- United States

- /

- Metals and Mining

- /

- NYSE:MP

Is MP Materials Stock Getting Ahead of Itself After the 2025 Rare Earths Rally?

Reviewed by Bailey Pemberton

- Investors wondering if MP Materials is still a smart consideration after its big run up, or if the market has already priced in the story, can use this breakdown to assess whether the current share price makes sense.

- Despite a sharp pullback of 8.2% over the last week and 18.1% over the last month, the stock is still up an eye catching 217.5% year to date and 228.5% over the past year. This suggests that sentiment has shifted dramatically.

- Recent moves have been fueled by heightened attention on rare earth supply chains and US onshoring efforts, with MP Materials often cited as a strategic domestic player in policy and industry discussions. In addition, media coverage around clean energy, electric vehicles and critical minerals has kept the company in the spotlight, amplifying both enthusiasm and volatility.

- Yet on our framework MP Materials only scores 1 out of 6 on undervaluation checks. In the next sections we will walk through traditional valuation approaches and then finish with a more holistic way of thinking about what the stock is truly worth.

MP Materials scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: MP Materials Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth today by projecting the cash it could generate in the future and discounting those cash flows back into today’s dollars.

For MP Materials, the latest twelve months Free Cash Flow is roughly -$294.5 Million, reflecting heavy investment and a business that is not yet consistently generating cash. Analysts expect cash flows to turn positive over the next few years, with projections stepping up to around -$27.8 Million in 2026, then rising to $22.7 Million in 2027 and accelerating further. Beyond the first five years, Simply Wall St extrapolates this trajectory, with Free Cash Flow estimates climbing to about $243.5 Million by 2035.

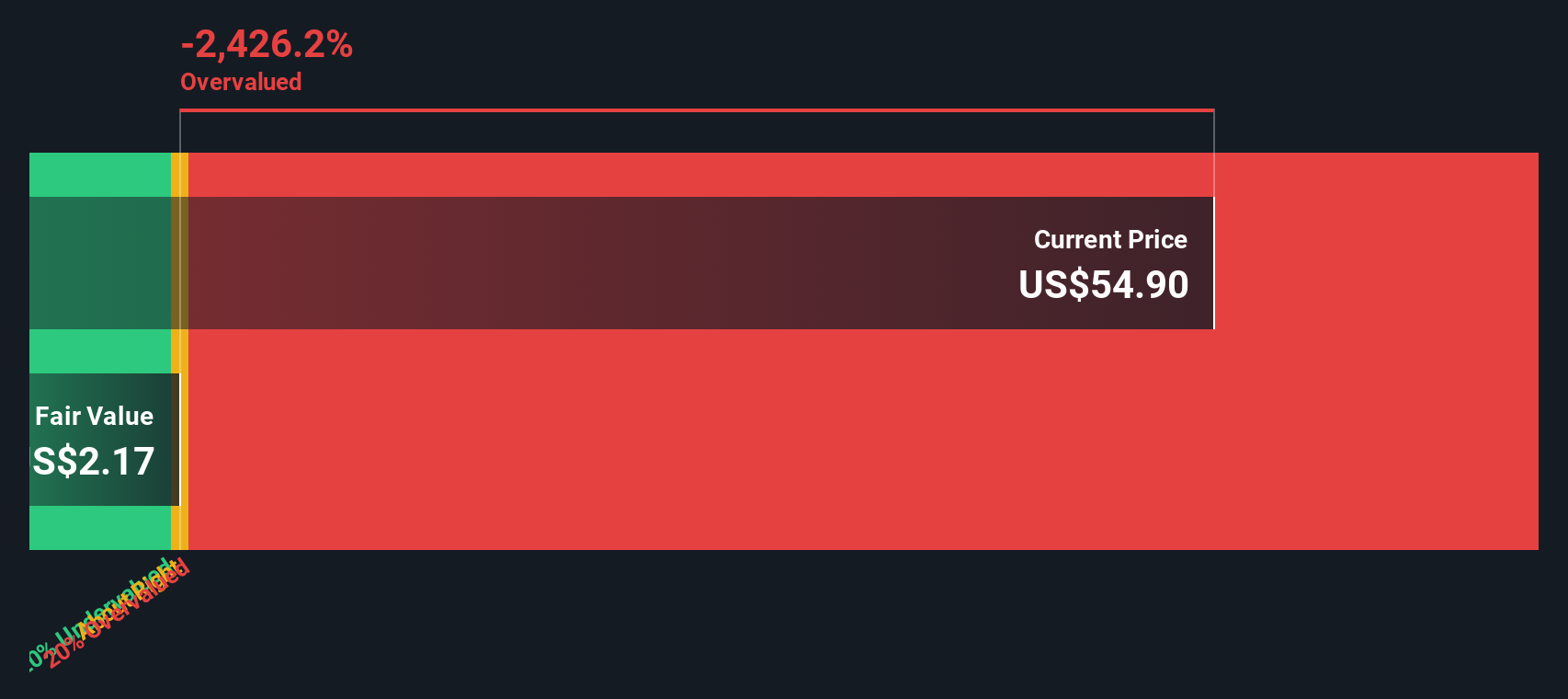

When all these future cash flows are discounted back using a 2 Stage Free Cash Flow to Equity model, the intrinsic value comes out at roughly $16.09 per share. Compared with the current share price, this implies the stock is about 223.4% overvalued on a DCF basis, suggesting that a lot of future success is already priced in.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests MP Materials may be overvalued by 223.4%. Discover 918 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: MP Materials Price vs Sales

For companies where profits are still developing or volatile, the Price to Sales ratio is often a more reliable yardstick than earnings based metrics, because sales are typically more stable and less affected by accounting choices.

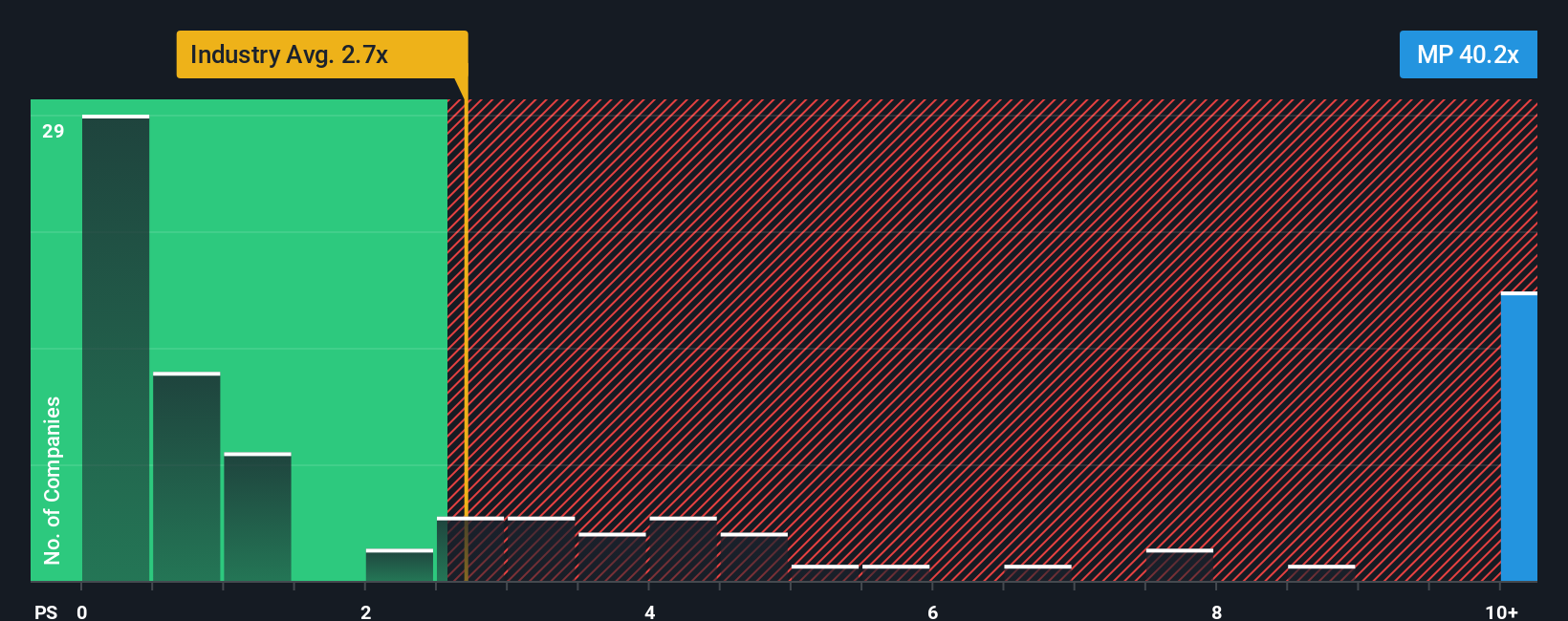

In general, faster growth and lower risk can justify a higher Price to Sales multiple, while slower growth and higher uncertainty should translate into a lower, more conservative multiple. With MP Materials currently trading on a rich 39.63x Price to Sales ratio, the stock sits far above the Metals and Mining industry average of about 2.26x and even further above its peer group average of around 0.78x.

Simply Wall St’s Fair Ratio framework refines this comparison by estimating what multiple the market should reasonably pay for MP, given its growth outlook, profitability profile, industry positioning, market cap and specific risks. On this basis, MP’s Fair Ratio is just 2.58x. This is a far more nuanced benchmark than simple peer or industry comparisons because it adjusts for the company’s own fundamentals. Set against the actual 39.63x Price to Sales multiple, this suggests investors are paying well above what the underlying profile would justify.

Result: OVERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1460 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your MP Materials Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simply the stories investors tell about a company in numbers, by connecting their view of MP Materials future revenue, earnings and margins to a financial forecast and then to a fair value estimate. On Simply Wall St, Narratives live in the Community page and are easy to use, allowing you to plug in your assumptions, see an implied fair value and then compare that fair value to the current share price to decide whether MP looks like a buy, hold or sell based on your story. Because Narratives update dynamically as new information, such as earnings, contract wins or news about the Saudi refinery venture, flows in, your thesis stays aligned with reality rather than a static snapshot. For example, one investor might build a bullish Narrative that leans into government backed contracts, downstream magnet margins and a fair value near the higher analyst target around $85.0. In contrast, a more cautious investor could emphasize execution, concentration and regulatory risks to arrive at a fair value closer to the low end near $65.0. Yet both are using the same structured Narrative tool to make clearer, more disciplined decisions.

Do you think there's more to the story for MP Materials? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MP

High growth potential with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion