Advertisement

- United States

- /

- Insurance

- /

- NYSE:OSCR

Oscar Health (OSCR): Evaluating Valuation After Policy Proposal Sparks Investor Optimism

Simply Wall St

Reviewed by Simply Wall St

Oscar Health (OSCR) shares jumped after news broke that the White House may propose a two-year extension of Obamacare subsidies, expand eligibility, and introduce minimum premium payments. Investors are watching this policy closely, given its impact on ACA-focused insurers.

See our latest analysis for Oscar Health.

Oscar Health’s share price has been on a wild ride lately, thanks to the ACA subsidy news sending the stock up nearly 29% over the last week and sparking renewed investor interest. While the recent headlines fueled a burst of momentum, the longer-term picture is a bit more nuanced. Oscar’s one-year total shareholder return stands at just under 8%. Zooming out to three years, those who stuck around have seen a total return of 530%. Volatility comes with the territory, but Oscar remains a name to watch as the policy landscape evolves.

If health insurers’ rebound has caught your attention, consider exploring more opportunities among medical innovators—See the full list for free.

With Oscar shares rallying on fresh policy hopes, investors are left to wonder if the recent surge is just the start of a bigger move, or if the market has already priced in all the future growth potential.

Most Popular Narrative: 41% Overvalued

Oscar Health’s prevailing narrative puts fair value well below where shares last closed. Analyst expectations currently lag recent market enthusiasm, and with the current price well ahead of this fair value estimate, the stock faces a high bar to justify further upside.

Recent market-wide increases in morbidity within the individual ACA market highlight Oscar Health's vulnerability to dynamic risk pools, heightening uncertainty in claims costs and putting pressure on the company's ability to maintain or grow net margins and future earnings, even with planned repricing actions.

Curious why this narrative says Oscar needs nearly a new profit playbook to grow into its price? The forecast leans on bold assumptions for margin expansion, tech-driven cost cuts, and ambitious revenue gains. Could their digital health innovations offset rising risk and stricter regulations? Only the full narrative reveals what’s factored into this punchy fair value calculation.

Result: Fair Value of $12.88 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

Still, robust digital adoption and Oscar’s strong top-line growth could challenge the bearish view. This supports hopes for faster-than-expected profitability improvements.

Find out about the key risks to this Oscar Health narrative.

Another View: Multiples Tell a Different Story

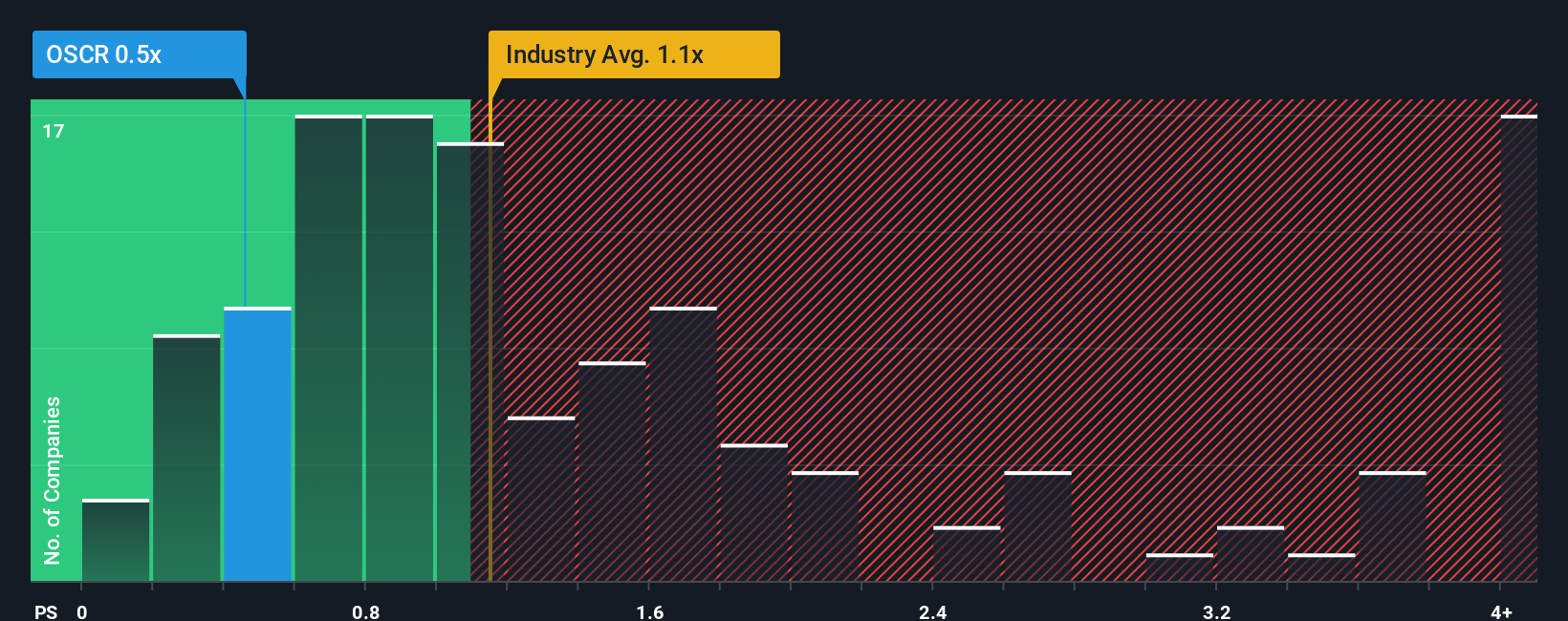

Looking through the lens of market pricing, Oscar Health’s price-to-sales ratio sits at just 0.4x. That is a notable discount compared to both industry peers (0.7x average) and the broader US Insurance sector, where the average is 1.1x. It also falls well below our fair ratio. This suggests the market may not be fully buying the growth narrative, introducing upside potential if sentiment shifts; yet it could also signal skepticism about sustainable profits. Which scenario will play out next?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Oscar Health Narrative

If you see things differently or want to dig into the numbers yourself, you can craft your own perspective quickly. Do it your way

A great starting point for your Oscar Health research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Opportunities?

Don’t leave potential gains on the table. Step up your investing strategy with fresh stock ideas tailored to trends and market shifts on Simply Wall Street.

- Unlock value by targeting companies often overlooked with proven upside in these 933 undervalued stocks based on cash flows for cash flow-driven bargains that might not stay hidden for long.

- Boost your returns with reliable passive income streams by checking out these 15 dividend stocks with yields > 3% yielding over 3% and built for financial strength.

- Embrace the frontier of technology by tracking rapid growth fields using these 25 AI penny stocks, where artificial intelligence is driving the next wave of winning businesses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:OSCR

Oscar Health

Operates as a healthcare technology company in the United States.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

92 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative