Advertisement

- United States

- /

- Basic Materials

- /

- NYSE:EXP

How Investors Are Reacting To Eagle Materials (EXP) Cement Strength Offsetting Wallboard Weakness

Simply Wall St

Reviewed by Sasha Jovanovic

- Eagle Materials recently reported that steady growth in its cement and aggregates businesses, supported by an aggregates acquisition, is helping counter weak demand in its gypsum wallboard segment amid a soft housing market.

- This mix of resilient cash generation, ongoing buybacks and dividends, and a bullish independent thesis on its construction exposure has drawn attention to how well the company may be positioned for a future housing upturn.

- Next, we’ll examine how this resilience in cement and aggregates, alongside continued cash returns, may influence Eagle Materials’ investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Eagle Materials Investment Narrative Recap

To own Eagle Materials, you have to believe that its cement and aggregates operations and disciplined capital returns can offset a weak wallboard cycle until housing activity improves. The latest update, showing steady Heavy Materials growth and solid cash generation despite soft wallboard demand, does not materially change the near term risk that prolonged housing affordability issues keep wallboard volumes and margins under pressure.

Against that backdrop, the company’s decision to maintain its regular US$0.25 per share quarterly dividend, most recently affirmed for payment in January 2026, stands out. Continued dividends, alongside buybacks, support the current investment case that Eagle can keep returning cash even as earnings growth moderates, but they also sharpen the question of how much financial flexibility it retains if construction markets or input costs move against it.

Yet beneath the strength in cement and aggregates, investors should be aware of how concentrated regional exposure could magnify the impact of...

Read the full narrative on Eagle Materials (it's free!)

Eagle Materials' narrative projects $2.6 billion revenue and $524.5 million earnings by 2028. This requires 3.8% yearly revenue growth and about a $71.6 million earnings increase from $452.9 million today.

Uncover how Eagle Materials' forecasts yield a $251.70 fair value, a 13% upside to its current price.

Exploring Other Perspectives

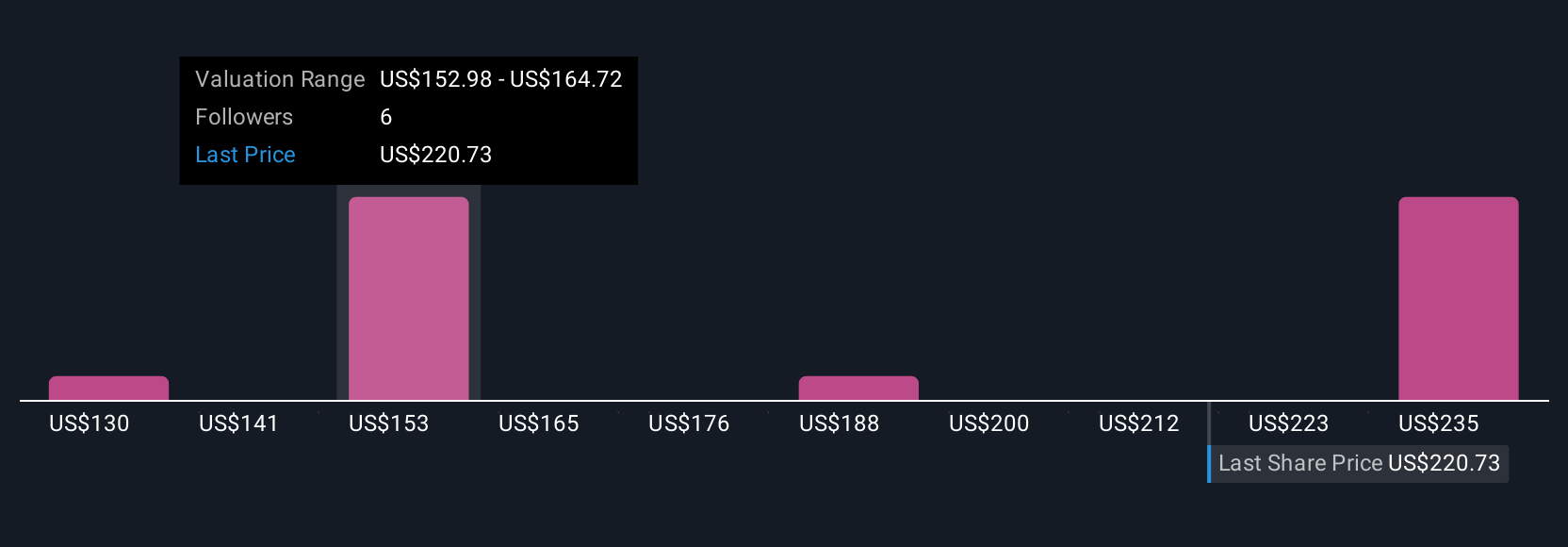

Four members of the Simply Wall St Community value Eagle Materials between US$129.50 and US$451.44 per share, highlighting sharply different expectations. When you set those views against ongoing weakness in wallboard demand, it underlines how important your own assumptions about the housing cycle will be for interpreting the company’s outlook.

Explore 4 other fair value estimates on Eagle Materials - why the stock might be worth 42% less than the current price!

Build Your Own Eagle Materials Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Eagle Materials research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Eagle Materials research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Eagle Materials' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Eagle Materials might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EXP

Eagle Materials

Through its subsidiaries, manufactures and sells heavy construction products and light building materials in the United States.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

54 followersusers have followed this narrative

6 commentsusers have commented on this narrative

17 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15081.9% undervalued

49 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

54 followersusers have followed this narrative

6 commentsusers have commented on this narrative

17 likesusers have liked this narrative