Advertisement

- United States

- /

- Interactive Media and Services

- /

- NasdaqGS:META

Why You Should Care About Meta Platforms' (NASDAQ:META) Strong Returns On Capital

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. With that in mind, the ROCE of Meta Platforms (NASDAQ:META) looks attractive right now, so lets see what the trend of returns can tell us.

Understanding Return On Capital Employed (ROCE)

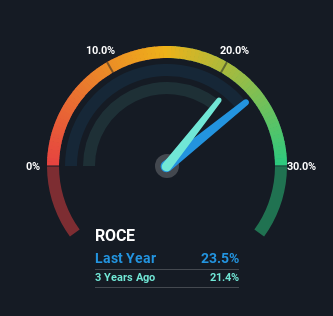

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Meta Platforms is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.24 = US$44b ÷ (US$216b - US$31b) (Based on the trailing twelve months to September 2023).

So, Meta Platforms has an ROCE of 24%. In absolute terms that's a great return and it's even better than the Interactive Media and Services industry average of 9.0%.

Check out our latest analysis for Meta Platforms

In the above chart we have measured Meta Platforms' prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Meta Platforms here for free.

What Can We Tell From Meta Platforms' ROCE Trend?

In terms of Meta Platforms' history of ROCE, it's quite impressive. The company has employed 114% more capital in the last five years, and the returns on that capital have remained stable at 24%. Now considering ROCE is an attractive 24%, this combination is actually pretty appealing because it means the business can consistently put money to work and generate these high returns. If Meta Platforms can keep this up, we'd be very optimistic about its future.

In Conclusion...

In the end, the company has proven it can reinvest it's capital at high rates of returns, which you'll remember is a trait of a multi-bagger. And the stock has done incredibly well with a 165% return over the last five years, so long term investors are no doubt ecstatic with that result. So even though the stock might be more "expensive" than it was before, we think the strong fundamentals warrant this stock for further research.

One more thing, we've spotted 1 warning sign facing Meta Platforms that you might find interesting.

If you'd like to see other companies earning high returns, check out our free list of companies earning high returns with solid balance sheets here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:META

Meta Platforms

Engages in the development of products that enable people to connect and share with friends and family through mobile devices, personal computers, virtual reality and mixed reality headsets, augmented reality, and wearables worldwide.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|31.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|44.7% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|40.9% undervalued

AG

Community Contributor