Advertisement

- United States

- /

- Chemicals

- /

- NYSE:ALB

Is Albemarle's (ALB) Debt Profile a Strategic Move or a Sign of Shifting Industry Dynamics?

Simply Wall St

Reviewed by Sasha Jovanovic

- In late November 2025, recent analyses have raised concerns about Albemarle’s financial strength and growth prospects as the company faces industry headwinds and rising debt metrics.

- An interesting insight is that Albemarle’s lower than expected return on invested capital and weaker interest coverage compare unfavorably to peers, highlighting rising investor uncertainty about its ability to generate consistent value.

- We'll examine how increasing concerns over Albemarle’s financial resilience may shape its future investment narrative and industry position.

AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Albemarle Investment Narrative Recap

To be a shareholder in Albemarle today, you need to believe in the company's long-term relevance in global energy storage and specialty chemicals, despite heightened short-term investor concerns about profitability, debt levels, and value creation. The recent spotlight on Albemarle’s below-average return on invested capital and compressed interest coverage amplifies worries about its ability to fund operations and maintain financial flexibility. While this news draws attention to current challenges, it does not fundamentally alter the near-term catalyst: stabilization of lithium prices, or the primary risk of persistent industry overcapacity. Of the recent Albemarle news, the $181 million goodwill impairment announced in Q3 2025 is the most relevant in the context of ongoing financial strength questions. This charge, alongside a second consecutive quarterly net loss, highlights the impact of weaker underlying market conditions and hints at a cautious approach to asset values, shaping both short-term performance and future capital allocation decisions. In contrast, investors should also be aware of the continued risk from oversupplied lithium markets and its effect on Albemarle’s margins if conditions persist...

Read the full narrative on Albemarle (it's free!)

Albemarle's outlook projects $6.9 billion in revenue and $1.1 billion in earnings by 2028. This relies on an annual revenue growth rate of 11.5% and a $2.2 billion increase in earnings from the current level of -$1.1 billion.

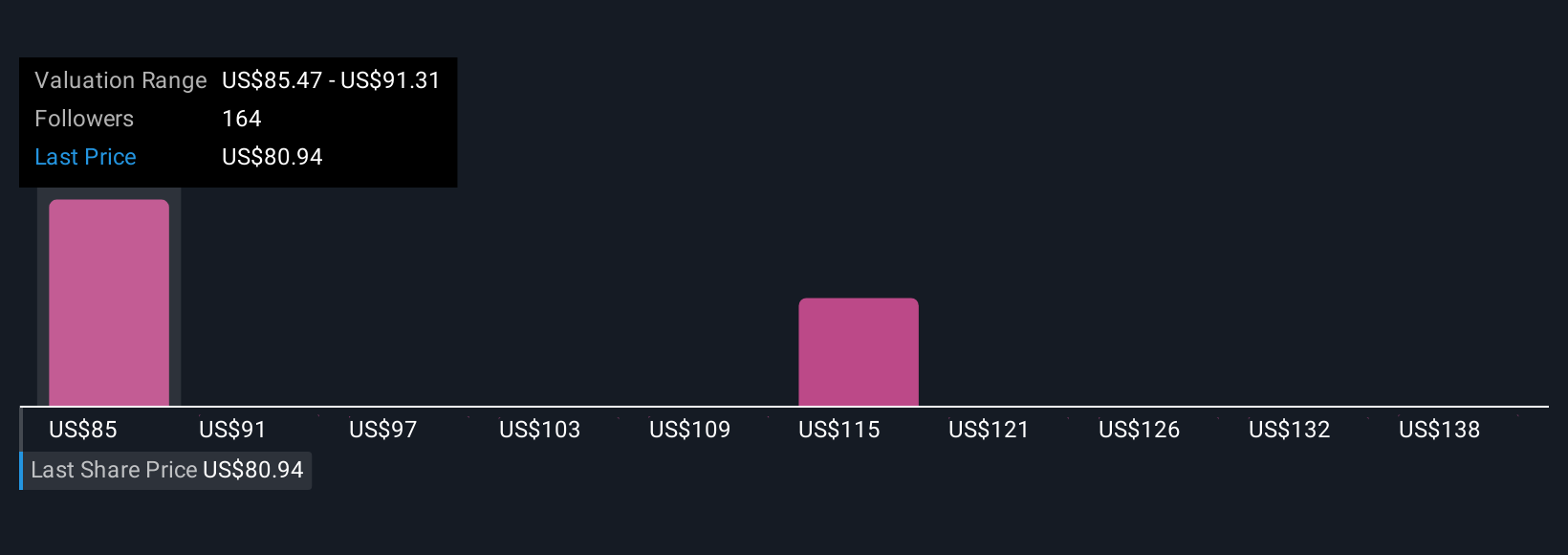

Uncover how Albemarle's forecasts yield a $103.01 fair value, a 21% downside to its current price.

Exploring Other Perspectives

Ten members of the Simply Wall St Community estimate Albemarle’s fair value between US$88.90 and US$143.88, reflecting considerable variation. These views contrast with rising concerns over Albemarle’s ability to generate shareholder value, which continues to influence investor sentiment and the company’s outlook.

Explore 10 other fair value estimates on Albemarle - why the stock might be worth 32% less than the current price!

Build Your Own Albemarle Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Albemarle research is our analysis highlighting 1 key reward that could impact your investment decision.

- Our free Albemarle research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Albemarle's overall financial health at a glance.

Interested In Other Possibilities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Find companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 35 best rare earth metal stocks of the very few that mine this essential strategic resource.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ALB

Adequate balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

139 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative