- United States

- /

- Entertainment

- /

- NYSE:TME

Tencent Music Entertainment Group (TME) Reports Q2 2025 Net Income of CNY 2,409 Million

Reviewed by Simply Wall St

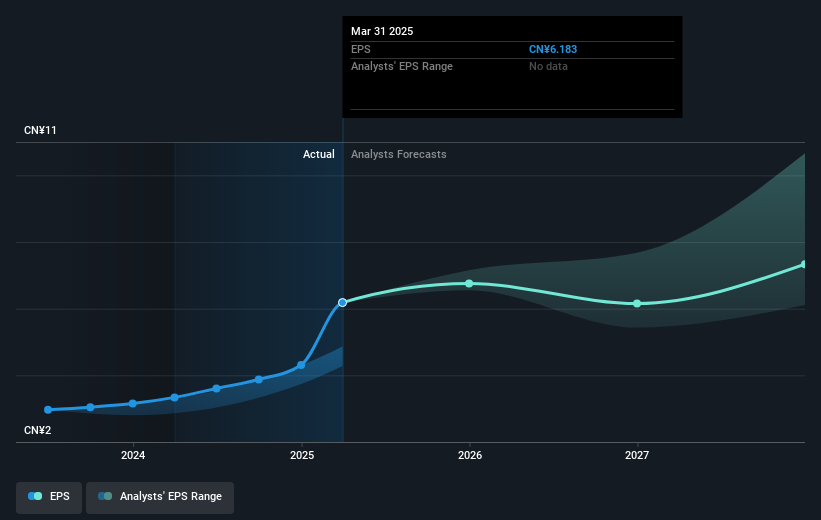

Tencent Music Entertainment Group (TME) recently reported significant earnings growth for Q2 2025, with revenues rising to CNY 8,442 million and net income reaching CNY 2,409 million, accompanied by a 56% increase in its share price over the last quarter. The earnings improvement reflects strong performance, which coincides with record highs in broader market indices and renewed optimism after promising consumer price data. Although inflation concerns and interest rate uncertainties continue to loom, the company's earnings release and the strategic management actions likely added weight to these broader market gains, supporting TME's notable price movement.

Tencent Music Entertainment Group's impressive earnings growth in Q2 2025 has aligned with a substantial share price surge of 56%. This financial performance is a testament to the company's dual-engine strategy, focusing on content and platform innovation to enhance user engagement and platform efficiency. Over the past three years, TME shareholders have seen a very large total return of 467.06%, underscoring the significant increase in shareholder value over this period.

Compared to the broader US market, TME has surpassed the annualized market return of 19.6%, reflecting its robust performance within the last year. The recent earnings growth and share price increase highlight the company's strong execution in expanding its SVIP memberships and leveraging AI technology, which could bolster future revenue streams and earnings forecasts. However, the current share price of US$25.60 closely aligns with the average analyst price target of US$26.18, suggesting limited upside potential in the near term.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Tencent Music Entertainment Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TME

Tencent Music Entertainment Group

Operates online music entertainment platforms that provides music streaming, online karaoke, and live streaming services in the People’s Republic of China.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion