Advertisement

- United States

- /

- Chemicals

- /

- NYSE:ASH

Ashland's (NYSE:ASH) Shareholders Will Receive A Bigger Dividend Than Last Year

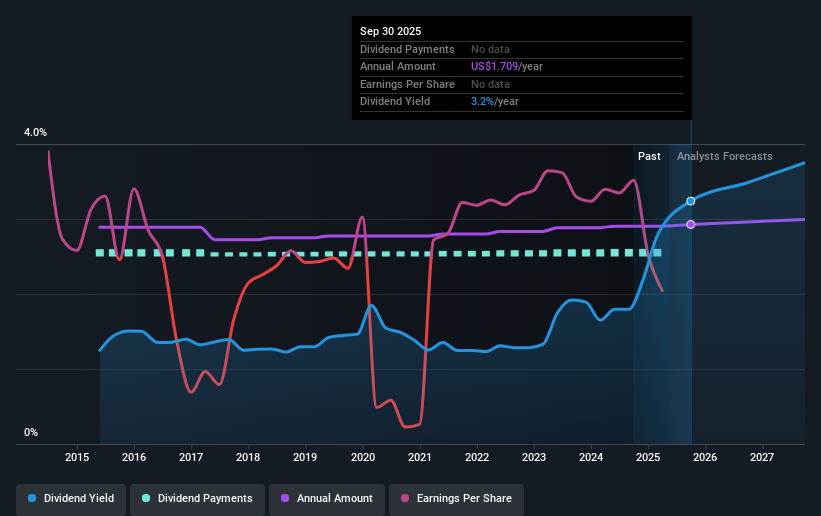

The board of Ashland Inc. (NYSE:ASH) has announced that it will be increasing its dividend by 2.5% on the 15th of June to $0.415, up from last year's comparable payment of $0.405. This will take the dividend yield to an attractive 3.1%, providing a nice boost to shareholder returns.

Ashland's Future Dividend Projections Seem Positive

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Ashland is unprofitable despite paying a dividend, and it is paying out 224% of its free cash flow. This makes us feel that the dividend will be hard to maintain.

According to analysts, EPS should be several times higher next year. If the dividend continues along recent trends, we estimate the payout ratio will be 28%, so there isn't too much pressure on the dividend.

See our latest analysis for Ashland

Dividend Volatility

While the company has been paying a dividend for a long time, it has cut the dividend at least once in the last 10 years. Since 2015, the annual payment back then was $1.36, compared to the most recent full-year payment of $1.62. This implies that the company grew its distributions at a yearly rate of about 1.8% over that duration. It's encouraging to see some dividend growth, but the dividend has been cut at least once, and the size of the cut would eliminate most of the growth anyway, which makes this less attractive as an income investment.

The Company Could Face Some Challenges Growing The Dividend

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. Ashland has seen EPS rising for the last five years, at 48% per annum. Even though the company is not profitable, it is growing at a solid clip. If profitability can be achieved soon and growth continues apace, this stock could certainly turn into a solid dividend payer.

The Dividend Could Prove To Be Unreliable

Overall, we always like to see the dividend being raised, but we don't think Ashland will make a great income stock. In general, the distributions are a little bit higher than we would like, but we can't ignore the fact the quickly growing earnings gives this stock great potential in the future. We would be a touch cautious of relying on this stock primarily for the dividend income.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Taking the debate a bit further, we've identified 1 warning sign for Ashland that investors need to be conscious of moving forward. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:ASH

Ashland

Provides additives and specialty ingredients in the North and Latin America, Europe, Asia Pacific, and internationally.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|7.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|93.3% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.4% undervalued

GM

Community Contributor