- United States

- /

- Metals and Mining

- /

- NYSE:B

Is It Too Late to Consider Barrick Mining After a 185.5% Year to Date Surge?

Reviewed by Bailey Pemberton

- If you have been wondering whether Barrick Mining is still a buy after its big run, this breakdown will help you decide if the market is getting ahead of itself or finally waking up.

- The stock has surged recently, climbing 5.2% over the last week, 24.7% in the past month, and an eye catching 185.5% year to date, while its 1 year gain sits at 198.6% and it is up 130.2% over 5 years.

- Much of this momentum reflects renewed interest in miners as investors rotate back into real assets and reposition for a different rate and inflation environment. Alongside that, sector wide exploration successes and capital discipline narratives have put large, established players like Barrick Mining back on the radar for both growth and defensive positioning.

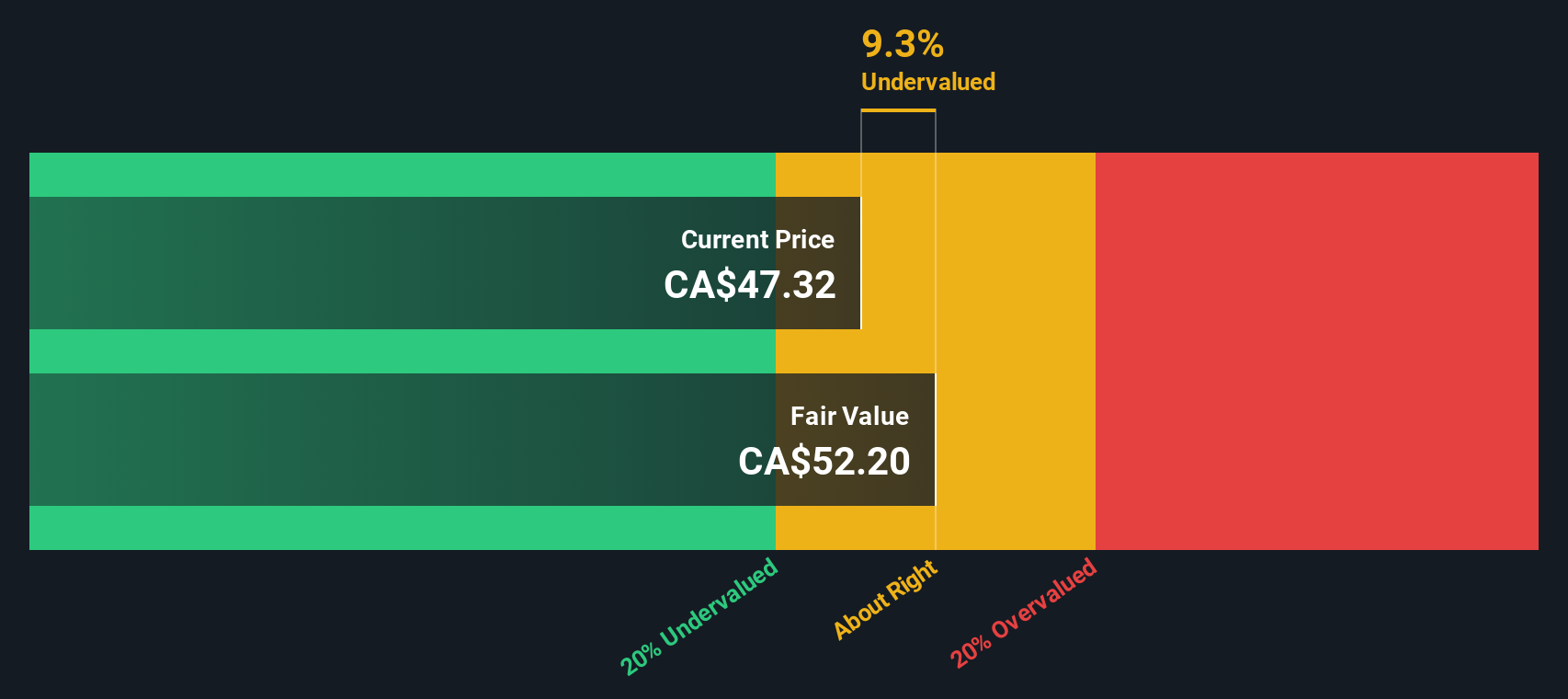

- Even after that rally, Barrick Mining scores a 5/6 valuation check score. This suggests it still screens as undervalued on most of our metrics. Next we will unpack those different valuation approaches, before finishing with a more complete way to judge what the stock is really worth.

Approach 1: Barrick Mining Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth by projecting the cash it can generate in the future and then discounting those cash flows back to today in dollar terms.

For Barrick Mining, the latest twelve month free cash flow is about $2.57 billion. Analysts and internal projections expect this to increase gradually, with forecast free cash flow reaching around $9.07 billion by 2029 and continuing to rise into the next decade. These later years are extrapolated beyond formal analyst coverage using a 2 Stage Free Cash Flow to Equity model. This approach assumes faster growth initially, followed by a tapering to more sustainable levels over time.

When all those projected cash flows are discounted back, the model arrives at an intrinsic value of $124.60 per share. Compared to the current share price, this suggests the stock is trading at roughly a 63.4% discount, indicating the market may be pricing Barrick below its long term cash generating potential.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Barrick Mining is undervalued by 63.4%. Track this in your watchlist or portfolio, or discover 899 more undervalued stocks based on cash flows.

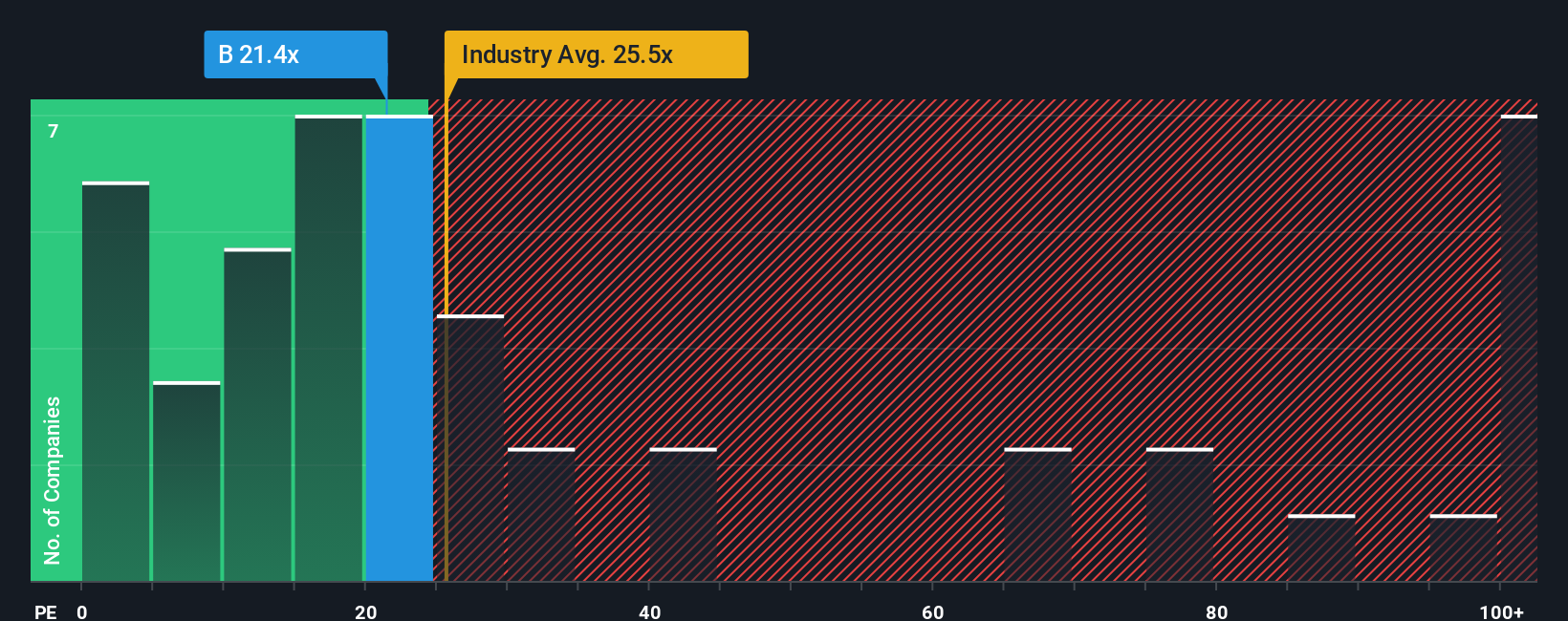

Approach 2: Barrick Mining Price vs Earnings

For profitable companies, the price to earnings ratio is often the simplest way to think about valuation, because it links what investors are paying today to the profits the business is already generating. A higher PE can be justified if investors expect stronger, more reliable growth, while slower growth or higher risk usually calls for a lower, more conservative multiple.

Barrick Mining currently trades on a PE of about 21.5x, which sits below both the Metals and Mining industry average of roughly 25.4x and the peer group average of around 25.8x. On the surface, that discount suggests the market is still applying a modest penalty to Barrick relative to similar miners, despite its improving fundamentals and recent share price strength.

Simply Wall St’s Fair Ratio framework goes a step further than these simple comparisons. It estimates what PE a company should trade on, given its earnings growth outlook, risk profile, profit margins, industry and market cap. For Barrick, the Fair Ratio is 26.8x, meaning the shares trade at a meaningful discount to what would be expected on these fundamentals, which points to further upside if the company delivers as forecast.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1458 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Barrick Mining Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of Barrick Mining’s future to a set of numbers and a fair value estimate on Simply Wall St’s Community page.

A Narrative is your story about a company, captured in assumptions about its future revenue, earnings and margins, which are then translated into a forecast and a Fair Value. You can compare this to today’s share price to help inform a decision to buy, hold or sell.

Because Narratives live on the platform used by millions of investors and update dynamically when new information such as earnings results or major project news arrives, they stay aligned with the latest data without you having to rebuild your model from scratch.

For Barrick Mining, one investor’s bullish Narrative might assume a strong commodity super cycle, 4.5 percent annual revenue growth, net margins recovering to 15 percent and a Fair Value around $20.44 per share. A more cautious investor might plug in slower growth, more political risk and a much lower Fair Value, yet both can quickly see how far their view sits from the current market price.

Do you think there's more to the story for Barrick Mining? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Barrick Mining might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:B

Barrick Mining

Engages in the exploration, development, production, and sale of mineral properties.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion