- United States

- /

- Insurance

- /

- NYSE:WDH

3 US Growth Stocks With High Insider Ownership And Up To 74% Earnings Growth

Reviewed by Simply Wall St

As the S&P 500 and Nasdaq Composite reach record highs, driven by a surge in technology stocks, investors are closely monitoring growth opportunities within the U.S. market. In this environment of heightened optimism, companies with strong earnings growth and significant insider ownership can be particularly appealing, as they often signal confidence from those who know the business best.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | 26% | 25.7% |

| Super Micro Computer (NasdaqGS:SMCI) | 14.4% | 24.3% |

| Duolingo (NasdaqGS:DUOL) | 14.6% | 41.6% |

| On Holding (NYSE:ONON) | 19.1% | 29.6% |

| Coastal Financial (NasdaqGS:CCB) | 18% | 46.1% |

| Clene (NasdaqCM:CLNN) | 21.6% | 60.2% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.5% |

| Alkami Technology (NasdaqGS:ALKT) | 10.9% | 98.6% |

| BBB Foods (NYSE:TBBB) | 22.9% | 43.3% |

| Credit Acceptance (NasdaqGS:CACC) | 14.1% | 50% |

Let's explore several standout options from the results in the screener.

Viemed Healthcare (NasdaqCM:VMD)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Viemed Healthcare, Inc. offers home medical equipment and post-acute respiratory healthcare services in the United States, with a market cap of approximately $337.58 million.

Operations: The company's revenue is primarily derived from its Sleep and Respiratory Disorders Sector, which generated $214.30 million.

Insider Ownership: 12.6%

Earnings Growth Forecast: 32.5% p.a.

Viemed Healthcare's earnings are projected to grow significantly at 32.5% annually, outpacing the US market's 15.4%. Revenue growth is forecast at 12.9% per year, also above market averages. Recent earnings reports show a positive trajectory with Q3 sales rising to US$58 million from US$49.4 million year-over-year and net income increasing to US$3.88 million from US$2.92 million, indicating strong operational performance without substantial insider trading activity recently noted.

- Take a closer look at Viemed Healthcare's potential here in our earnings growth report.

- The analysis detailed in our Viemed Healthcare valuation report hints at an inflated share price compared to its estimated value.

Enfusion (NYSE:ENFN)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Enfusion, Inc. offers software-as-a-service solutions for the investment management industry across various regions, with a market cap of approximately $1.28 billion.

Operations: The company's revenue from its online financial information provider segment amounts to $195.16 million.

Insider Ownership: 10.5%

Earnings Growth Forecast: 74.8% p.a.

Enfusion's earnings are forecast to grow significantly at 74.8% annually, surpassing the US market's 15.4%. Revenue is expected to increase by 16.7% per year, outpacing the broader market growth rate of 8.9%. Despite a decline in net profit margin from last year, insider buying has slightly exceeded selling recently. The company reported Q3 revenue of US$51.17 million and net income of US$1.42 million, with ongoing strategic leadership changes enhancing its growth trajectory.

- Click to explore a detailed breakdown of our findings in Enfusion's earnings growth report.

- Our expertly prepared valuation report Enfusion implies its share price may be lower than expected.

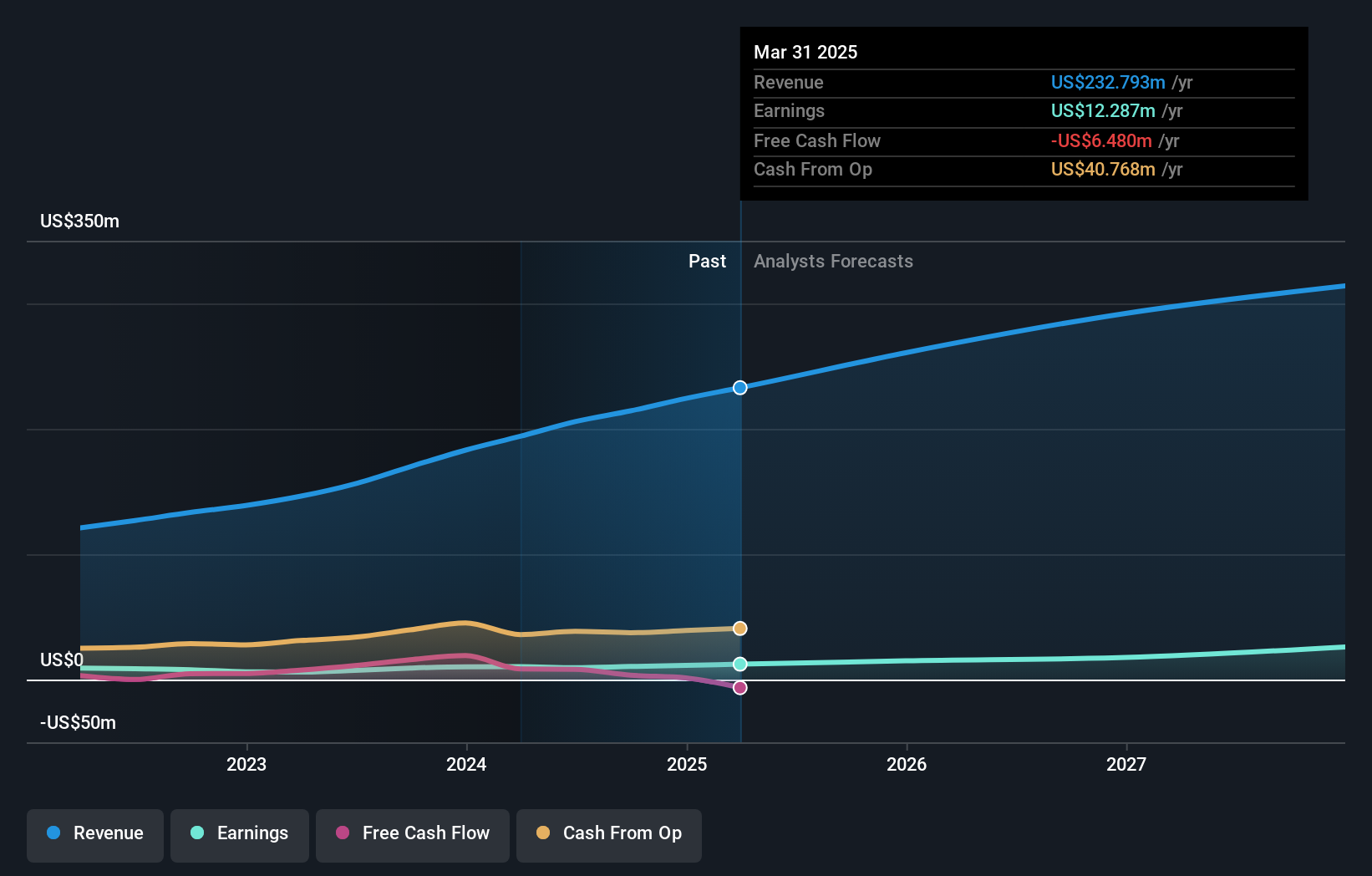

Waterdrop (NYSE:WDH)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Waterdrop Inc., with a market cap of $416.90 million, operates as an online insurance brokerage service connecting users with insurance products underwritten by companies in the People’s Republic of China.

Operations: The company's revenue primarily comes from its insurance segment, generating CN¥2.39 billion, followed by the crowd funding segment at CN¥212.66 million.

Insider Ownership: 21.7%

Earnings Growth Forecast: 20.8% p.a.

Waterdrop's recent financial results show a net income increase to CNY 88.29 million for Q2 2024, up from CNY 21.7 million the previous year, with sales slightly declining to CNY 676.16 million. The company announced a US$50 million share buyback program and a special cash dividend of US$0.02 per ADS. Trading below the market's P/E ratio at 11.6x, Waterdrop is poised for strong earnings growth at an expected annual rate of over 20%.

- Dive into the specifics of Waterdrop here with our thorough growth forecast report.

- The analysis detailed in our Waterdrop valuation report hints at an deflated share price compared to its estimated value.

Turning Ideas Into Actions

- Dive into all 211 of the Fast Growing US Companies With High Insider Ownership we have identified here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Waterdrop might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WDH

Waterdrop

Through its subsidiaries, provides online insurance brokerage services to match and connect users with related insurance products underwritten by insurance companies in the People’s Republic of China.

Flawless balance sheet and good value.