- United States

- /

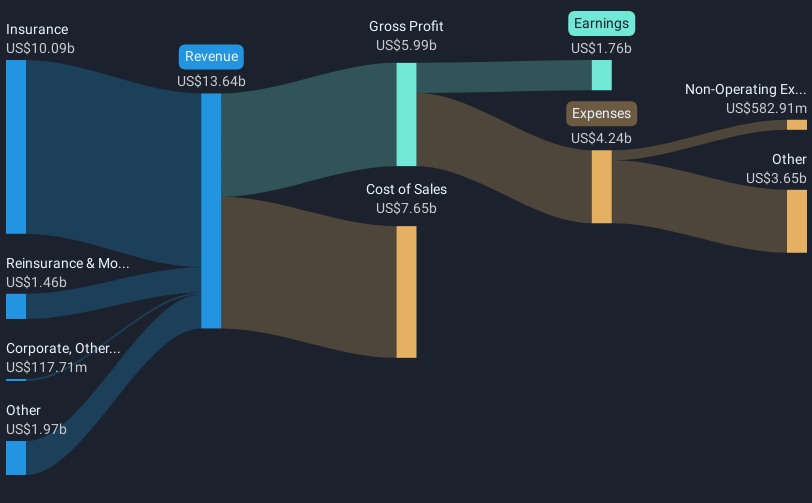

- Insurance

- /

- NYSE:WRB

W. R. Berkley (NYSE:WRB) Jumps 21% Last Quarter Following Strong Q4 2024 Earnings

Reviewed by Simply Wall St

W. R. Berkley (NYSE:WRB) recently announced key initiatives, such as appointing Heath Kidd as Executive Vice President and forming Berkley Embedded Solutions to enhance its insurance offerings, which may relate to its 21% stock price increase last quarter. The company's strong Q4 2024 earnings, alongside share buybacks totaling $67 million, likely supported investor confidence. Despite broader market declines amid tariff concerns and economic uncertainty, WRB’s focus on innovation appears to have contributed to its outperformance, surpassing the general market trend, which only saw a 5.5% increase in the past year.

Buy, Hold or Sell W. R. Berkley? View our complete analysis and fair value estimate and you decide.

Over the past five years, W. R. Berkley Corporation has delivered a substantial total shareholder return of 258.16%. Several factors contributed to this impressive performance. Technological investments and a strategic focus on specialty areas like workers' compensation have strengthened the company’s competitive position, enhancing underwriting margins and investment income. The launch of Berkley Embedded Solutions marks significant growth in tailored insurance products, further driving revenue.

Frequent share repurchases, totaling over $67 million in early 2025, have supported shareholder value while business expansions, such as Berkley Construction Solutions in 2022, have fueled revenue growth. Also, the company's ability to outperform the market and the insurance industry over the past year, while maintaining strong earnings growth, illustrates its robust operational management and financial resilience. Dividend payouts, including special dividends, have been consistent, contributing to the total returns experienced by shareholders.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if W. R. Berkley might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WRB

W. R. Berkley

An insurance holding company, operates as a commercial line writer worldwide.

Excellent balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Community Narratives