- United States

- /

- Pharma

- /

- NasdaqGM:AQST

Aquestive Therapeutics, Inc. (NASDAQ:AQST) Shares Slammed 27% But Getting In Cheap Might Be Difficult Regardless

Aquestive Therapeutics, Inc. (NASDAQ:AQST) shares have retraced a considerable 27% in the last month, reversing a fair amount of their solid recent performance. Looking at the bigger picture, even after this poor month the stock is up 39% in the last year.

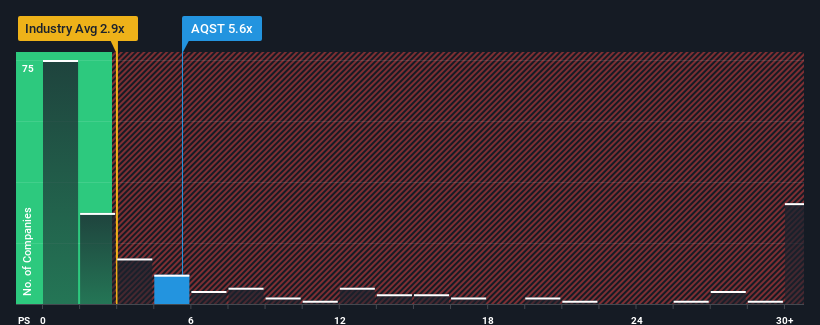

Although its price has dipped substantially, Aquestive Therapeutics may still be sending very bearish signals at the moment with a price-to-sales (or "P/S") ratio of 5.6x, since almost half of all companies in the Pharmaceuticals industry in the United States have P/S ratios under 2.9x and even P/S lower than 0.8x are not unusual. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

View our latest analysis for Aquestive Therapeutics

How Aquestive Therapeutics Has Been Performing

Recent times haven't been great for Aquestive Therapeutics as its revenue has been rising slower than most other companies. One possibility is that the P/S ratio is high because investors think this lacklustre revenue performance will improve markedly. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Keen to find out how analysts think Aquestive Therapeutics' future stacks up against the industry? In that case, our free report is a great place to start.Do Revenue Forecasts Match The High P/S Ratio?

Aquestive Therapeutics' P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

Retrospectively, the last year delivered a decent 11% gain to the company's revenues. The latest three year period has also seen a 6.8% overall rise in revenue, aided somewhat by its short-term performance. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

Shifting to the future, estimates from the nine analysts covering the company suggest revenue should grow by 22% per annum over the next three years. With the industry only predicted to deliver 17% each year, the company is positioned for a stronger revenue result.

With this in mind, it's not hard to understand why Aquestive Therapeutics' P/S is high relative to its industry peers. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Final Word

A significant share price dive has done very little to deflate Aquestive Therapeutics' very lofty P/S. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Aquestive Therapeutics maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Pharmaceuticals industry, as expected. Right now shareholders are comfortable with the P/S as they are quite confident future revenues aren't under threat. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

Before you settle on your opinion, we've discovered 4 warning signs for Aquestive Therapeutics (2 are concerning!) that you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:AQST

Aquestive Therapeutics

Operates as a pharmaceutical company in the United States and internationally.

Good value with limited growth.

Similar Companies

Market Insights

Community Narratives