Advertisement

- United States

- /

- Interactive Media and Services

- /

- NasdaqGS:MTCH

Does Darrell Cavens Joining the Board Signal a New Strategic Era for Match Group (MTCH)?

Simply Wall St

Reviewed by Sasha Jovanovic

- Match Group recently announced that e-commerce leader Darrell Cavens will join its Board of Directors and that the company will seek shareholder approval to declassify its board in connection with its 2025 annual meeting.

- This move brings significant digital commerce and governance expertise to Match Group, while signaling commitment to board refreshment and enhanced corporate governance practices.

- We'll look at how adding Darrell Cavens, a digital commerce veteran, could reshape Match Group's investment narrative and strategic direction.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Match Group Investment Narrative Recap

To be a shareholder in Match Group, an investor must believe in the company’s ability to offset user declines and competitive threats through ongoing product innovation, brand diversification, and digital commerce expertise. The recent addition of Darrell Cavens to the board brings valuable technology and online retailing experience, but this alone is not likely to meaningfully shift the most important near-term catalyst, user growth turnaround at Tinder and Hinge, or alleviate the most pressing risk around sustained declines in user metrics.

Among recent company developments, Match Group’s introduction of Tinder’s Face Check verification stands out as closely aligned with product-led catalysts by strengthening user trust and safety, two areas critical for engagement and payer growth. While this initiative and Cavens’ background both focus on technology-driven improvement, investors should closely monitor whether these changes can drive the necessary momentum to reverse user trends.

By contrast, ongoing user declines and competitive pressures remain a material risk that investors should be aware of, especially if...

Read the full narrative on Match Group (it's free!)

Match Group's outlook suggests revenue of $4.0 billion and earnings of $811.8 million by 2028. This is based on an assumed annual revenue growth rate of 5.0% and reflects a $274 million increase in earnings from the current $537.8 million.

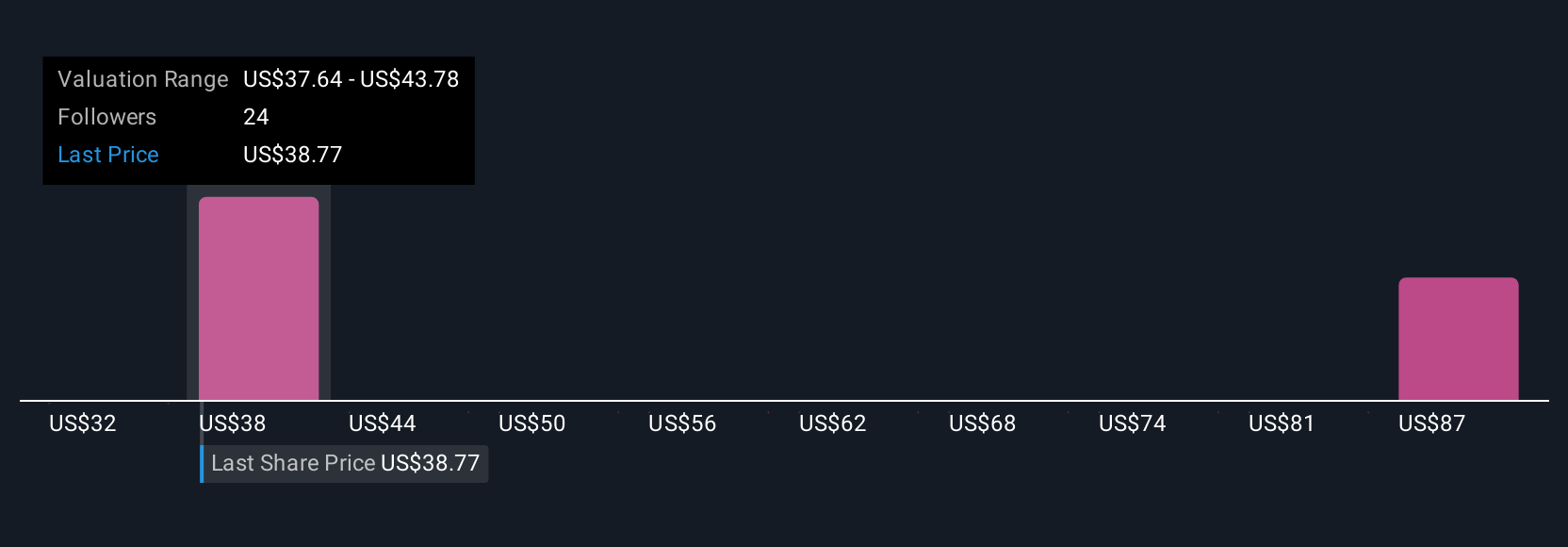

Uncover how Match Group's forecasts yield a $37.32 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Fair value estimates from the Simply Wall St Community range from US$31.51 to US$80.87 across 5 member analyses. Many see opportunity tied to successful product innovation, while others flag persistent user and competition risks, offering readers several sharply different perspectives to consider.

Explore 5 other fair value estimates on Match Group - why the stock might be worth over 2x more than the current price!

Build Your Own Match Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Match Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Match Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Match Group's overall financial health at a glance.

Curious About Other Options?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:MTCH

Undervalued second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

935 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative