Advertisement

- United States

- /

- Entertainment

- /

- NasdaqGS:TTWO

Take-Two Interactive Software (TTWO): How Does Strong Earnings and Guidance Impact Its Valuation?

Reviewed by Kshitija Bhandaru

Take-Two Interactive Software (TTWO) has the market’s attention after the company exceeded Wall Street expectations in its recent quarterly report. Adjusted earnings per share came in at $0.61, more than double what analysts had forecast, with revenue climbing over 12% compared to last year. The board’s confidence was apparent in upbeat full-year revenue guidance, a move that is generating conversation around the video game publisher and what could come next for the stock.

This positive news has fueled a sharp move in Take-Two’s share price, with the stock rising nearly 10% over the past month and significantly outperforming the broader Consumer Discretionary sector. Investors have observed a steady trend: over the past year, the stock delivered a total return of 62%, while the three-year gain reached 97%. With this momentum, Take-Two’s financial performance is beginning to look like more than just a short-term increase. It reflects tangible business progress amid rising expectations for future growth.

So after such a strong run following these results, is Take-Two a bargain with more room to climb, or is the market already factoring all the positive news into the current price?

Most Popular Narrative: 4.3% Undervalued

According to the most widely followed valuation narrative, Take-Two is currently trading below its estimated fair value. This suggests modest upside remains for investors who buy at current prices.

Take-Two's mobile portfolio is experiencing outsized growth through direct-to-consumer initiatives, enhanced personalization, new event-driven features, and benefits from broader access provided by high-speed internet and mobile penetration. These trends are likely lifting both net revenue and margins as distribution costs decline.

Want to know the growth blueprint behind this analyst valuation? The narrative leans on aggressive future earnings, rising profit margins, and a longer-term multiple worthy of industry standouts. What underlying numbers are fueling this calculated optimism? Dive in to uncover the key financial assumptions that anchor this fair value estimate.

Result: Fair Value of $262.02 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, the outlook remains vulnerable, especially if major franchise releases underperform or if shifting gamer habits erode premium game engagement.

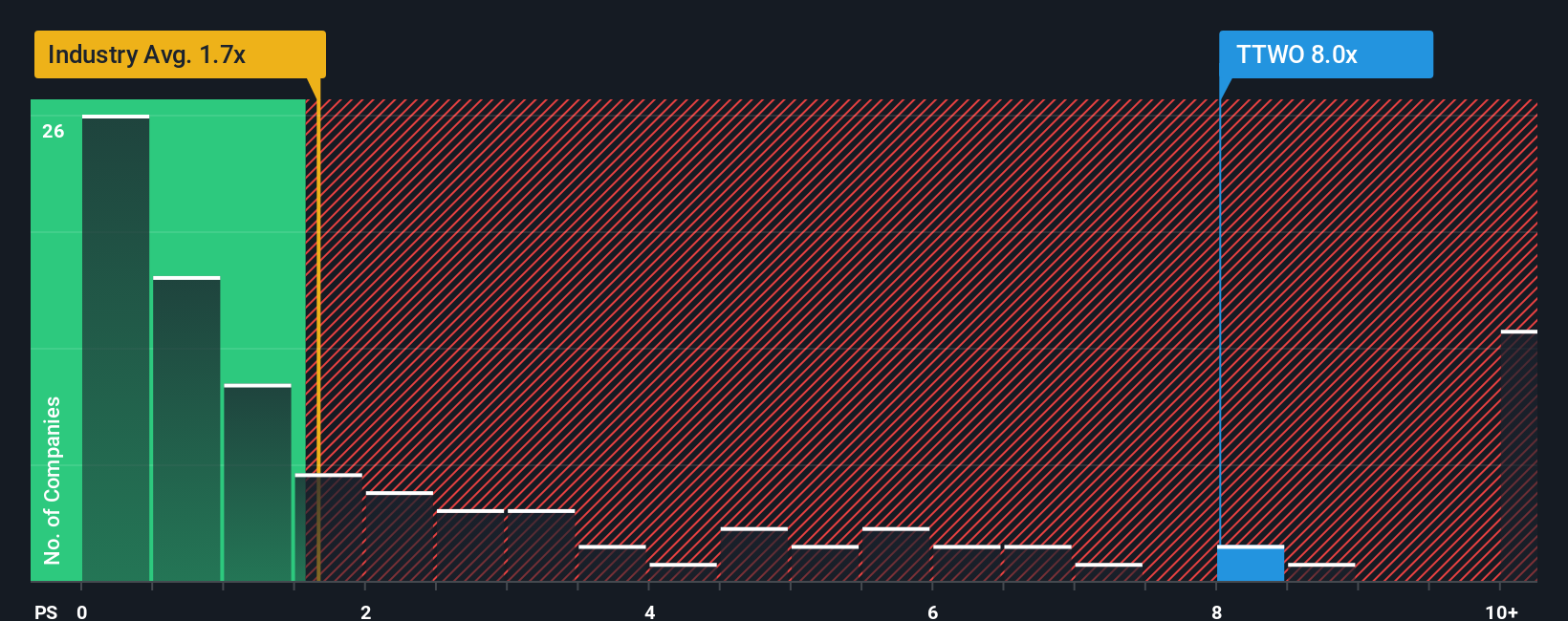

Find out about the key risks to this Take-Two Interactive Software narrative.Another View: Market Compares Differently

While the fair value estimate offers optimism, a look at how the market values Take-Two compared to the broader industry tells a different story. This approach suggests shares may be priced well above industry norms. Is the optimism already factored in, or is something being missed?

See what the numbers say about this price — find out in our valuation breakdown.

Stay updated when valuation signals shift by adding Take-Two Interactive Software to your watchlist or portfolio. Alternatively, explore our screener to discover other companies that fit your criteria.

Build Your Own Take-Two Interactive Software Narrative

If you want to dig deeper or reach your own conclusions, you can dive into the numbers and build a personalized narrative in just a few minutes by using Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Take-Two Interactive Software.

Looking for More Investment Ideas?

Don't let exciting opportunities slip by. The Simply Wall St Screener helps you tap into overlooked gems, tech breakthroughs, and income powerhouses ready for smart investors like you.

- Spot undervalued potential and gain an edge in the market by starting with undervalued stocks based on cash flows.

- Pursue high-yielding income streams and discover stocks offering robust dividends through dividend stocks with yields > 3%.

- Identify momentum in disruptive technologies transforming industries by searching for tomorrow’s winners with AI penny stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Take-Two Interactive Software might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TTWO

Take-Two Interactive Software

Develops, publishes, and markets interactive entertainment solutions for consumers worldwide.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8210.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5296.9% undervalued

4 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

Faltaren on AmpliTech Group ·

AmpliTech Group Will Triple Revenue by 2030 with O-RAN Expansion

Fair Value:US$3078.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative