- United States

- /

- Metals and Mining

- /

- NYSE:HL

Hecla Mining (HL) Valuation Check After Record Results, Strong Silver Prices and S&P MidCap 400 Inclusion

Reviewed by Simply Wall St

Hecla Mining (HL) has suddenly jumped onto more watchlists after a banner year, with record results, strong silver prices, and an upcoming move into the S&P MidCap 400 that is putting the stock squarely in focus.

See our latest analysis for Hecla Mining.

That surge is not happening in a vacuum, with a roughly 273.95% year to date share price return and a 291.14% one year total shareholder return reflecting powerful momentum as record results, index inclusion and unusual options activity reset market expectations.

If Hecla’s run has you thinking about what else is moving, this could be a good moment to discover fast growing stocks with high insider ownership.

Yet with shares now trading above the average analyst target and expectations soaring on silver strength, is Hecla still a mispriced growth story, or are investors already paying upfront for years of future upside?

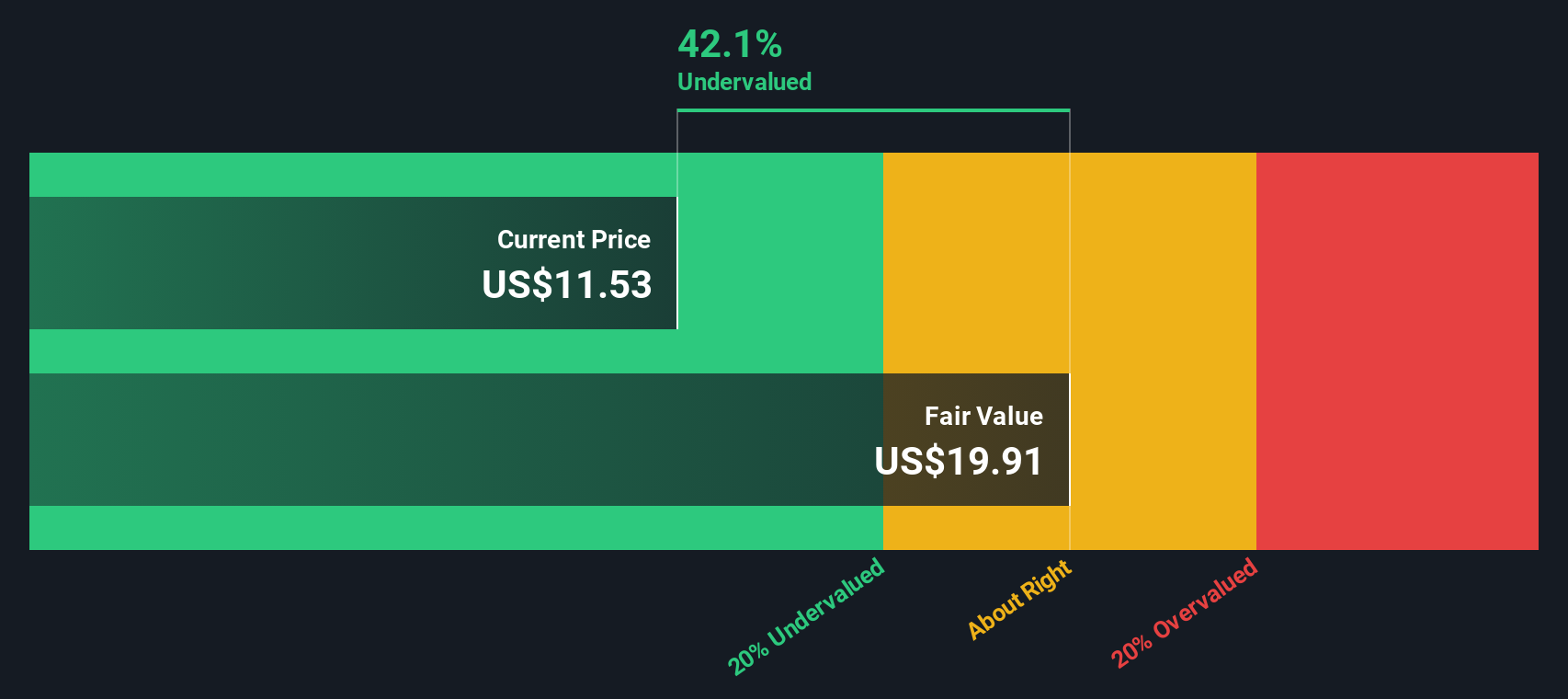

Most Popular Narrative: 35.2% Overvalued

With Hecla Mining last closing at $19.67 against a narrative fair value of $14.55, the story leans toward a stretched valuation built on ambitious assumptions.

The analysts have a consensus price target of $8.361 for Hecla Mining based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $12.5, and the most bearish reporting a price target of just $6.5.

Want to see how modest revenue trends combine with sharply rising margins to justify such a rich future earnings multiple? The full narrative reveals the math behind that premium.

Result: Fair Value of $14.55 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, steadily rising capital and regulatory costs, along with potential permitting delays at key projects, could quickly erode the margin expansion this premium narrative assumes.

Find out about the key risks to this Hecla Mining narrative.

Another View: DCF Points the Other Way

While the narrative fair value suggests Hecla is 35.2% overvalued, our DCF model lands in a very different place, implying shares are trading at a steep 52.6% discount to fair value. If the cash flows are right, is the market badly mispricing this momentum story?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Hecla Mining for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 913 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Hecla Mining Narrative

If you see the story differently or want to dig into the numbers yourself, you can craft a complete narrative in just minutes: Do it your way.

A great starting point for your Hecla Mining research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready for your next investing edge?

Before the market moves without you, tap into fresh opportunities using the Simply Wall St screener. High conviction ideas emerge from real fundamentals and data driven insight.

- Capitalize on overlooked value by targeting these 913 undervalued stocks based on cash flows that the market has not fully appreciated yet.

- Catch powerful income opportunities early with these 13 dividend stocks with yields > 3% that can strengthen your portfolio’s cash flow.

- Position yourself ahead of the next technological wave through these 28 quantum computing stocks shaping tomorrow’s computing landscape.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Hecla Mining might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HL

Hecla Mining

Provides precious and base metals in the United States, Canada, Japan, Korea, and China.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Clarivate Stock: When Data Becomes the Backbone of Innovation and Law

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion