Advertisement

- United States

- /

- Metals and Mining

- /

- NYSE:SCCO

Is Southern Copper’s 51.6% Rally Supported by Strong Demand and Expansion News?

Simply Wall St

Reviewed by Bailey Pemberton

- Ever wondered if Southern Copper is worth the price tag? You are not alone. Many investors are asking whether it is undervalued, overvalued, or somewhere in between.

- The stock has shown big moves lately, jumping 9.0% in the past week and boasting a solid 51.6% gain year-to-date, though it slipped by 3.0% over the last month.

- Analysts and investors have taken notice as copper prices continue climbing, with the company standing out in recent headlines for strategic investments and expanding capacity to meet rising demand. Coverage in financial media has highlighted both global supply fears and strong industry tailwinds, adding fresh context to Southern Copper’s share price action.

- But here is the key number: Southern Copper’s valuation score is 0 out of 6, indicating it does not appear undervalued on any major metric. Next, we will break down what this means using the main valuation approaches. Stick around for a deeper perspective at the end of the article that could change how you think about value altogether.

Southern Copper scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Southern Copper Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates the intrinsic value of a company by projecting its expected future cash flows and discounting them back to their present value. For Southern Copper, this method looks at both analyst estimates and extrapolated data to forecast the company's Free Cash Flow (FCF) over the coming years.

Currently, Southern Copper’s Free Cash Flow stands at approximately $3.44 billion. Based on analyst projections and extrapolations, this figure is expected to rise each year, reaching an estimated $7.14 billion by 2035. Analysts have provided forecasts for the next five years, while figures beyond that point are rounded out using calculated estimates.

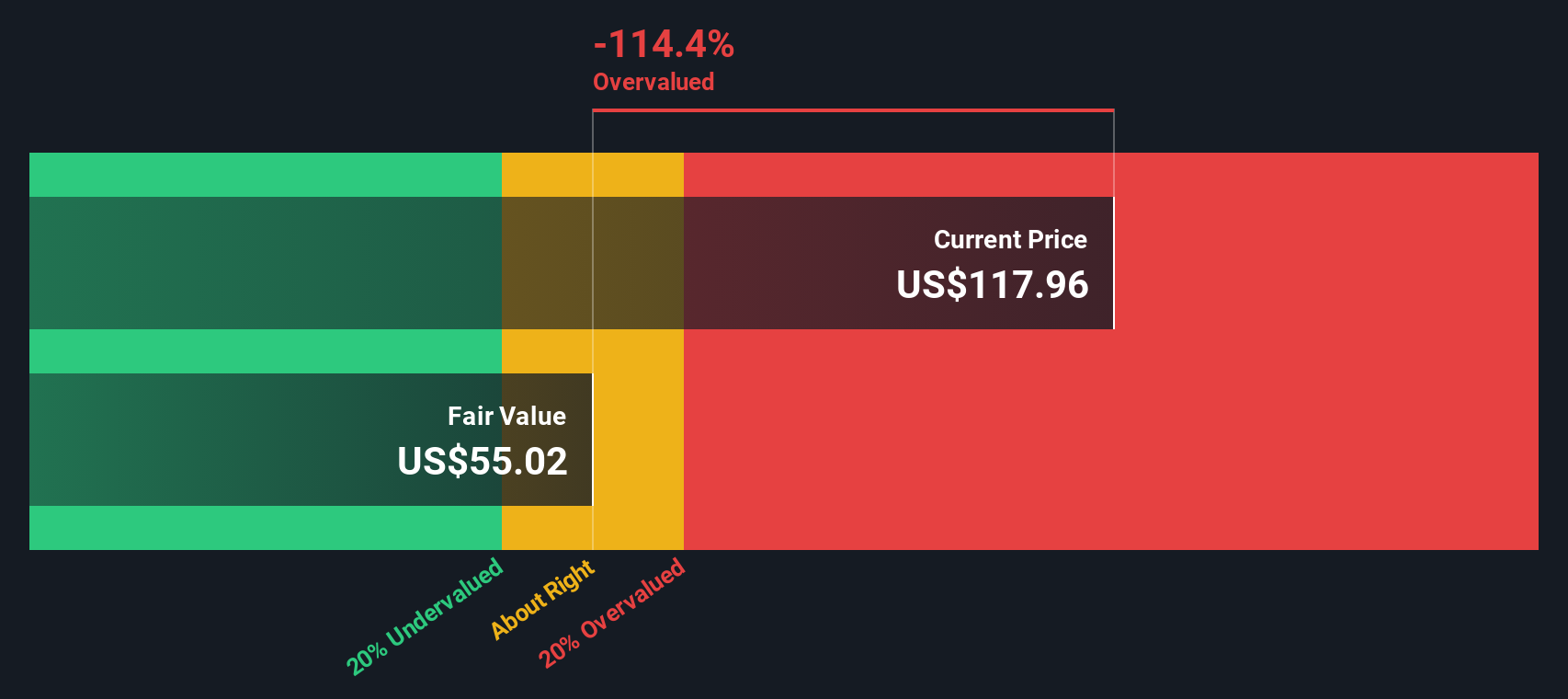

Using all these projections, the DCF model calculates an intrinsic fair value for Southern Copper’s stock of about $125.91 per share. Comparing this value to the current stock price shows the shares are trading at a 7.0% premium. In other words, the stock is not undervalued according to this cash flow-based valuation, but it is also not significantly overvalued.

Result: ABOUT RIGHT

Southern Copper is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

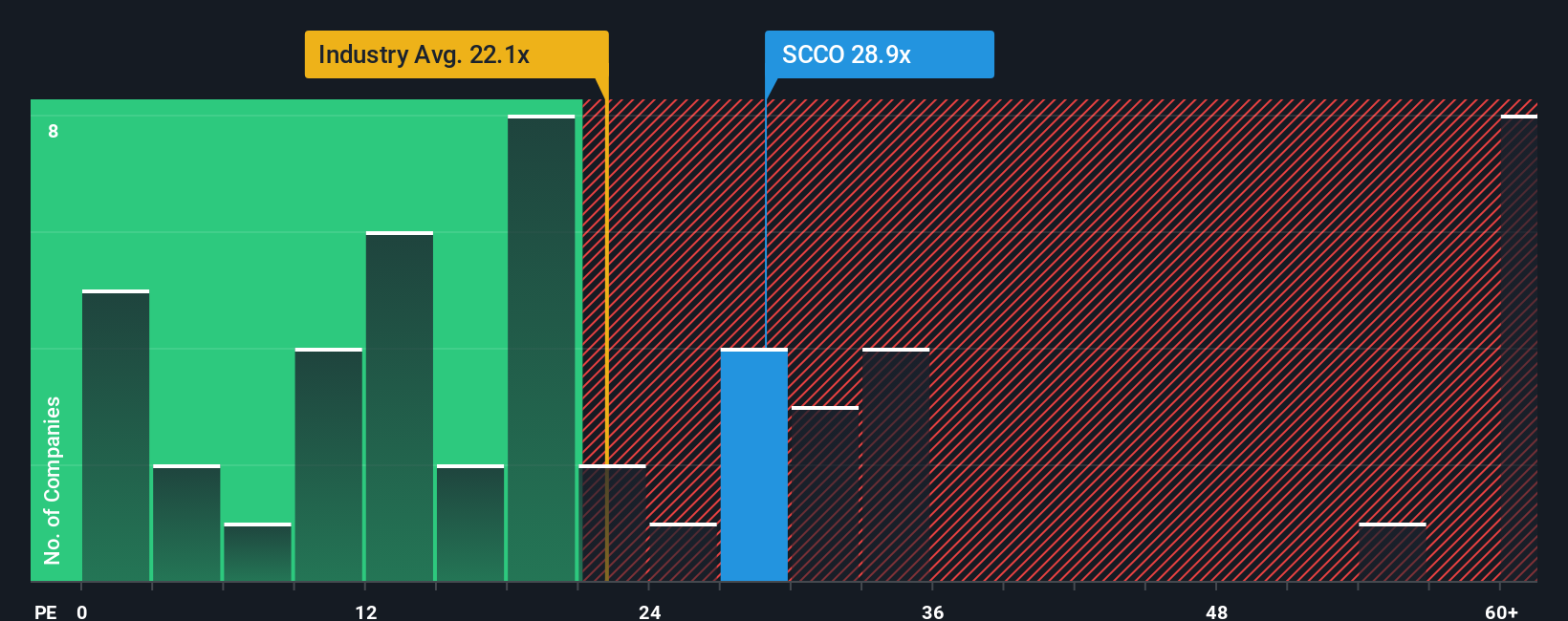

Approach 2: Southern Copper Price vs Earnings (P/E Ratio)

For companies like Southern Copper that are consistently profitable, the Price-to-Earnings (P/E) ratio is a widely used metric to judge valuation. This ratio reflects how much investors are willing to pay per dollar of earnings, making it especially relevant for firms with steady profits.

The level of P/E that is considered “normal” often depends on how fast a company is expected to grow and how risky its operations are. Faster-growing companies typically enjoy higher P/E ratios, while those considered riskier usually see a discount compared to safer peers.

Currently, Southern Copper is trading at a P/E of 28.9x. For context, the average P/E across the Metals and Mining industry is 22.2x, and its major peers average about 25.5x. On both measures, Southern Copper appears more expensive than the industry and its peer group.

This is where Simply Wall St’s proprietary “Fair Ratio” comes in. The Fair Ratio for Southern Copper is 23.7x, which is calculated using factors beyond simple peer comparison, such as the company’s earnings growth potential, industry characteristics, profit margins, market cap, and specific business risks. This tailored approach aims to give a more accurate benchmark for what Southern Copper’s P/E should be in today’s market, rather than relying solely on raw industry averages.

With the stock trading at 28.9x but a Fair Ratio of 23.7x, Southern Copper’s shares are moderately overvalued based on this approach.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1438 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Southern Copper Narrative

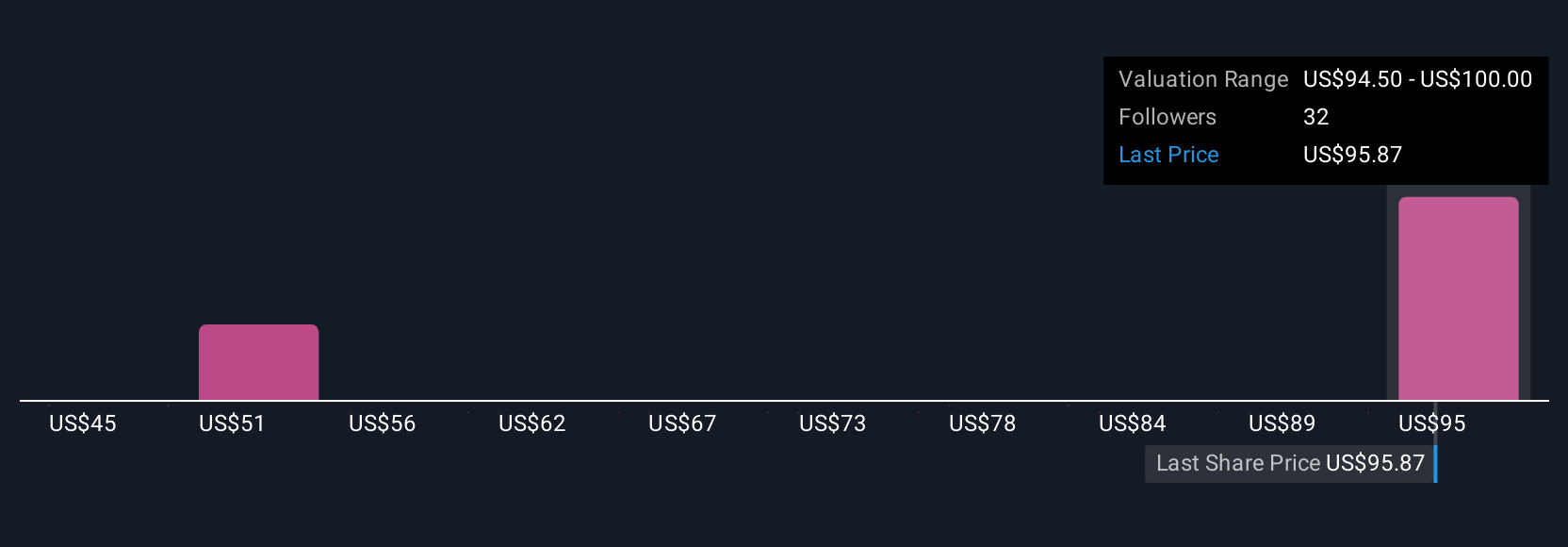

Earlier we mentioned there is an even better way to understand valuation. Let’s introduce you to Narratives. A Narrative is your personalized view of a company, a story built around your expectations for its future, including forecasts for revenue, earnings, and margins. This leads to what you think is a fair value. Narratives connect the dots between the company’s business outlook and a financial forecast, turning a collection of numbers into a focused investment thesis that is easy to reference and refine.

On Simply Wall St’s Community page, used by millions of other investors, you can create, share, and update Narratives to quickly compare how your fair value stacks up against the current share price. Narratives are dynamically updated when new news or earnings data arrives, so you are always making decisions based on the latest information. For example, analysts with a bullish Narrative on Southern Copper might expect project expansions and strong copper prices to drive the stock as high as $128.70 per share, while bearish analysts worry about project delays and geopolitical risks, seeing fair value closer to $66.63. Narratives empower you to invest with confidence, grounded in both numbers and real company stories.

Do you think there's more to the story for Southern Copper? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:SCCO

Southern Copper

Engages in mining, exploring, smelting, and refining copper and other minerals in Peru, Mexico, Argentina, Ecuador, and Chile.

Outstanding track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

933 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative