Advertisement

- United States

- /

- Pharma

- /

- NasdaqGM:AQST

After Leaping 29% Aquestive Therapeutics, Inc. (NASDAQ:AQST) Shares Are Not Flying Under The Radar

Aquestive Therapeutics, Inc. (NASDAQ:AQST) shares have continued their recent momentum with a 29% gain in the last month alone. The last 30 days bring the annual gain to a very sharp 39%.

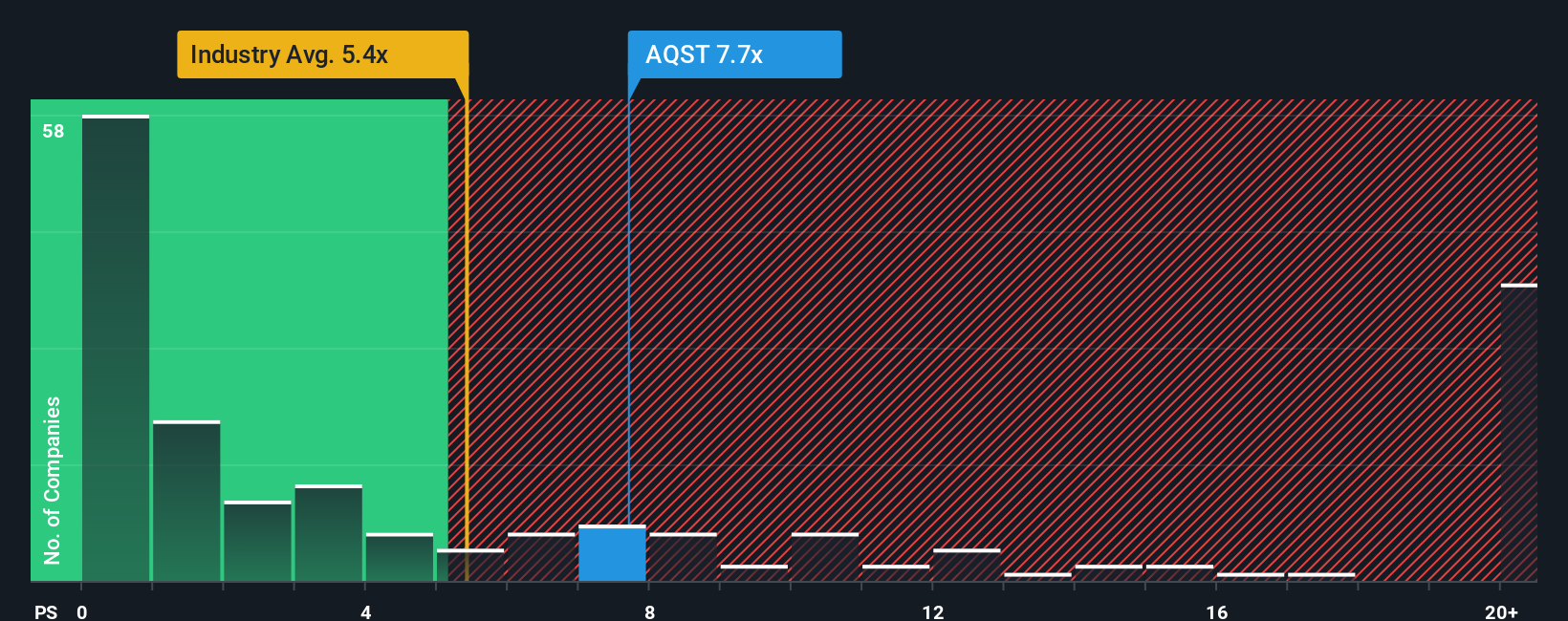

After such a large jump in price, Aquestive Therapeutics' price-to-sales (or "P/S") ratio of 7.7x might make it look like a sell right now compared to the wider Pharmaceuticals industry in the United States, where around half of the companies have P/S ratios below 5.4x and even P/S below 1.3x are quite common. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Aquestive Therapeutics

What Does Aquestive Therapeutics' Recent Performance Look Like?

Recent times haven't been great for Aquestive Therapeutics as its revenue has been rising slower than most other companies. Perhaps the market is expecting future revenue performance to undergo a reversal of fortunes, which has elevated the P/S ratio. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Aquestive Therapeutics will help you uncover what's on the horizon.Is There Enough Revenue Growth Forecasted For Aquestive Therapeutics?

The only time you'd be truly comfortable seeing a P/S as high as Aquestive Therapeutics' is when the company's growth is on track to outshine the industry.

Retrospectively, the last year delivered a decent 5.3% gain to the company's revenues. Still, revenue has barely risen at all in aggregate from three years ago, which is not ideal. Therefore, it's fair to say that revenue growth has been inconsistent recently for the company.

Shifting to the future, estimates from the nine analysts covering the company suggest revenue should grow by 28% per annum over the next three years. With the industry only predicted to deliver 18% per annum, the company is positioned for a stronger revenue result.

In light of this, it's understandable that Aquestive Therapeutics' P/S sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Bottom Line On Aquestive Therapeutics' P/S

Aquestive Therapeutics shares have taken a big step in a northerly direction, but its P/S is elevated as a result. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

As we suspected, our examination of Aquestive Therapeutics' analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Aquestive Therapeutics (at least 1 which is potentially serious), and understanding them should be part of your investment process.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:AQST

Aquestive Therapeutics

Operates as a pharmaceutical company in the United States and internationally.

Slightly overvalued with limited growth.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor