- United States

- /

- Packaging

- /

- NYSE:SEE

Should You Investigate Sealed Air Corporation (NYSE:SEE) At US$35.69?

Sealed Air Corporation (NYSE:SEE), is not the largest company out there, but it saw a decent share price growth of 13% on the NYSE over the last few months. Shareholders may appreciate the recent price jump, but the company still has a way to go before reaching its yearly highs again. With many analysts covering the mid-cap stock, we may expect any price-sensitive announcements have already been factored into the stock’s share price. However, could the stock still be trading at a relatively cheap price? Today we will analyse the most recent data on Sealed Air’s outlook and valuation to see if the opportunity still exists.

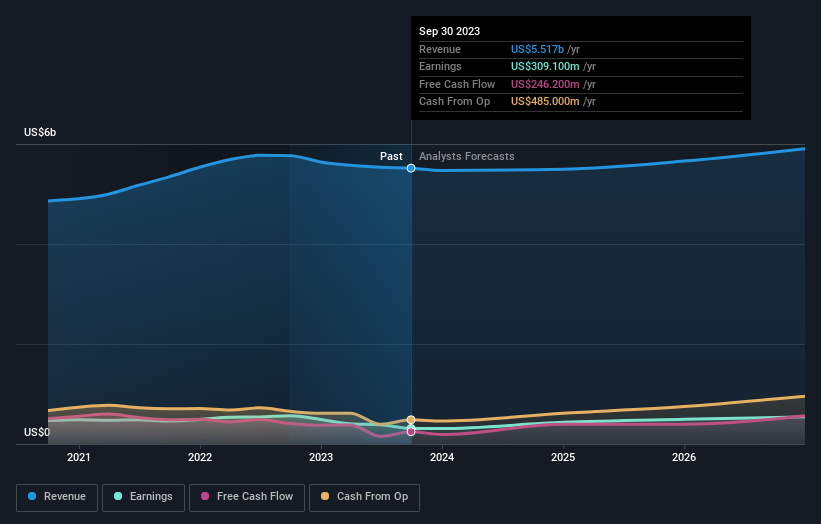

Check out our latest analysis for Sealed Air

Is Sealed Air Still Cheap?

The share price seems sensible at the moment according to our price multiple model, where we compare the company's price-to-earnings ratio to the industry average. We’ve used the price-to-earnings ratio in this instance because there’s not enough visibility to forecast its cash flows. The stock’s ratio of 16.68x is currently trading slightly below its industry peers’ ratio of 17.19x, which means if you buy Sealed Air today, you’d be paying a decent price for it. And if you believe Sealed Air should be trading in this range, then there isn’t much room for the share price to grow beyond the levels of other industry peers over the long-term. Is there another opportunity to buy low in the future? Since Sealed Air’s share price is quite volatile, we could potentially see it sink lower (or rise higher) in the future, giving us another chance to buy. This is based on its high beta, which is a good indicator for how much the stock moves relative to the rest of the market.

What does the future of Sealed Air look like?

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Buying a great company with a robust outlook at a cheap price is always a good investment, so let’s also take a look at the company's future expectations. With profit expected to grow by 72% over the next couple of years, the future seems bright for Sealed Air. It looks like higher cash flow is on the cards for the stock, which should feed into a higher share valuation.

What This Means For You

Are you a shareholder? SEE’s optimistic future growth appears to have been factored into the current share price, with shares trading around industry price multiples. However, there are also other important factors which we haven’t considered today, such as the track record of its management team. Have these factors changed since the last time you looked at SEE? Will you have enough confidence to invest in the company should the price drop below the industry PE ratio?

Are you a potential investor? If you’ve been keeping tabs on SEE, now may not be the most advantageous time to buy, given it is trading around industry price multiples. However, the optimistic forecast is encouraging for SEE, which means it’s worth diving deeper into other factors such as the strength of its balance sheet, in order to take advantage of the next price drop.

If you want to dive deeper into Sealed Air, you'd also look into what risks it is currently facing. When we did our research, we found 2 warning signs for Sealed Air (1 is a bit concerning!) that we believe deserve your full attention.

If you are no longer interested in Sealed Air, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

If you're looking to trade Sealed Air, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:SEE

Sealed Air

Provides packaging solutions in the United States and internationally, Europe, the Middle East, Africa, and Asia Pacific.

Undervalued established dividend payer.

Similar Companies

Market Insights

Community Narratives