Advertisement

- United States

- /

- Biotech

- /

- NasdaqGS:ANAB

Upgrade: Analysts Just Made A Dazzling Increase To Their AnaptysBio, Inc. (NASDAQ:ANAB) Forecasts

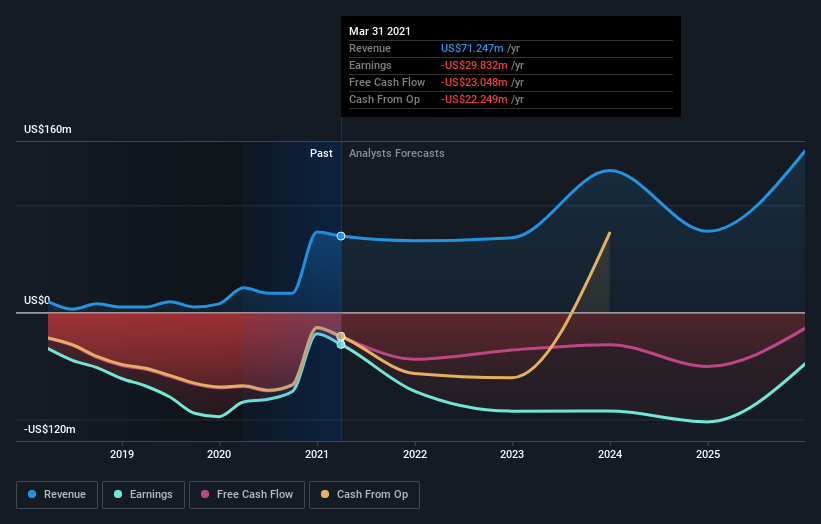

AnaptysBio, Inc. (NASDAQ:ANAB) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's statutory forecasts. The analysts greatly increased their revenue estimates, suggesting a stark improvement in business fundamentals. AnaptysBio has also found favour with investors, with the stock up a remarkable 12% to US$26.16 over the past week. We'll be curious to see if these new estimates convince the market to lift the stock price higher still.

Following the upgrade, the consensus from four analysts covering AnaptysBio is for revenues of US$67m in 2021, implying a discernible 6.1% decline in sales compared to the last 12 months. Per-share losses are expected to explode, reaching US$2.64 per share. Yet before this consensus update, the analysts had been forecasting revenues of US$48m and losses of US$3.01 per share in 2021. We can see there's definitely been a change in sentiment in this update, with the analysts administering a sizeable upgrade to this year's revenue estimates, while at the same time reducing their loss estimates.

Check out our latest analysis for AnaptysBio

The consensus price target rose 14% to US$29.80, with the analysts encouraged by the higher revenue and lower forecast losses for this year. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on AnaptysBio, with the most bullish analyst valuing it at US$50.00 and the most bearish at US$19.00 per share. So we wouldn't be assigning too much credibility to analyst price targets in this case, because there are clearly some widely differing views on what kind of performance this business can generate. As a result it might not be possible to derive much meaning from the consensus price target, which is after all just an average of this wide range of estimates.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. We would highlight that sales are expected to reverse, with a forecast 8.1% annualised revenue decline to the end of 2021. That is a notable change from historical growth of 31% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 14% annually for the foreseeable future. It's pretty clear that AnaptysBio's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing here is that analysts reduced their loss per share estimates for this year, reflecting increased optimism around AnaptysBio's prospects. Fortunately, they also upgraded their revenue estimates, and are forecasting revenues to grow slower than the wider market. With a serious upgrade to expectations and a rising price target, it might be time to take another look at AnaptysBio.

Still, the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for AnaptysBio going out to 2025, and you can see them free on our platform here..

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you decide to trade AnaptysBio, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGS:ANAB

AnaptysBio

A clinical-stage biotechnology company, focuses in delivering immunology therapeutics.

Slight risk and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.8% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.5% undervalued

GM

Community Contributor