Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Cardlytics, Inc. (NASDAQ:CDLX) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Cardlytics

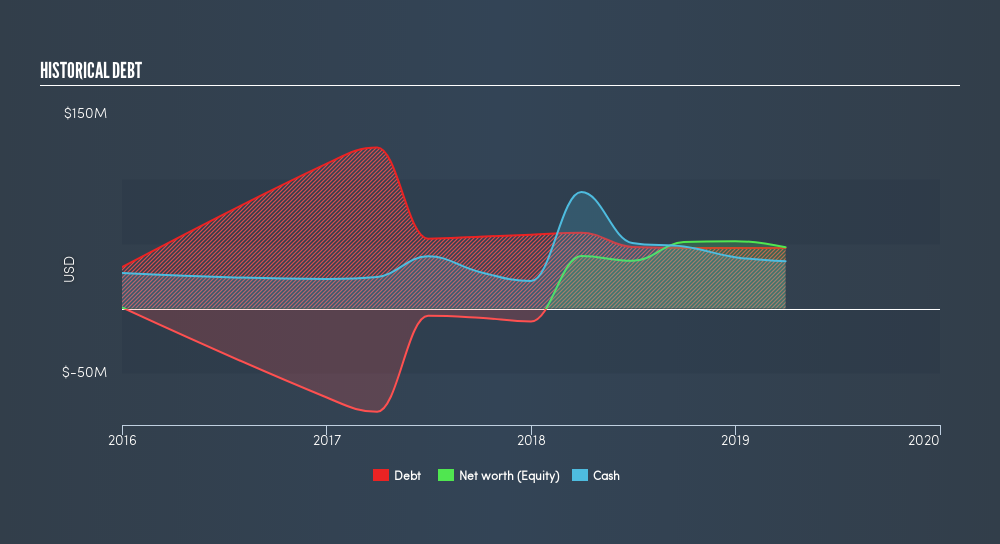

What Is Cardlytics's Debt?

The image below, which you can click on for greater detail, shows that Cardlytics had debt of US$46.7m at the end of March 2019, a reduction from US$58.6m over a year. However, because it has a cash reserve of US$36.4m, its net debt is less, at about US$10.3m.

How Healthy Is Cardlytics's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Cardlytics had liabilities of US$49.6m due within 12 months and liabilities of US$49.7m due beyond that. Offsetting these obligations, it had cash of US$36.4m as well as receivables valued at US$55.6m due within 12 months. So it has liabilities totalling US$7.29m more than its cash and near-term receivables, combined.

Having regard to Cardlytics's size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the US$672.3m company is struggling for cash, we still think it's worth monitoring its balance sheet. Either way, since Cardlytics does have more debt than cash, it's worth keeping an eye on its balance sheet. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Cardlytics's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Cardlytics managed to grow its revenue by 13%, to US$154m. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

Caveat Emptor

Importantly, Cardlytics had negative earnings before interest and tax (EBIT), over the last year. To be specific the EBIT loss came in at US$38m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. Another cause for caution is that is bled US$29m in negative free cash flow over the last twelve months. So to be blunt we think it is risky. When I consider a company to be a bit risky, I think it is responsible to check out whether insiders have been reporting any share sales. Luckily, you can click here ito see our graphic depicting Cardlytics insider transactions.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NasdaqGM:CDLX

Cardlytics

Operates an advertising platform in the United States and the United Kingdom.

Very undervalued with slight risk.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion