Advertisement

- United States

- /

- Packaging

- /

- NYSE:CCK

Here's What Analysts Are Forecasting For Crown Holdings, Inc. After Its Yearly Results

It's been a good week for Crown Holdings, Inc. (NYSE:CCK) shareholders, because the company has just released its latest full-year results, and the shares gained 5.0% to US$79.60. It looks like the results were a bit of a negative overall. While revenues of US$12b were in line with analyst predictions, statutory earnings were less than expected, missing estimates by 2.4% to hit US$3.78 per share. Analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We thought readers would find it interesting to see analysts' latest (statutory) post-earnings forecasts for next year.

View our latest analysis for Crown Holdings

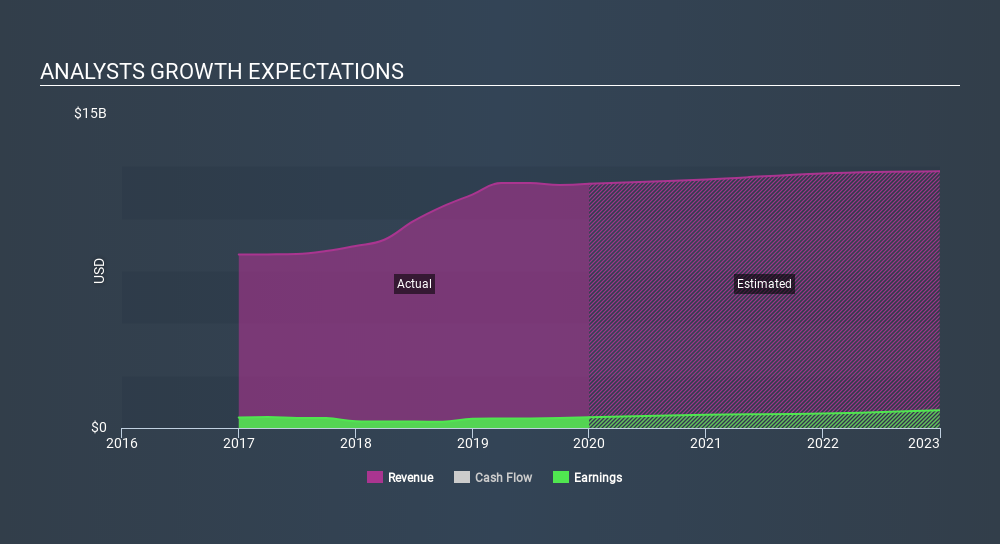

Following last week's earnings report, Crown Holdings's 14 analysts are forecasting 2020 revenues to be US$11.9b, approximately in line with the last 12 months. Statutory earnings per share are expected to leap 23% to US$4.68. Before this earnings report, analysts had been forecasting revenues of US$11.9b and earnings per share (EPS) of US$4.75 in 2020. So it's pretty clear that, although analysts have updated their estimates, there's been no major change in expectations for the business following the latest results.

Analysts reconfirmed their price target of US$83.47, showing that the business is executing well and in line with expectations. The consensus price target just an average of individual analyst targets, so - considering that the price target changed, it would be handy to see how wide the range of underlying estimates is. Currently, the most bullish analyst values Crown Holdings at US$100.00 per share, while the most bearish prices it at US$61.00. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

In addition, we can look to Crown Holdings's past performance and see whether business is expected to improve, and if the company is expected to perform better than wider market. We would highlight that Crown Holdings's revenue growth is expected to slow, with forecast 1.8% increase next year well below the historical 6.7%p.a. growth over the last five years. By way of comparison, other companies in this market with analyst coverage, are forecast to grow their revenue at 2.3% per year. Factoring in the forecast slowdown in growth, it seems obvious that analysts still expect Crown Holdings to grow slower than the wider market.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with analysts reconfirming that earnings per share are expected to continue performing in line with their prior expectations. On the plus side, there were no major changes to revenue estimates; although analyst forecasts imply revenues will perform worse than the wider market. The consensus price target held steady at US$83.47, with the latest estimates not enough to have an impact on analysts' estimated valuations.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for Crown Holdings going out to 2022, and you can see them free on our platform here..

It might also be worth considering whether Crown Holdings's debt load is appropriate, using our debt analysis tools on the Simply Wall St platform, here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:CCK

Crown Holdings

Engages in the packaging business in the United States and internationally.

Proven track record and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|18.7% undervalued

TI

Community Contributor