Advertisement

- United States

- /

- Chemicals

- /

- NYSE:ESI

The Returns At Element Solutions (NYSE:ESI) Aren't Growing

What trends should we look for it we want to identify stocks that can multiply in value over the long term? Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. However, after briefly looking over the numbers, we don't think Element Solutions (NYSE:ESI) has the makings of a multi-bagger going forward, but let's have a look at why that may be.

Understanding Return On Capital Employed (ROCE)

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Element Solutions is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

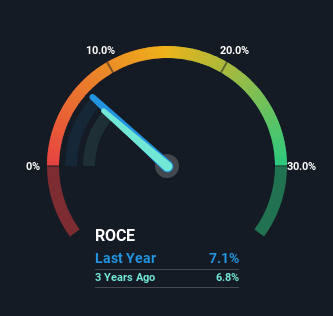

0.071 = US$336m ÷ (US$5.1b - US$384m) (Based on the trailing twelve months to September 2024).

Therefore, Element Solutions has an ROCE of 7.1%. On its own, that's a low figure but it's around the 8.1% average generated by the Chemicals industry.

View our latest analysis for Element Solutions

Above you can see how the current ROCE for Element Solutions compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free analyst report for Element Solutions .

The Trend Of ROCE

Over the past five years, Element Solutions' ROCE and capital employed have both remained mostly flat. This tells us the company isn't reinvesting in itself, so it's plausible that it's past the growth phase. So don't be surprised if Element Solutions doesn't end up being a multi-bagger in a few years time.

Our Take On Element Solutions' ROCE

In a nutshell, Element Solutions has been trudging along with the same returns from the same amount of capital over the last five years. Yet to long term shareholders the stock has gifted them an incredible 120% return in the last five years, so the market appears to be rosy about its future. But if the trajectory of these underlying trends continue, we think the likelihood of it being a multi-bagger from here isn't high.

On a separate note, we've found 1 warning sign for Element Solutions you'll probably want to know about.

While Element Solutions isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

Valuation is complex, but we're here to simplify it.

Discover if Element Solutions might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:ESI

Element Solutions

Operates as a specialty chemicals technology company in the United States, China, and internationally.

Adequate balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Gain Therapeutics ·

The Market Is Sleeping on This Parkinson's Biotech - And I Think That's a Mistake

Fair Value:US$7.675.4% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

11 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.2538.0% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

TE

TechMegaTrends on Bambuser ·

Bambuser is today the only listed company in Europe that simultaneously possesses an 85% gross margin, proprietary AI infrastructure for the

Fair Value:SEK 238.2690.2% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

HE

HedgeY on Constellium ·

Constellium jet another cyclical aluminum processor, or a mispriced aluminum platform?

Fair Value:US$3410.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

DI

DinTang on Bumitama Agri ·

Expectations focused on stable output, disciplined costs, and continued cash returns to shareholders

Fair Value:S$2.4620.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$5809.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

Martimmfonseca on Meta Platforms ·

Meta Could Reach $653–$792 Over the Next Five Years

Fair Value:US$6532.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3952.7% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

42 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

38 followersusers have followed this narrative

11 commentsusers have commented on this narrative

32 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$587.3134.6% undervalued

1355 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

MS

msd on Life Insurance Corporation of India ·

HOwmuch ever attractive , no one buying LIC shares, dont know why.

0

|0