- United States

- /

- Interactive Media and Services

- /

- NYSE:TWTR

These 4 Measures Indicate That Twitter (NYSE:TWTR) Is Using Debt Safely

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Twitter, Inc. (NYSE:TWTR) does use debt in its business. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Twitter

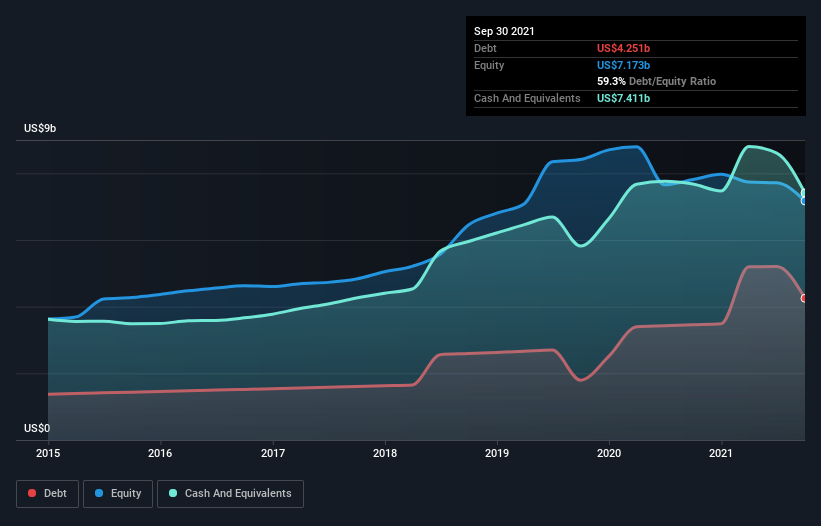

What Is Twitter's Net Debt?

The image below, which you can click on for greater detail, shows that at September 2021 Twitter had debt of US$4.25b, up from US$3.46b in one year. But it also has US$7.41b in cash to offset that, meaning it has US$3.16b net cash.

How Healthy Is Twitter's Balance Sheet?

We can see from the most recent balance sheet that Twitter had liabilities of US$2.11b falling due within a year, and liabilities of US$5.30b due beyond that. Offsetting this, it had US$7.41b in cash and US$1.01b in receivables that were due within 12 months. So it can boast US$1.01b more liquid assets than total liabilities.

This short term liquidity is a sign that Twitter could probably pay off its debt with ease, as its balance sheet is far from stretched. Simply put, the fact that Twitter has more cash than debt is arguably a good indication that it can manage its debt safely.

Even more impressive was the fact that Twitter grew its EBIT by 361% over twelve months. If maintained that growth will make the debt even more manageable in the years ahead. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Twitter's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While Twitter has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, Twitter actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing up

While it is always sensible to investigate a company's debt, in this case Twitter has US$3.16b in net cash and a decent-looking balance sheet. And it impressed us with free cash flow of US$324m, being 167% of its EBIT. So is Twitter's debt a risk? It doesn't seem so to us. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 2 warning signs for Twitter that you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Twitter might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:TWTR

Twitter, Inc. operates as a platform for public self-expression and conversation in real-time.

Mediocre balance sheet and slightly overvalued.