Advertisement

- United States

- /

- Media

- /

- NasdaqGS:PSKY

Has The Skydance Merger Created a Compelling Opportunity in Paramount Skydance Stock?

Simply Wall St

Reviewed by Bailey Pemberton

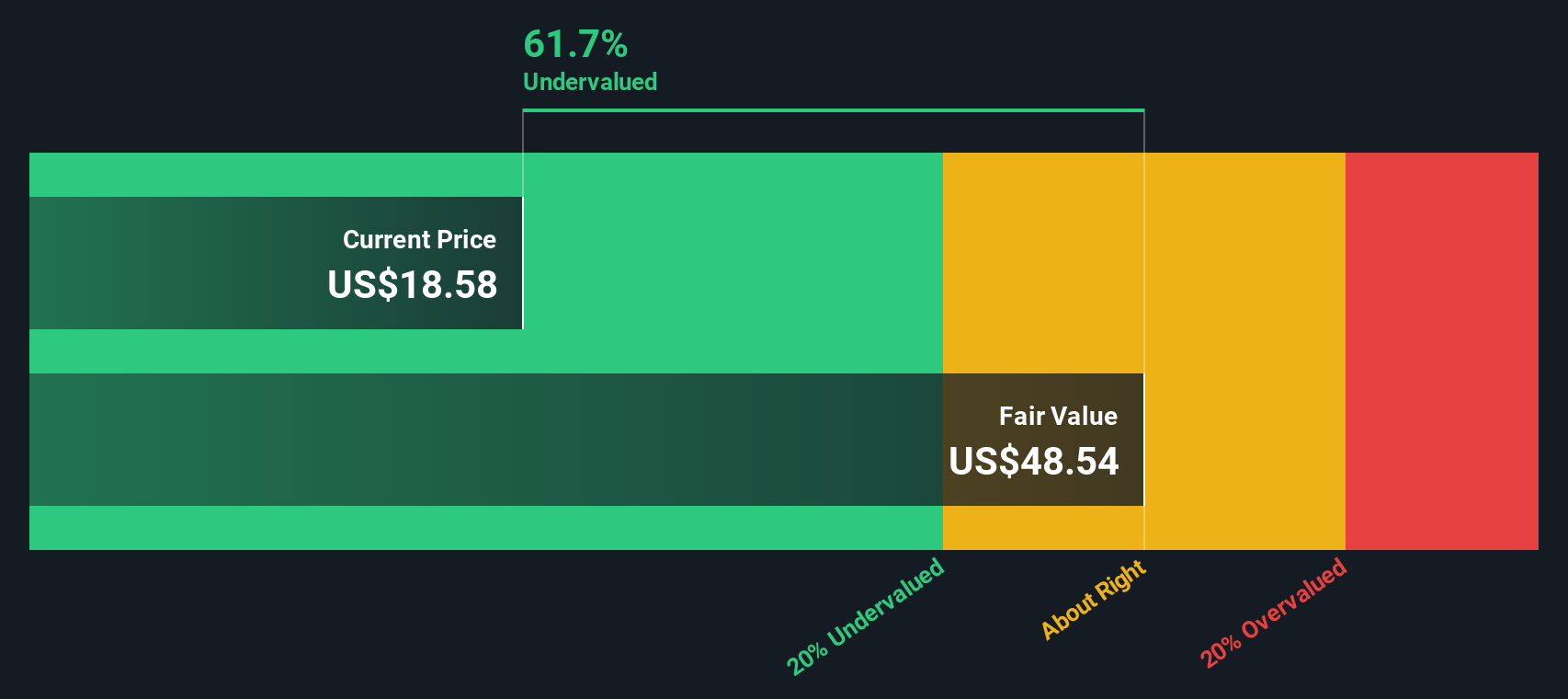

- If you are wondering whether Paramount Skydance is genuinely a bargain or just another media stock story everyone talks about and few understand, you are in the right place to see what the numbers actually say about its value.

- The share price has slipped 7.5% over the last week and is down 1.8% over the past month, yet it is still up 40.1% year to date and 37.0% over the last year. This mix hints at shifting market expectations rather than a simple up or down story.

- Much of the recent price action has been shaped by headlines around the completed Skydance merger, which reshaped the legacy Paramount structure and governance. Investors have also been digesting commentary about how the combined studio and streaming strategy might unlock value from Paramount's content library while trying to manage debt and streaming competition.

- On our framework, Paramount Skydance earns a 5/6 valuation score, suggesting it screens as undervalued on most of the usual checks. However, the real story will come from how we combine different valuation approaches and apply a more nuanced way of thinking about value, which we will explore at the end of the article.

Approach 1: Paramount Skydance Discounted Cash Flow (DCF) Analysis

A DCF model estimates what a business is worth today by projecting the cash it can generate in the future and then discounting those cash flows back to their value in today's dollars.

For Paramount Skydance, the latest twelve month Free Cash Flow is about $305 Million. Analysts and internal estimates project that this will grow meaningfully over time, with Free Cash Flow expected to reach roughly $1.47 Billion by 2035 based on a 2 Stage Free Cash Flow to Equity framework that blends analyst forecasts for the next few years with longer term extrapolations by Simply Wall St.

When these projected cash flows, including a terminal value beyond the explicit forecast horizon, are discounted back, the resulting intrinsic value for the shares is $19.25. Compared with the current market price, this implies the stock is trading at a 23.0% discount. This suggests investors are paying noticeably less than what the cash flow profile would justify.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Paramount Skydance is undervalued by 23.0%. Track this in your watchlist or portfolio, or discover 909 more undervalued stocks based on cash flows.

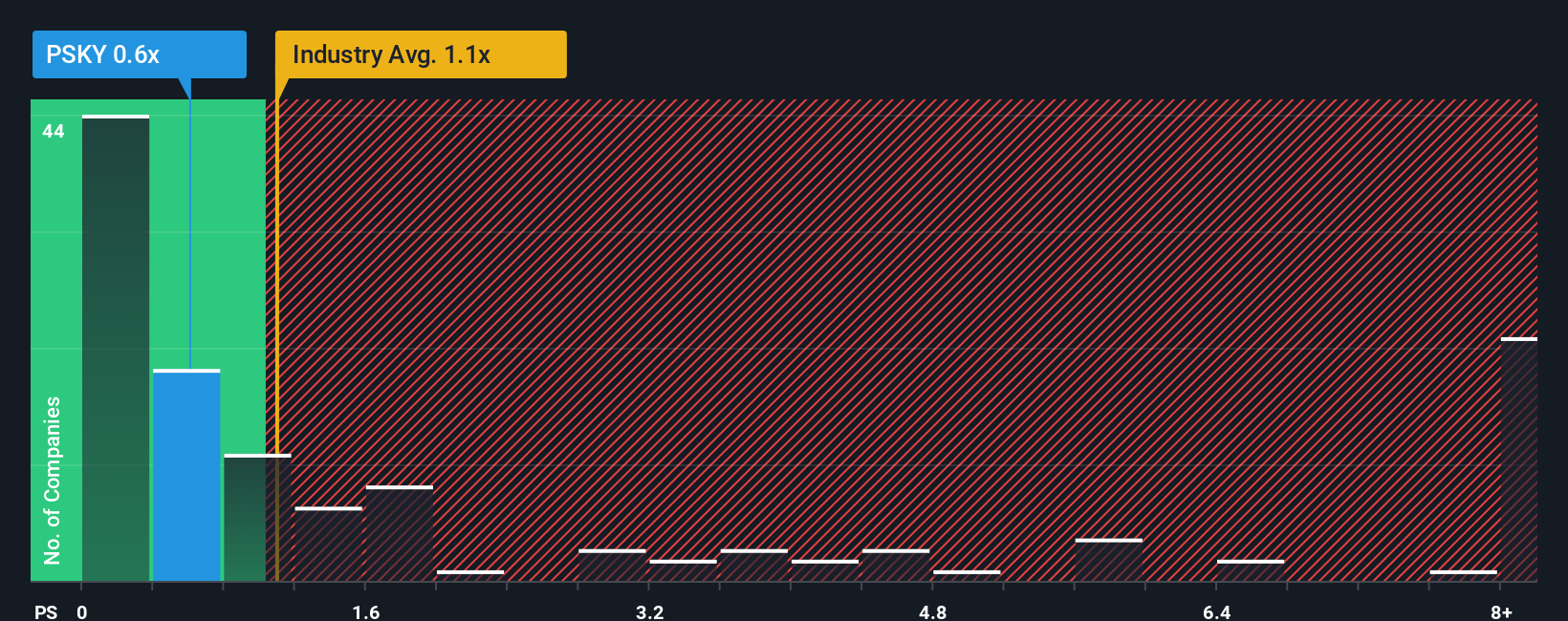

Approach 2: Paramount Skydance Price vs Sales

For media and streaming businesses that are still normalising profitability, the Price to Sales ratio is often a more reliable yardstick than earnings based measures, because revenue tends to be more stable than short term profits affected by restructuring, content write downs or integration costs.

What investors are really doing with any valuation multiple is weighing expected growth against risk, so a higher growth, lower risk business should normally justify a higher Price to Sales ratio than a slower, more cyclical one. Paramount Skydance currently trades on a Price to Sales ratio of about 0.57x, well below both the Media industry average of around 1.08x and its peer group average of roughly 1.08x. On the surface this makes the stock look inexpensive.

Simply Wall St's Fair Ratio framework goes a step further by estimating what Price to Sales multiple a company should trade on, given its growth outlook, profitability profile, industry, market cap and risk factors. This produces a Fair Ratio of 1.50x for Paramount Skydance, which is meaningfully above the current 0.57x. On this lens, the shares screen as attractively priced relative to what a balanced view of fundamentals would imply.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Paramount Skydance Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of a company’s story with the numbers behind its value. A Narrative is your own structured storyline for a stock, where you set assumptions for future revenue, earnings and margins, and those assumptions flow into a forecast and then into an explicit fair value estimate. Narratives on Simply Wall St, available to millions of investors on the Community page, make this process accessible by guiding you from business thesis to financial model without needing a spreadsheet. Once you have a Narrative, you can easily compare its Fair Value to the current share price to decide whether Paramount Skydance looks like a buy, hold or sell under your assumptions. Narratives also stay alive, automatically updating when new information such as earnings results, guidance or major news is released, so your view does not go stale. For Paramount Skydance, one investor’s Narrative might assume a very optimistic fair value with rapid streaming growth, while another’s might build a more cautious fair value driven by slower revenue growth and margin pressure.

Do you think there's more to the story for Paramount Skydance? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PSKY

Paramount Skydance

Operates as a media and entertainment company worldwide.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4729.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6410.8% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.8% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.71.9% undervalued

1342 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative