Advertisement

- United States

- /

- Interactive Media and Services

- /

- NYSE:PINS

Does Pinterest’s Latest Valuation Signal Opportunity After Share Price Decline?

Simply Wall St

Reviewed by Bailey Pemberton

Wondering what to do with Pinterest stock right now? You are not alone. Investors have watched the company’s share price drift a bit lower in the past month, down 6.6%, despite being up 7.9% since the start of the year. Over the past three years, the stock boasts an impressive 49.7% climb, but if you zoom out to five years, it is actually down 33.0%. That kind of chart can make even the most confident investor pause and ask, what’s next?

It has been an interesting period for Pinterest, with waves of news that have nudged the stock back into the spotlight. Industry chatter about online advertising trends and new partnerships has mingled with ongoing debates about user growth, sparking fresh perspectives on the company’s risk and growth potential. While nothing lately has rocked the boat, this shifting context has made investors more aware of the company’s evolving story.

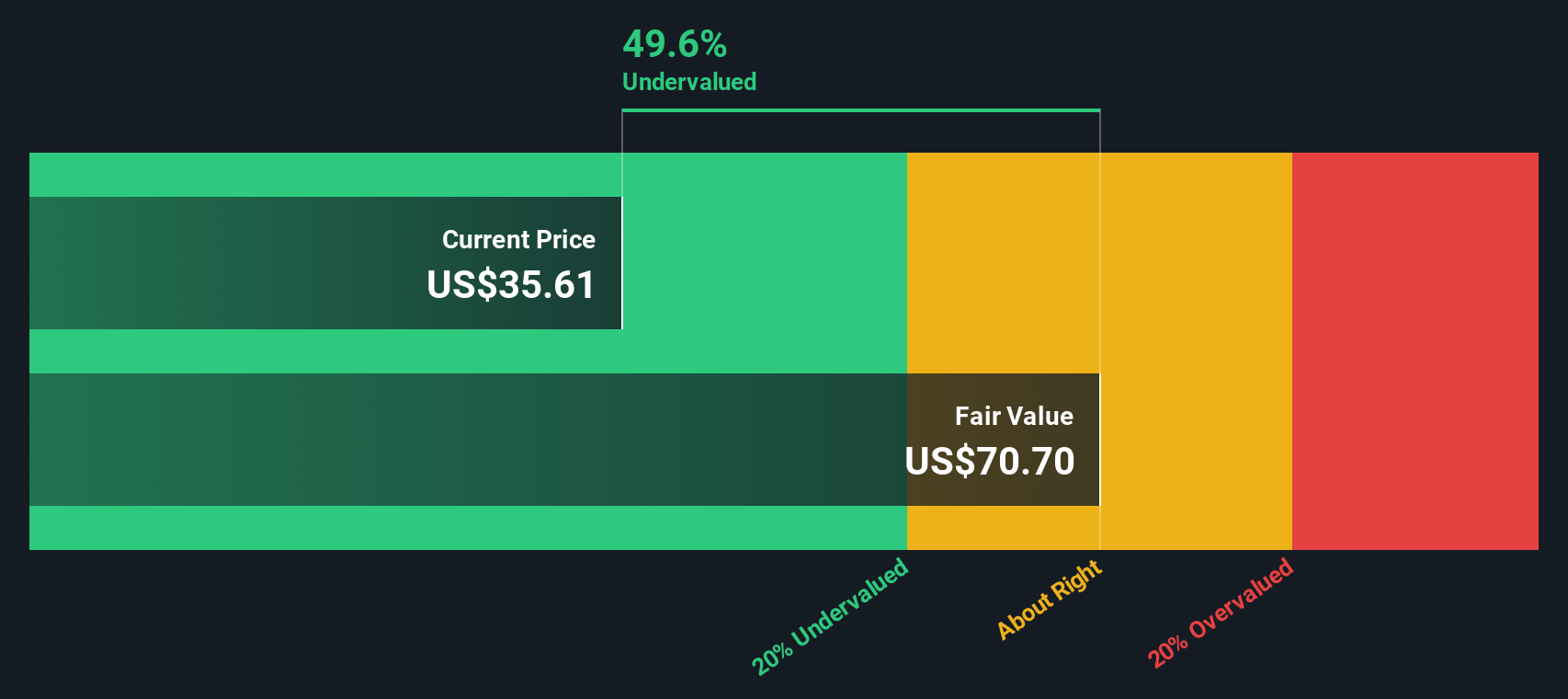

Here is the thing that may surprise you: by the numbers, Pinterest is looking distinctly undervalued based on a series of standard checks. The company scores a 6 out of 6 on our valuation scale, meaning it lands in the undervalued camp on every metric we look at. But before you make any moves, let’s break down these valuation methods and, more importantly, consider if there is an even smarter way to think about what the stock is really worth.

Why Pinterest is lagging behind its peers

Approach 1: Pinterest Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates what a business is worth by projecting its future cash flows and discounting them back to today’s dollars. In other words, it asks, how much are all of Pinterest's expected future profits worth right now?

For Pinterest, the DCF starts with its latest Free Cash Flow, which was a robust $1.05 Billion in the past twelve months. Looking ahead, analysts see Free Cash Flow climbing steadily. Projections suggest it will reach about $2.44 Billion by 2029, with interim years also showing strong growth. While expert estimates usually extend out just five years, Simply Wall St extrapolates further to offer a full decade’s outlook, balancing analyst confidence and historical trends.

When we run these cash flows through the DCF model, Pinterest lands an estimated intrinsic value of $72.77 per share. That is a striking 54.7% above the current share price, signaling significant undervaluation if these future growth projections hold.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Pinterest is undervalued by 54.7%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

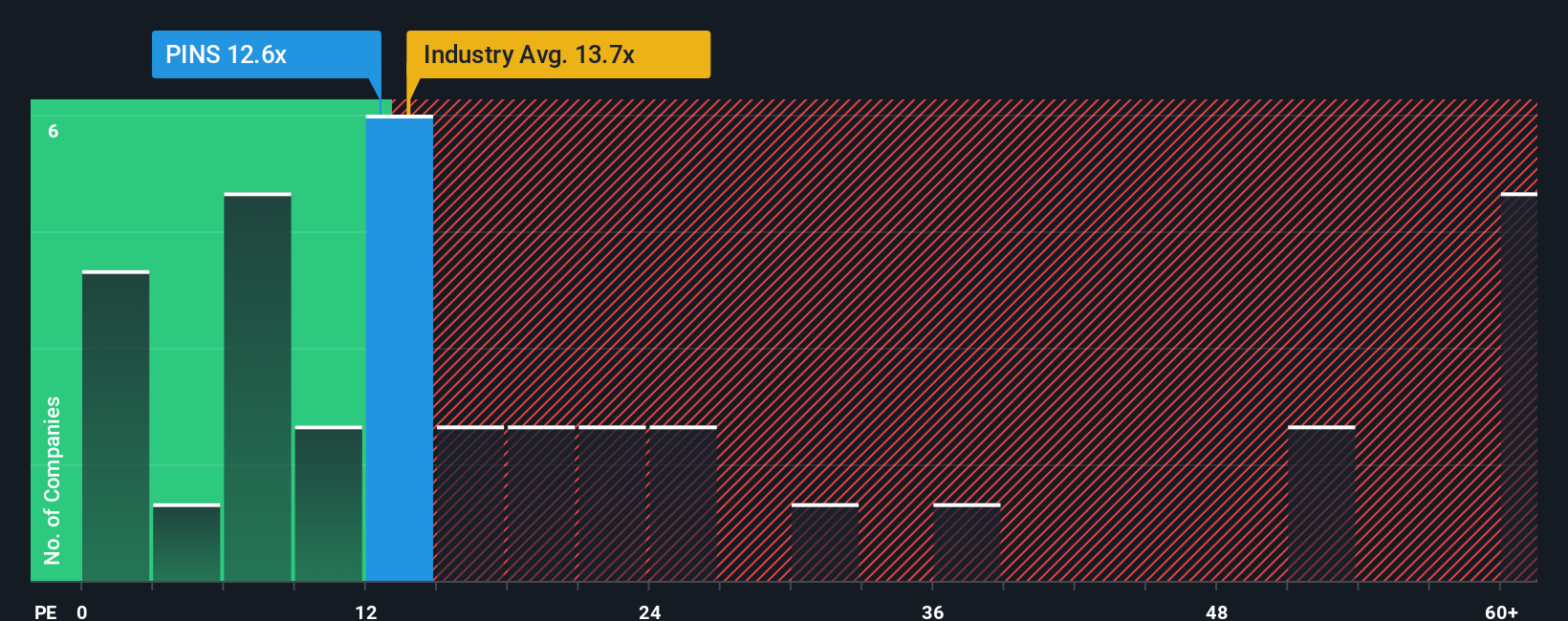

Approach 2: Pinterest Price vs Earnings

For a profitable company like Pinterest, the Price-to-Earnings (PE) ratio is a go-to valuation metric. It shows how much investors are willing to pay for each dollar of current earnings, which makes it a helpful way to compare companies within the same industry or against their own growth prospects.

It is important to remember that the "right" PE ratio depends not just on earnings but also on expectations for future growth and the risks the business faces. Higher growth companies can warrant higher PE ratios, while more risks or slower growth usually mean lower multiples.

Pinterest currently trades at a PE ratio of 11.6x. That is noticeably lower than both the interactive media industry average of 15.6x and the peer group average of 58.7x. At first glance, this gap suggests Pinterest could be undervalued, but those numbers alone can be misleading if they do not properly reflect the company's unique prospects and risk profile.

This is where Simply Wall St’s "Fair Ratio" comes in. The Fair Ratio for Pinterest is calculated at 17.1x, which is custom-built to reflect its specific earnings growth, profit margins, industry dynamics, market size, and risk factors. Unlike simple peer or industry comparisons, this approach weighs what actually matters for the business right now and looking forward.

Comparing Pinterest’s actual PE of 11.6x to the Fair Ratio of 17.1x suggests the stock is undervalued versus what you would reasonably expect given its outlook and fundamentals.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

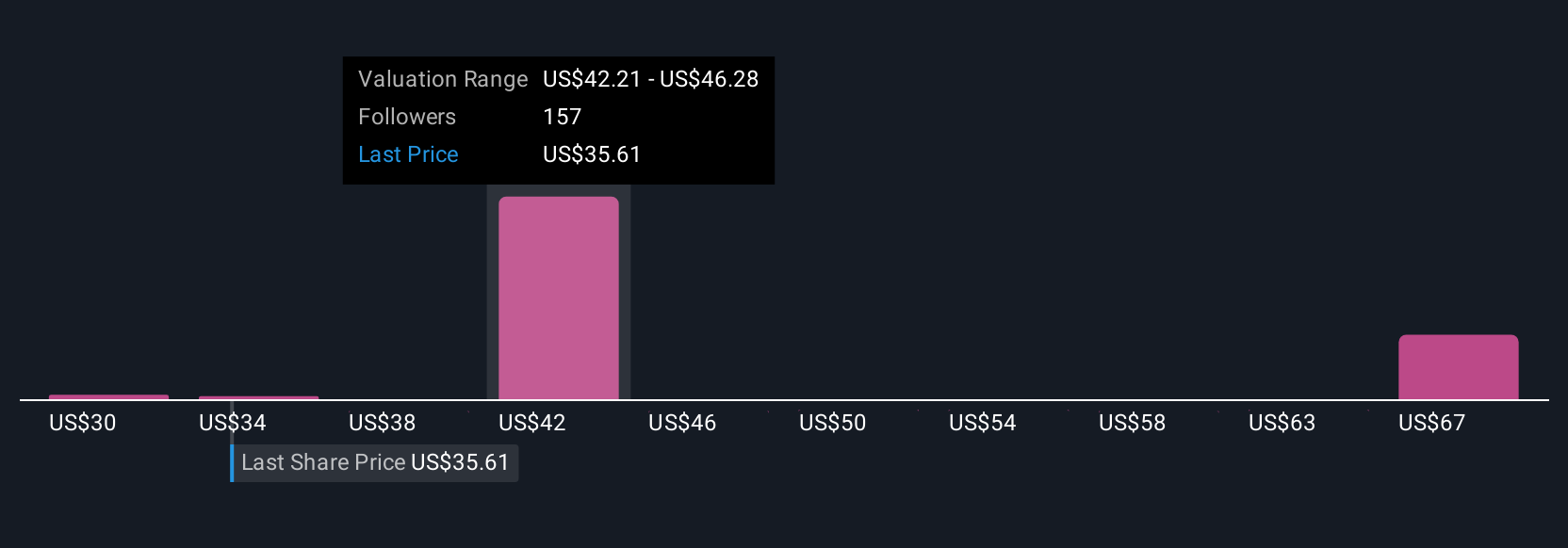

Upgrade Your Decision Making: Choose your Pinterest Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. Rather than relying solely on rigid models or one-size-fits-all ratios, Narratives allow investors to bring together the full story behind a company by combining their perspective on Pinterest’s future (like growth drivers, competitive strengths, and risks) with what those assumptions mean for future revenue, earnings, and ultimately, fair value.

A Narrative is your investment thesis brought to life: it ties the facts and forecasts into a clear financial picture and then directly shows you whether the current price looks attractive or stretched, based on your view. On Simply Wall St's Community page, Narratives are easy to explore and create, enabling users of all experience levels to test and share their ideas. Millions already do.

Because Narratives update instantly when new earnings or news arrives, they help you stay grounded in the latest information and know exactly when to revisit your stance. For example, one user’s Narrative projects a fair value for Pinterest of $43.58 per share based on strong international expansion and rising margins, while another, more cautious about future risks, estimates fair value at $37.68. This makes it easy to see the real range of well-argued viewpoints, compare them to the current market price, and act accordingly with confidence.

Do you think there's more to the story for Pinterest? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PINS

Operates as a visual search and discovery platform in the United States, Canada, Europe, and internationally.

Very undervalued with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.5% undervalued

GM

Community Contributor