Advertisement

- United States

- /

- Chemicals

- /

- NYSE:EMN

Does the Recent 34% Share Price Drop Offer an Opportunity in Eastman Chemical?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Eastman Chemical is trading at a bargain or showing warning signs? You are not alone. Let us break down exactly what the numbers suggest.

- While the stock saw a 2.2% bump this past week, it is still down almost 34% year-to-date and an even steeper 42% over the past 12 months. This makes it a candidate for investors interested in value and volatility.

- Recent headlines have focused on ongoing industry challenges and shifting demand for specialty materials. Some analysts are discussing how these external pressures may be shaping investor sentiment, as well as what it could mean for a potential turnaround in Eastman Chemical's share price.

- Eastman Chemical currently clocks a valuation score of 6 out of 6, suggesting that it screens as undervalued on all our major checks. Next, let us dive into the major valuation methods used for assessing stocks like Eastman Chemical. We will also highlight a way to better understand what this number means at the end of the article.

Find out why Eastman Chemical's -42.2% return over the last year is lagging behind its peers.

Approach 1: Eastman Chemical Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates what a business is worth today by projecting its future cash flows and discounting them back to their present value. For Eastman Chemical, analysts start by looking at the company's most recent Free Cash Flow, which stands at $330.8 million. This figure represents the cash the company generates after expenses, before any debt repayments or dividends.

Analyst estimates provide projections for the next five years, with expected Free Cash Flow rising to $738 million in 2028. Simply Wall St then extrapolates these growth rates further out to 2035, using expected annual growth rates that gradually slow. Over the next ten years, the estimates suggest that Eastman Chemical's cash generation could more than double from current levels. This reflects analyst expectations for recovery and expansion in its specialty materials business.

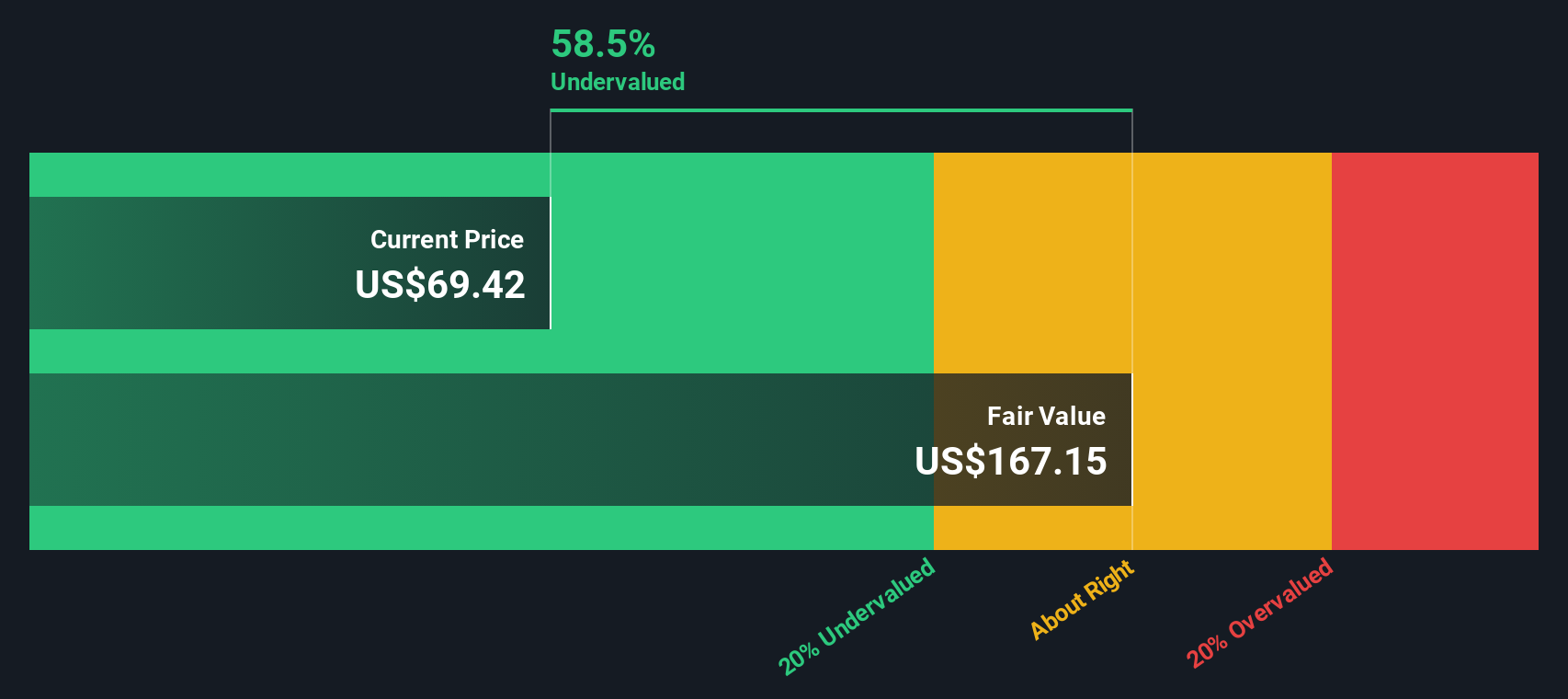

The DCF model values Eastman Chemical shares at $117.89 each. This is 50.2% higher than the current share price, which implies that the stock trades at a significant discount to its intrinsic value based on projected future cash flows. In simple terms, the market currently appears to be undervaluing Eastman Chemical's cash-generating potential.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Eastman Chemical is undervalued by 50.2%. Track this in your watchlist or portfolio, or discover 924 more undervalued stocks based on cash flows.

Approach 2: Eastman Chemical Price vs Earnings

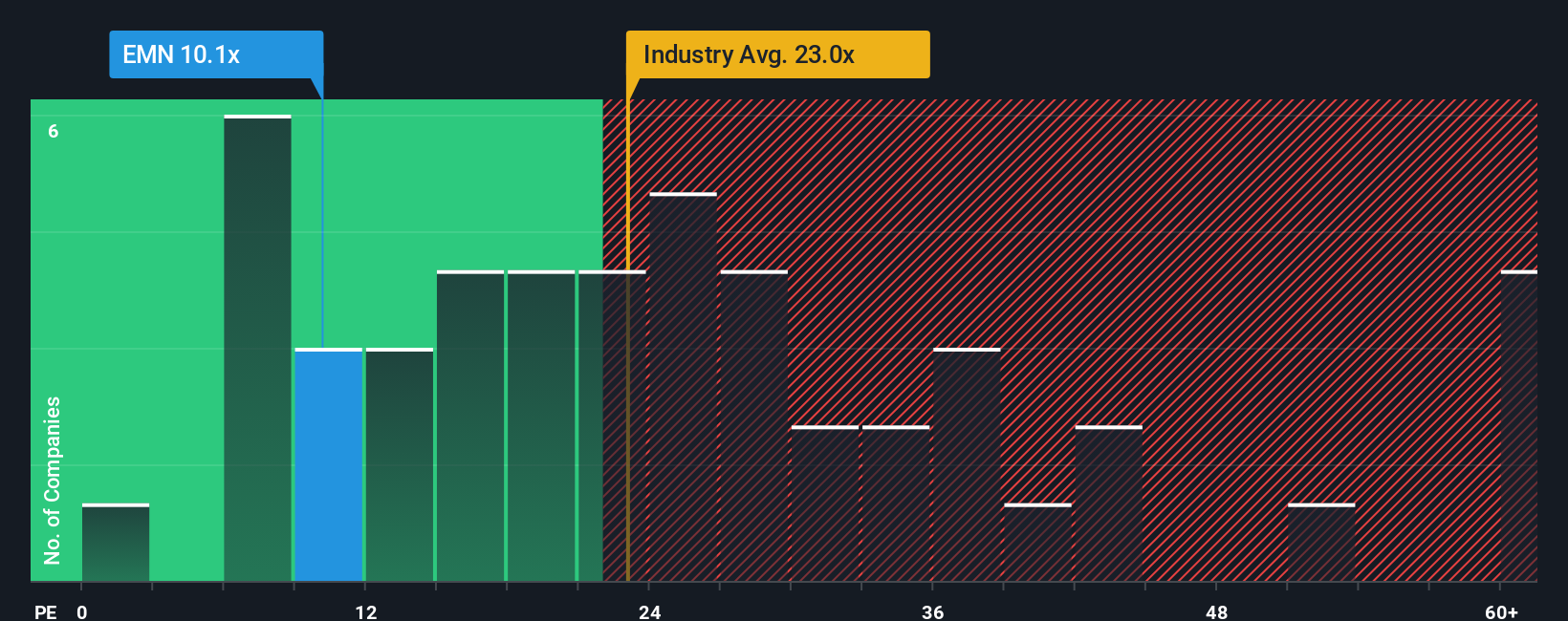

The Price-to-Earnings (PE) ratio is a widely used valuation measure for profitable companies like Eastman Chemical, as it directly compares a company's market price to its actual earnings. For investors, a lower PE may indicate an undervalued stock, while a higher PE can reflect either superior growth prospects or heightened risk.

Growth expectations and perceived risk both play a major role in what is considered a “normal” or “fair” PE ratio for a company. Fast-growing or lower-risk companies generally warrant higher PE multiples, while slower growers or riskier businesses usually trade at lower PEs. It is important to view this number in context, comparing not only to peers but also to what is reasonable for this company’s growth profile.

Currently, Eastman Chemical trades at a PE ratio of 9.58x, which is noticeably lower than both its peer average (19.28x) and the chemicals industry average (22.20x). However, benchmarks like industry averages do not always tell the full story. Simply Wall St's proprietary Fair Ratio for Eastman Chemical is 19.60x, reflecting a more nuanced calculation that factors in the company's projected earnings growth, risk profile, profit margins, and market cap. This approach provides a more tailored benchmark than a simple comparison to peers or the broader industry, ensuring a fairer assessment unique to Eastman Chemical's circumstances.

Compared to its Fair Ratio, Eastman Chemical’s actual PE is sharply lower. This suggests its shares may be undervalued when adjusting for all relevant factors.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1440 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Eastman Chemical Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. In simple terms, a Narrative is your unique story about a company. It connects your own expectations (such as fair value, future revenue, earnings, and margins) with what is happening in the real world. Narratives link these personal perspectives to financial forecasts, allowing you to see how a company’s story translates into numbers and fair value estimates.

On Simply Wall St’s Community page, millions of investors use Narratives as an easy and accessible tool to capture their investment views and see exactly how they stack up against the current market price. By comparing your Narrative’s Fair Value to today’s price, you can quickly spot whether the stock looks like a buy or a sell for you. The best part is that Narratives are dynamic. Whenever new news or earnings reports arrive, the valuations and assumptions in your Narrative are automatically updated to reflect the latest information.

For example, some Eastman Chemical investors might believe aggressive cost savings and global recycling momentum will drive future growth, resulting in a bullish Narrative with a fair value above $100. Others, more cautious due to weak industrial demand and margin pressure, may set their Narrative closer to $60. No matter your perspective, Narratives help you make decisions rooted in your own reasoning, empowering you to invest smarter and with more confidence.

Do you think there's more to the story for Eastman Chemical? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Eastman Chemical might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EMN

Eastman Chemical

Operates as a specialty materials company in the United States, China, and internationally.

Undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

19 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative