Advertisement

- United States

- /

- Chemicals

- /

- NYSEAM:CMT

Core Molding Technologies (NYSEMKT:CMT) Strong Profits May Be Masking Some Underlying Issues

Core Molding Technologies, Inc.'s (NYSEMKT:CMT) robust recent earnings didn't do much to move the stock. We think this is due to investors looking beyond the statutory profits and being concerned with what they see.

Check out our latest analysis for Core Molding Technologies

Examining Cashflow Against Core Molding Technologies' Earnings

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

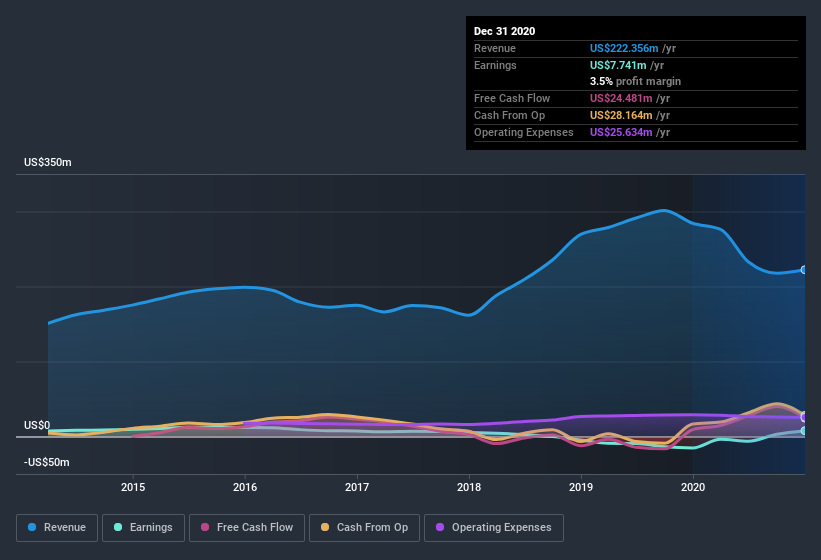

Over the twelve months to December 2020, Core Molding Technologies recorded an accrual ratio of -0.13. That indicates that its free cash flow was a fair bit more than its statutory profit. To wit, it produced free cash flow of US$24m during the period, dwarfing its reported profit of US$7.74m. Core Molding Technologies shareholders are no doubt pleased that free cash flow improved over the last twelve months. Having said that it seems that a recent tax benefit and some unusual items have impacted its profit (and this its accrual ratio).

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Core Molding Technologies.

The Impact Of Unusual Items On Profit

While the accrual ratio might bode well, we also note that Core Molding Technologies' profit was boosted by unusual items worth US$833k in the last twelve months. We can't deny that higher profits generally leave us optimistic, but we'd prefer it if the profit were to be sustainable. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And, after all, that's exactly what the accounting terminology implies. If Core Molding Technologies doesn't see that contribution repeat, then all else being equal we'd expect its profit to drop over the current year.

An Unusual Tax Situation

Moving on from the accrual ratio, we note that Core Molding Technologies profited from a tax benefit which contributed US$3.6m to profit. This is meaningful because companies usually pay tax rather than receive tax benefits. We're sure the company was pleased with its tax benefit. And given that it lost money last year, it seems possible that the benefit is evidence that it now expects to find value in its past tax losses. However, the devil in the detail is that these kind of benefits only impact in the year they are booked, and are often one-off in nature. In the likely event the tax benefit is not repeated, we'd expect to see its statutory profit levels drop, at least in the absence of strong growth.

Our Take On Core Molding Technologies' Profit Performance

Summing up, Core Molding Technologies' accrual ratio suggests that its statutory earnings are well matched by free cash flow while its unusual items and tax benefit is boosted profit in a way that may not be sustained. After taking into account all the aforementioned observations we think that Core Molding Technologies' profits probably give a generous impression of its sustainable level of profitability. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. For example, Core Molding Technologies has 3 warning signs (and 1 which is a bit unpleasant) we think you should know about.

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you’re looking to trade Core Molding Technologies, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NYSEAM:CMT

Core Molding Technologies

Operates as a molder of thermoplastic and thermoset structural products.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|62.4% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|19.2% undervalued

ZW

Community Contributor