Advertisement

- United States

- /

- Pharma

- /

- NasdaqGS:ACRS

Aclaris Therapeutics, Inc.'s (NASDAQ:ACRS) Shares Climb 25% But Its Business Is Yet to Catch Up

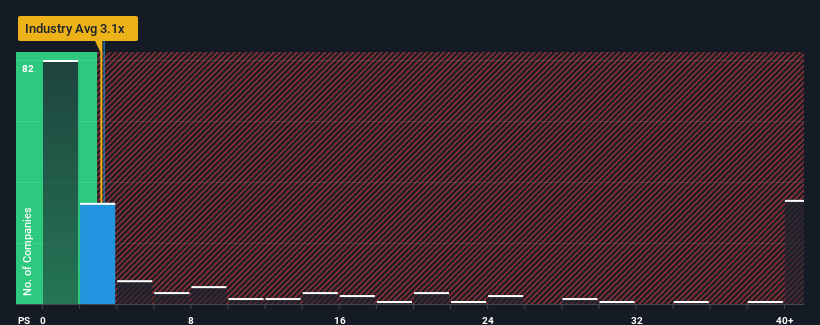

Despite an already strong run, Aclaris Therapeutics, Inc. (NASDAQ:ACRS) shares have been powering on, with a gain of 25% in the last thirty days. But the last month did very little to improve the 82% share price decline over the last year.

Although its price has surged higher, you could still be forgiven for feeling indifferent about Aclaris Therapeutics' P/S ratio of 3.3x, since the median price-to-sales (or "P/S") ratio for the Pharmaceuticals industry in the United States is also close to 3.1x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Check out our latest analysis for Aclaris Therapeutics

How Aclaris Therapeutics Has Been Performing

Aclaris Therapeutics could be doing better as it's been growing revenue less than most other companies lately. Perhaps the market is expecting future revenue performance to lift, which has kept the P/S from declining. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Aclaris Therapeutics.Is There Some Revenue Growth Forecasted For Aclaris Therapeutics?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Aclaris Therapeutics' to be considered reasonable.

If we review the last year of revenue growth, the company posted a worthy increase of 5.0%. Spectacularly, three year revenue growth has ballooned by several orders of magnitude, even though the last 12 months were fairly tame in comparison. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Looking ahead now, revenue is anticipated to slump, contracting by 32% per year during the coming three years according to the ten analysts following the company. With the industry predicted to deliver 41% growth per annum, that's a disappointing outcome.

With this in consideration, we think it doesn't make sense that Aclaris Therapeutics' P/S is closely matching its industry peers. Apparently many investors in the company reject the analyst cohort's pessimism and aren't willing to let go of their stock right now. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the negative growth outlook.

The Final Word

Its shares have lifted substantially and now Aclaris Therapeutics' P/S is back within range of the industry median. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

While Aclaris Therapeutics' P/S isn't anything out of the ordinary for companies in the industry, we didn't expect it given forecasts of revenue decline. When we see a gloomy outlook like this, our immediate thoughts are that the share price is at risk of declining, negatively impacting P/S. If the declining revenues were to materialize in the form of a declining share price, shareholders will be feeling the pinch.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 5 warning signs with Aclaris Therapeutics (at least 1 which doesn't sit too well with us), and understanding them should be part of your investment process.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:ACRS

Aclaris Therapeutics

A clinical-stage biopharmaceutical company, engages in the development of novel drug candidates for immune-inflammatory diseases in the United States.

Flawless balance sheet low.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|62.7% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor