Advertisement

- United States

- /

- Entertainment

- /

- NasdaqGS:TTWO

Is Take Two Interactive (TTWO) Now Attractive After Recent Share Price Pullback?

Reviewed by Bailey Pemberton

- If you are wondering whether Take-Two Interactive Software's current share price lines up with its underlying worth, this article will walk through what the numbers are really saying about value.

- The stock last closed at US$193.24 after a 19.2% decline over the past week and a 24.0% decline over the past month, even though the 1 year return sits at 5.5% and the 3 year return at 74.3%.

- These moves have come as attention has stayed on Take-Two's position in major gaming franchises and its broader role in the video game industry. This has kept investors focused on how durable its portfolio may be. Together, this context helps frame whether recent share price swings reflect changing sentiment on risk, long term potential, or both.

- Right now, Take-Two has a valuation score of 2 out of 6, which means it screens as undervalued on two of Simply Wall St's standard checks. Next, we will walk through what those traditional valuation methods miss and a more complete way to think about the stock's value.

Take-Two Interactive Software scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Take-Two Interactive Software Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes expected future cash flows, discounts them back to today using a required rate of return, and adds them up to estimate what the business might be worth right now.

For Take-Two Interactive Software, Simply Wall St uses a 2 Stage Free Cash Flow to Equity model based on cash flow projections. The latest twelve month Free Cash Flow stands at about $470.6 million. Analyst and model projections point to Free Cash Flow of $2.53 billion in 2030, with a series of annual estimates and extrapolated figures in between, all expressed in dollar terms and discounted back to today.

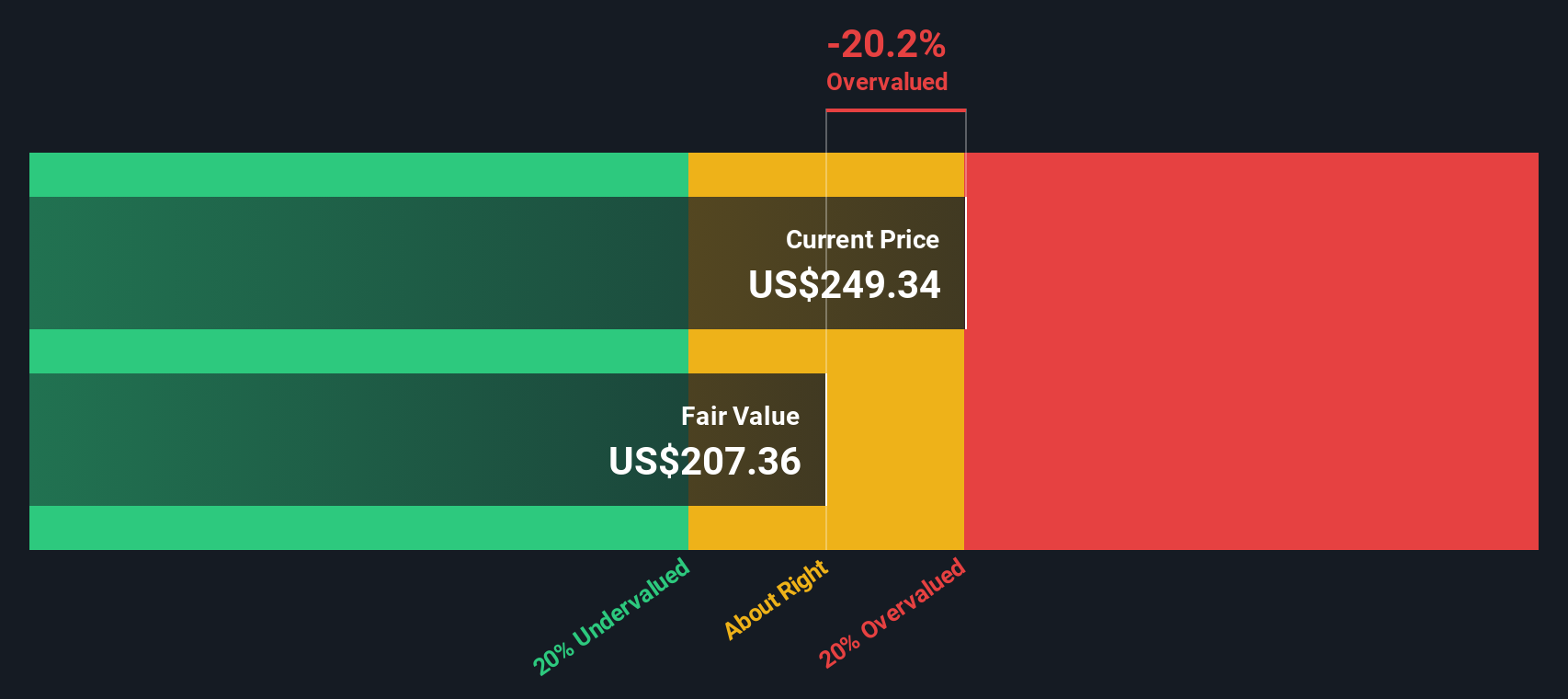

On this basis, the model arrives at an estimated intrinsic value of around $225.81 per share. Compared to the recent share price of $193.24, this implies the stock trades at about a 14.4% discount to this cash flow based estimate, which identifies it as undervalued under this approach.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Take-Two Interactive Software is undervalued by 14.4%. Track this in your watchlist or portfolio, or discover 55 more high quality undervalued stocks.

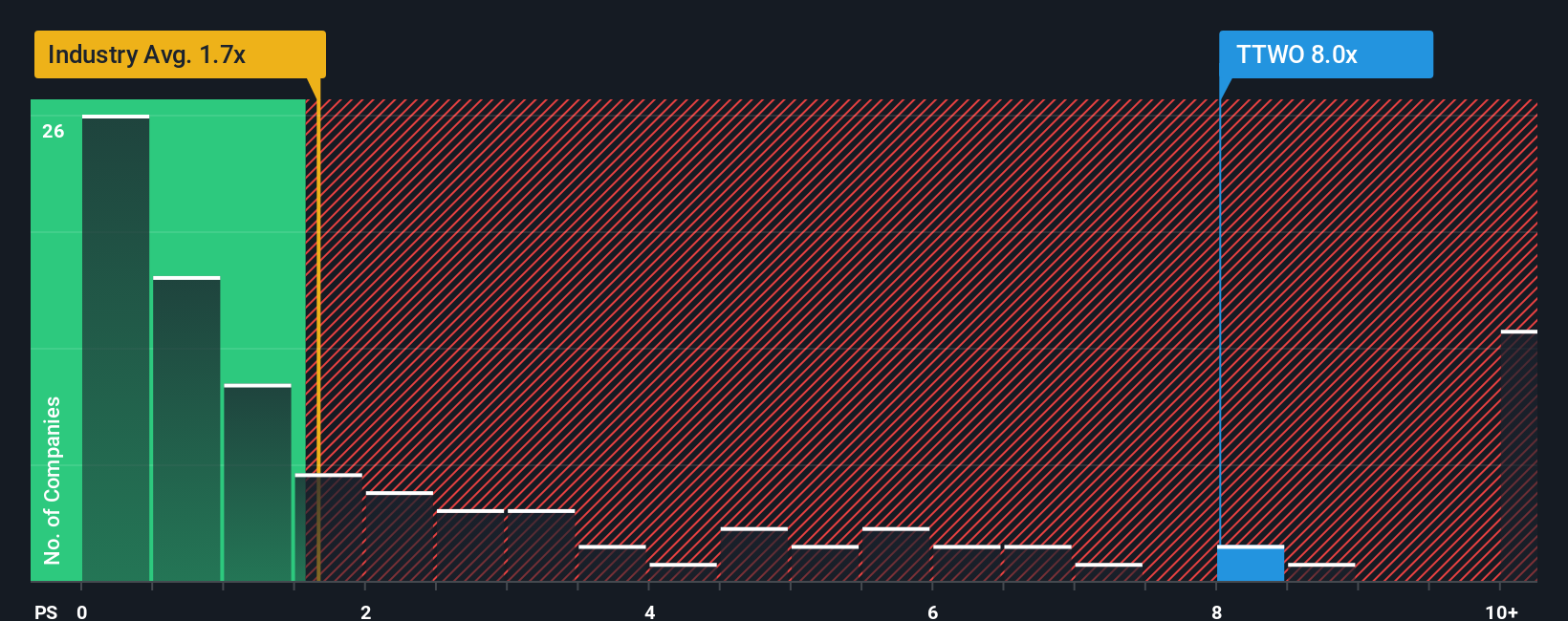

Approach 2: Take-Two Interactive Software Price vs Sales

For a business like Take-Two, where investors often focus on the strength of its franchises and revenue potential, the P/S ratio is a useful cross check because it compares what you pay per share with the sales the company is already generating.

In general, higher growth expectations or lower perceived risk can justify a higher “normal” P/S multiple, while slower growth or higher risk tend to support a lower one. So the context around the number matters as much as the number itself.

Take-Two currently trades on a P/S of 5.46x. That sits well above the Entertainment industry average of 1.32x and the peer group average of 4.52x. Simply Wall St’s Fair Ratio for Take-Two is 3.95x, which is its proprietary estimate of what a reasonable P/S might be given factors such as the company’s earnings profile, industry, profit margins, market cap and risk characteristics.

This Fair Ratio is more tailored than a simple comparison with peers or the broad industry because it adjusts for company specific fundamentals rather than assuming one size fits all. Compared with the actual 5.46x P/S, the 3.95x Fair Ratio suggests Take-Two’s shares are pricing in a higher multiple than those fundamentals would typically support.

Result: OVERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 22 top founder-led companies.

Upgrade Your Decision Making: Choose your Take-Two Interactive Software Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of Take-Two Interactive Software’s future with the numbers behind it. A Narrative is your story about the company, captured as assumptions for future revenue, earnings and margins, which then flow into a financial forecast and an estimated fair value. On Simply Wall St’s Community page, used by millions of investors, you can pick or create a Narrative that fits how you see Take-Two, then compare its Fair Value with today’s share price to help you decide whether the stock looks attractive or expensive to you. Narratives are updated automatically when new information such as earnings or news arrives, so your view can stay aligned with the latest data without extra effort. For example, some investors may use a Narrative that points to a relatively cautious fair value for Take-Two, while others may choose one that supports a materially higher fair value based on a more optimistic outlook.

Do you think there's more to the story for Take-Two Interactive Software? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Take-Two Interactive Software might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TTWO

Take-Two Interactive Software

Develops, publishes, and markets interactive entertainment solutions for consumers worldwide.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3449.4% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7101.3% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.651.0% undervalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£163.7% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

YA

Yaser on iShares Trust - iShares Semiconductor ETF ·

SOXX – iShares Semiconductor ETFFull Analysis Report & EOY 2027 Fair Value Estimate

Fair Value:US$6407.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

YA

Yaser on Schwab Strategic Trust - Schwab U.S. Large-Cap Growth ETF ·

SCHG – Schwab U.S. Large-Cap Growth ETF: Full Analysis & 2026 Fair Value Report

Fair Value:US$3810.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

LY

Lyra on New Horizon Aircraft ·

A Bet on the Last Breath of a Flying Prototype

Fair Value:US$0.24810.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.1% undervalued

66 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.3% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9717.0% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

Trending Discussion

AC

ACV on Alignment Healthcare ·

high medical loss ratios, and negative free cash flow signal that scaling profitably remains elusive...

0

|0