Advertisement

- United States

- /

- Life Sciences

- /

- NYSE:DNA

Ginkgo Bioworks Holdings, Inc. (NYSE:DNA) Stocks Pounded By 27% But Not Lagging Industry On Growth Or Pricing

To the annoyance of some shareholders, Ginkgo Bioworks Holdings, Inc. (NYSE:DNA) shares are down a considerable 27% in the last month, which continues a horrid run for the company. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 34% share price drop.

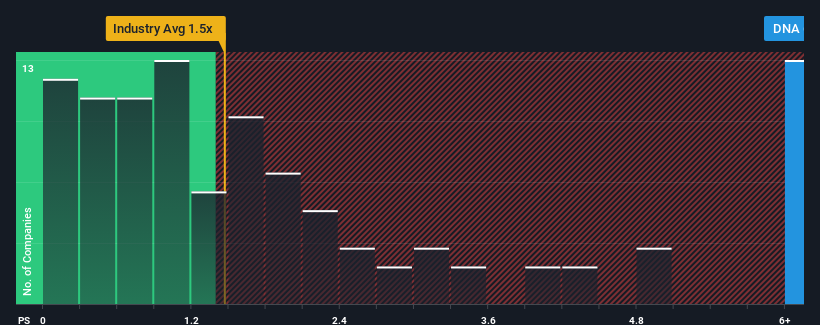

Even after such a large drop in price, when almost half of the companies in the United States' Chemicals industry have price-to-sales ratios (or "P/S") below 1.5x, you may still consider Ginkgo Bioworks Holdings as a stock not worth researching with its 6.2x P/S ratio. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for Ginkgo Bioworks Holdings

How Has Ginkgo Bioworks Holdings Performed Recently?

Recent times haven't been great for Ginkgo Bioworks Holdings as its revenue has been falling quicker than most other companies. It might be that many expect the dismal revenue performance to recover substantially, which has kept the P/S from collapsing. If not, then existing shareholders may be very nervous about the viability of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Ginkgo Bioworks Holdings will help you uncover what's on the horizon.What Are Revenue Growth Metrics Telling Us About The High P/S?

In order to justify its P/S ratio, Ginkgo Bioworks Holdings would need to produce outstanding growth that's well in excess of the industry.

Retrospectively, the last year delivered a frustrating 47% decrease to the company's top line. Even so, admirably revenue has lifted 228% in aggregate from three years ago, notwithstanding the last 12 months. So we can start by confirming that the company has generally done a very good job of growing revenue over that time, even though it had some hiccups along the way.

Looking ahead now, revenue is anticipated to climb by 19% per year during the coming three years according to the seven analysts following the company. That's shaping up to be materially higher than the 8.1% each year growth forecast for the broader industry.

With this in mind, it's not hard to understand why Ginkgo Bioworks Holdings' P/S is high relative to its industry peers. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From Ginkgo Bioworks Holdings' P/S?

A significant share price dive has done very little to deflate Ginkgo Bioworks Holdings' very lofty P/S. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our look into Ginkgo Bioworks Holdings shows that its P/S ratio remains high on the merit of its strong future revenues. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. Unless these conditions change, they will continue to provide strong support to the share price.

Plus, you should also learn about these 2 warning signs we've spotted with Ginkgo Bioworks Holdings.

If you're unsure about the strength of Ginkgo Bioworks Holdings' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:DNA

Ginkgo Bioworks Holdings

Develops a platform for cell programming in the United States.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets