Advertisement

- United States

- /

- Chemicals

- /

- NYSE:WLK

Could Westlake’s (WLK) Debt Refinancing Signal a Shift in Its Long-Term Financial Strategy?

Simply Wall St

Reviewed by Sasha Jovanovic

- In early November 2025, Westlake Corporation completed two major fixed-income offerings totaling nearly US$1.2 billion and concluded a tender offer for its 3.600% Senior Notes due 2026, repurchasing US$253.7 million of the outstanding US$750 million notes.

- This debt refinancing initiative reflects a drive to extend the company’s debt maturities and optimize its capital structure by using proceeds from new long-term notes to reduce near-term obligations.

- We’ll explore how Westlake’s sizable repurchase of 2026 notes with proceeds from new longer-dated debt could influence its future potential.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Westlake Investment Narrative Recap

To be a shareholder in Westlake right now, you have to believe that its underlying strengths in infrastructure and residential construction can overcome persistent losses and sector headwinds. The recent refinancing, raising nearly US$1.2 billion in new long-term debt and retiring a portion of the 2026 notes, does not materially alter the biggest short-term catalyst: stabilization in U.S. construction demand. However, it also does not resolve the most pressing risk, which remains ongoing margin compression in the Performance and Essential Materials segment due to global oversupply.

Among the recent announcements, the Q3 2025 earnings release stands out, reflecting a net loss of US$782 million and a substantial goodwill impairment. This loss underscores how cost pressures and weak end-market demand are having a significant impact, reaffirming the urgency for the catalysts, like municipal infrastructure spending, to deliver results and offset these operational challenges.

By contrast, investors should be aware that Westlake's exposure to sustained industry overcapacity and the resulting pricing pressure could...

Read the full narrative on Westlake (it's free!)

Westlake's narrative projects $13.0 billion revenue and $893.8 million earnings by 2028. This requires 3.5% yearly revenue growth and a $960.8 million increase in earnings from $-67.0 million today.

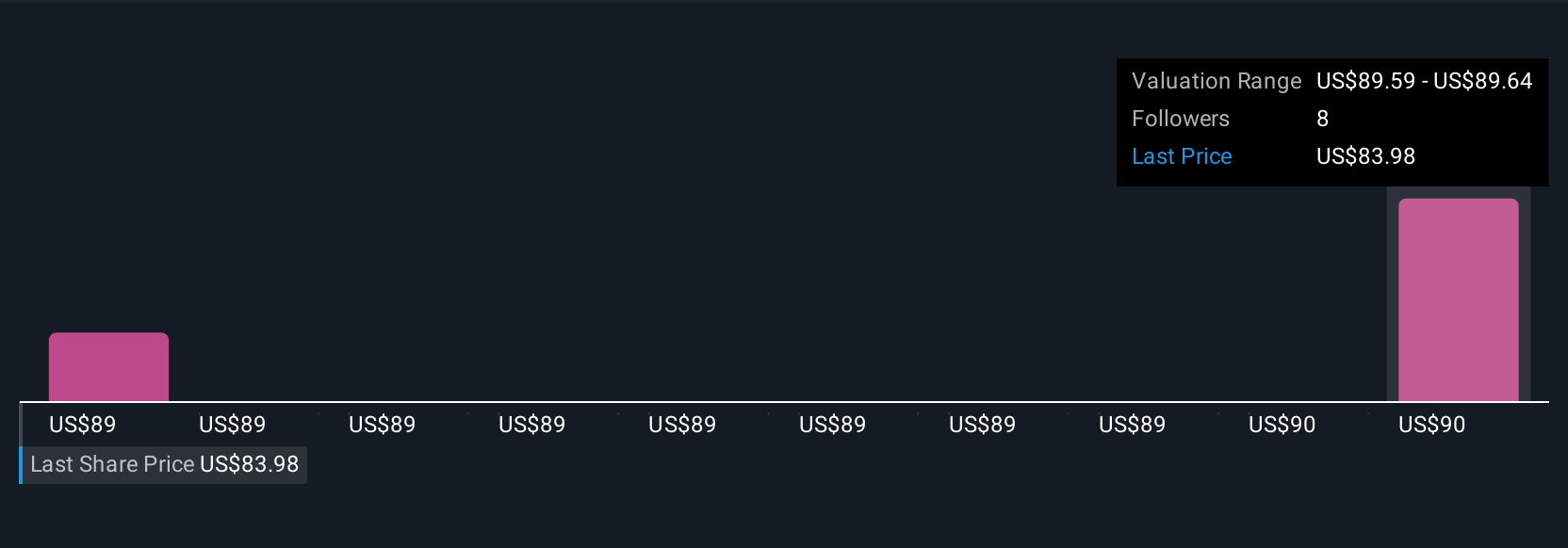

Uncover how Westlake's forecasts yield a $82.21 fair value, a 27% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members’ fair value estimates for Westlake range from US$62.32 to US$82.21, based on two independent viewpoints. With margin pressure from persistent oversupply still a key risk, you will find a wide variety of opinions and perspectives worth exploring here.

Explore 2 other fair value estimates on Westlake - why the stock might be worth just $62.32!

Build Your Own Westlake Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Westlake research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Westlake research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Westlake's overall financial health at a glance.

Ready For A Different Approach?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 37 companies in the world exploring or producing it. Find the list for free.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Westlake might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WLK

Westlake

Manufactures and markets performance and essential materials, and housing and infrastructure products in the United States, Canada, Germany, China, Mexico, Brazil, France, Italy, and internationally.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor