had cash of US$1.16b and US$85.8m worth of receivables due within a year. So it actually has US$235.4m more liquid assets than total liabilities.

Having regard to Exact Sciences's size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the US$14.3b company is struggling for cash, we still think it's worth monitoring its balance sheet. Simply put, the fact that Exact Sciences has more cash than debt is arguably a good indication that it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 1 warning sign for Exact Sciences which any shareholder or potential investor should be aware of.

Over 12 months, Exact Sciences reported revenue of US$724m, which is a gain of 81%, although it did not report any earnings before interest and tax. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is Exact Sciences?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months Exact Sciences lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of US$272m and booked a US$216m accounting loss. While this does make the company a bit risky, it's important to remember it has net cash of US$343.5m. That means it could keep spending at its current rate for more than two years. With very solid revenue growth in the last year, Exact Sciences may be on a path to profitability. By investing before those profits, shareholders take on more risk in the hope of bigger rewards. For riskier companies like Exact Sciences I always like to keep an eye on the long term profit and revenue trends. Fortunately, you can click to see our interactive graph of its profit, revenue, and operating cashflow.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqCM:EXAS

Exact Sciences

Provides cancer screening and diagnostic test products in the United States and internationally.

Very undervalued with reasonable growth potential.